You are now leaving the Bright website and entering a third-party website. Bright has no control over the content, products, or services offered, nor the security or privacy of information transmitted to others via their website. We recommend that you review the privacy policy of the site you are entering. Bright does not guarantee or endorse the products, information, or recommendations provided on any third-party website.

In today's world, access to financial resources is essential for achieving various life goals. Whether you are looking to buy a car or cover unexpected medical expenses, loans are often the go-to solution. The two common types of loans people consider are auto loans and personal loans for such needs. They serve as valuable tools for financing different needs but have distinct characteristics, eligibility criteria, and uses.

In this comprehensive guide, we delve deep into the world of auto loans and personal loans, helping you understand the key differences between them and assisting you in making sound financial decisions.

Read more: Top 10 Emergency Loan Lenders for Bad Credit in the USA

Auto Loan vs. Personal Loan: Which One Should You Choose?

Auto loans and personal loans serve distinct purposes. Auto loans are specifically for purchasing vehicles, using the vehicle as collateral. In contrast, personal loans are versatile and can be used for various expenses. Auto loans often have lower interest rates due to collateral, while personal loans have higher rates but offer flexibility.

Understanding the Importance of Loans

Loans are pivotal in modern society, as they enable individuals to accomplish various financial goals. They provide the necessary funds to buy a home, pursue higher education, start a business, or address unexpected expenses. Loans come in many forms, tailored to specific needs and circumstances. Among the myriad options available, auto and personal loans stand out as versatile choices, each with unique features and benefits.[1]

Begin your journey to financial wellness - Sign up with Bright Money today!

Auto Loans

Auto loans are a financial tool designed specifically for purchasing vehicles. They provide borrowers with the necessary funds to buy a car while offering the lender security in the form of the vehicle itself. The key feature of an auto loan is that the car being financed serves as collateral. This means that if the borrower defaults on the loan, the lender has the right to repossess the vehicle to recoup their losses. Due to this collateral, auto loans typically come with lower interest rates compared to unsecured loans, making them an attractive option for those looking to finance a car purchase.

Auto loans often have fixed repayment terms, commonly ranging from 36 to 72 months, though some lenders may offer longer terms. The loan amount, interest rate, and repayment term determine the monthly installment, which remains consistent throughout the loan's duration.

Borrowers can apply for auto loans through banks, credit unions, or dealership financing departments, with the choice often depending on their creditworthiness and individual financial circumstances. Overall, auto loans provide a structured and accessible way to finance a vehicle, allowing borrowers to drive off with a new or used car while spreading the cost over time.[2]

Now that we've explored the ins and outs of auto loans, let us turn our attention to personal loans and understand how they differ.

Discover smarter savings and budgeting - Join Bright Money now!

Personal Loans

A Personal Loan is a versatile financial product that provides borrowers with a lump sum of money, which they can use for various purposes, such as debt consolidation, home improvements, medical expenses, or even a dream vacation. Unlike auto loans or mortgages, personal loans are typically unsecured, meaning they do not require collateral like a car or home. This absence of collateral makes personal loans accessible to a wide range of borrowers, but it also means that interest rates can be higher than those of secured loans.

The fact that Personal Loans have fixed interest rates and repayment terms is one of their fundamental characteristics. This makes it simpler for borrowers to budget and plan for repayment because they have a clear idea of their monthly payments from the beginning. Numerous financial institutions, including banks, credit unions, and online lenders, offer personal loans.

A Personal Loan's acceptance is based on criteria such as the borrower's credit history, income, and lending guidelines. Personal loans are a great choice for people who want to fund various projects or consolidate debt while keeping their financial stability because of their flexibility and adaptability for a wide range of financial needs.[3]

Take control of your finances - Start saving with Bright Money!

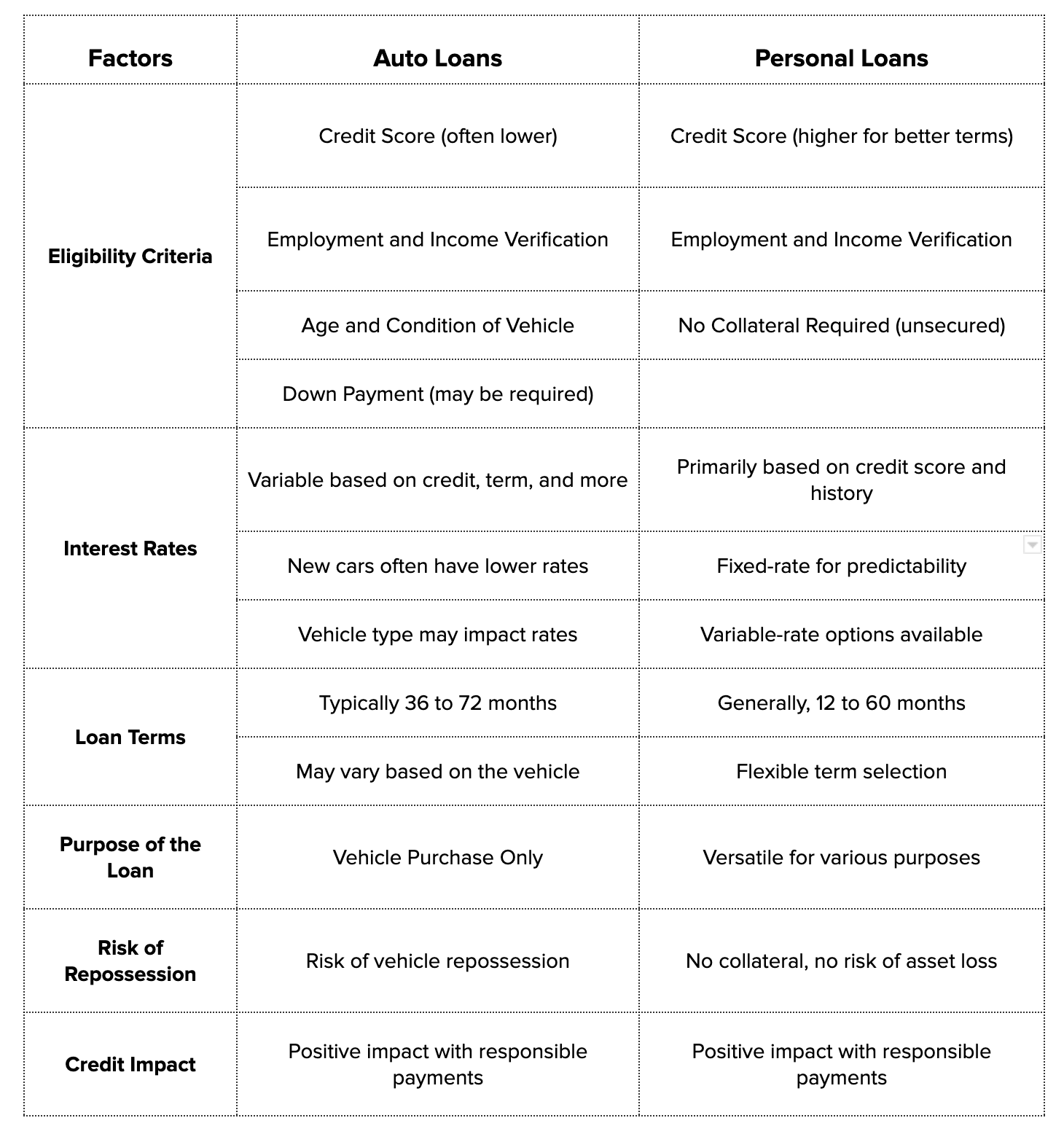

Comparing Auto Loans and Personal Loans

When deciding between an auto loan and a personal loan, several factors should influence your choice. These include eligibility criteria, interest rates, loan terms, and the purpose of the loan. Certainly, here's a table comparing Auto Loans and Personal Loans based on various factors:[4]

Please note that the specific terms and conditions can vary based on individual lenders' and borrowers' credit profiles. Shopping around and comparing offers is essential to determine the best fit for your financial needs.

Read more: How to Avoid Interest on Credit Cards?

Conclusion

In the world of financing, auto loans and personal loans are valuable tools that cater to various financial needs and circumstances. Auto loans are designed for the specific purpose of purchasing vehicles and are secured by the vehicle itself. Personal loans, on the other hand, are unsecured and can be used for a wide range of purposes.

When deciding between these two loan types, consider your financial goals, creditworthiness, and the purpose of the loan. Auto loans are ideal for those looking to finance a vehicle purchase, offering competitive interest rates and longer terms for new cars. Personal loans provide greater flexibility, allowing you to use the funds as needed, but they may come with slightly higher interest rates.

Ultimately, the choice between an auto loan and a personal loan depends on individual circumstances and preferences. By understanding the key differences outlined in this article, you can make an informed decision that aligns with your financial goals and helps you achieve your objectives while managing your finances responsibly.

Join our community of savvy savers - Sign up for Bright Money!

References:

- https://www.forbes.com/advisor/in/loans/types-of-loans/

- https://www.investopedia.com/how-car-loans-work-5202265

- https://www.investopedia.com/personal-loan-5076027

- https://www.investopedia.com/articles/personal-finance/070915/personal-loans-vs-car-loans-how-they-differ.asp

FAQs

- Can I use a personal loan to buy a car?

Yes, you can use a personal loan to buy a car. Personal loans are versatile and can be used for various purposes, including purchasing a vehicle. However, keep in mind that personal loans are typically unsecured and may have higher interest rates compared to auto loans.

- What is the minimum credit score needed for an auto loan?

The minimum credit score required for an auto loan varies among lenders. Generally, a credit score of 660 or higher is considered good for securing favorable auto loan terms. However, some lenders may work with borrowers who have lower credit scores but may offer less favorable terms.

- How do I qualify for a personal loan?

Qualifying for a personal loan depends on factors such as your credit score, income, employment history, and debt-to-income ratio. A higher credit score and a stable source of income can increase your chances of approval and secure better loan terms.

- What is the difference between a fixed-rate and variable-rate loan?

A fixed-rate loan has an interest rate that remains constant throughout the loan term, providing predictability in monthly payments. In contrast, a variable-rate loan has an interest rate that can change periodically based on market conditions, potentially leading to fluctuating monthly payments.

- Can I pay off my auto loan or personal loan early without penalties?

Many auto loans and personal loans allow borrowers to pay off their loans early without penalties. However, it is essential to review the terms and conditions of your loan agreement to confirm whether early repayment is allowed and if any prepayment penalties apply.