You are now leaving the Bright website and entering a third-party website. Bright has no control over the content, products, or services offered, nor the security or privacy of information transmitted to others via their website. We recommend that you review the privacy policy of the site you are entering. Bright does not guarantee or endorse the products, information, or recommendations provided on any third-party website.

Dealing with Credit Card Debt can be overwhelming, especially when high-interest rates are eating away at your finances. For many individuals, finding a way to manage and eventually eliminate Credit Card Debt is a top financial priority. One effective strategy for achieving this goal is to refinance your Credit Card Debt using a personal loan.

Read more: What is a Credit: Everything you need to know in 2023

Credit Card Debt can quickly spiral out of control, with high-interest rates causing balances to grow exponentially. According to the Federal Reserve, the average Credit Card interest rate in the United States was around 24% as of 2023. This can make it challenging to pay down the Debt, as a significant portion of your monthly payments goes towards interest rather than reducing the principal balance.

Refinancing Credit Card Debt with a personal loan is a smart move to regain control over your financial situation and reduce the cost of your Debt. Personal loans typically offer lower interest rates than Credit Cards, making it easier to manage your Debt and pay it off more quickly. Personal loans often come with fixed monthly payments, providing a clear roadmap to Debt freedom.

This article will discuss the best loans for refinancing Credit Card Debt, including different types of loans, their advantages, and how to choose the right one for your unique financial situation.

What are the best Loans for Refinancing Credit Card Debt?

The best loans for refinancing Credit Card Debt often include Debt Consolidation loans, where you can combine multiple Credit Card balances into a single, lower-interest loan. Consider exploring Bright Money for Debt Consolidation solutions that can simplify your payments and potentially reduce your interest costs.

Other options like personal loans, balance transfer Credit Cards, home equity loans (HELOCs), and peer-to-peer (P2P) loans also offer advantages, but Debt Consolidation loans are particularly effective in managing Credit Card Debt.

Start Your Path to Financial Freedom Today! Sign Up with Bright Money and Take Control of Your Finances.

Why should you Refinance your Credit Card Debt?

Refinancing your Credit Card Debt is like giving your finances a fresh start. It's a smart move because it can help you in several ways. First, it can lower your interest rates, which means you pay less over time. Second, it simplifies your financial life by combining multiple payments into one. Plus, it can give your credit score a boost since your credit utilization ratio goes down.

However, don't rush into it – shop around for the best deal and make sure you're aware of any fees. Most importantly, commit to better money habits to avoid falling back into Debt. It's your path to financial freedom.[1]

Don't Let Debt Hold You Back. Join Bright Money Now and Refinance Your Credit Card Debt for a Brighter Financial Future.

Now that we've established the advantages of refinancing Credit Card Debt, let's explore the best loan options available for this purpose.

Read more: How to choose the best Credit Card for you

The best Loans for Refinancing Credit Card Debt

When it comes to refinancing Credit Card Debt, several loan options can help you achieve your financial goals. Each type of loan has its advantages, and the best choice depends on your specific needs and financial situation.

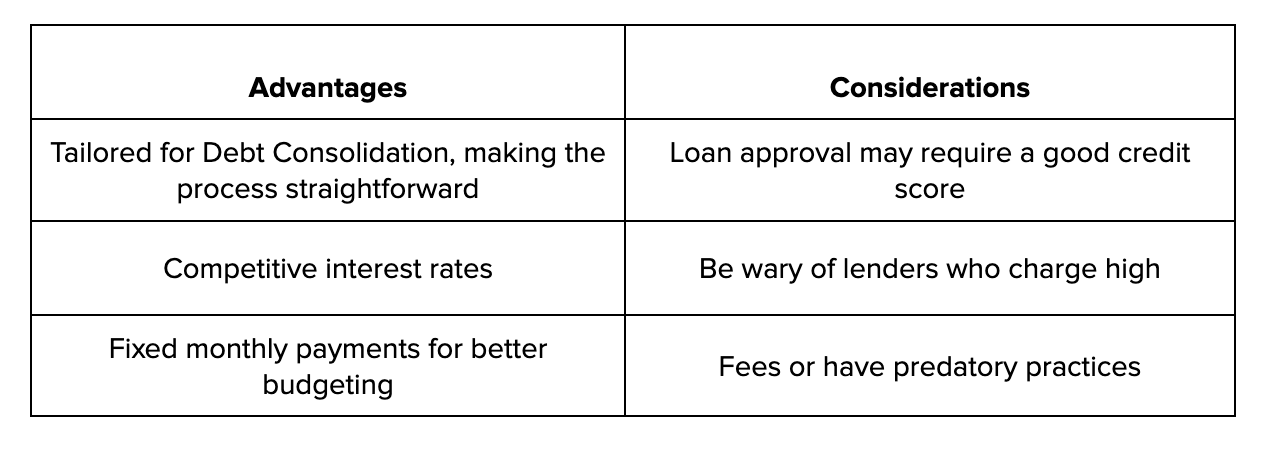

1. Debt Consolidation Loans

Debt Consolidation loans are specifically designed to help individuals consolidate and refinance their Debts, including Credit Card balances. Banks, credit unions, or online lenders often provide these loans.[2]

- General APR: Varies but typically ranges from 5% to 36%

- Payback Time: Typically 2 to 7 years

- Loan Amount: Can range from $1,000 to $100,000 or more

- Credit Score Required: Usually 580 or higher for the best rates

Certainly, here's a table summarizing the advantages and considerations of Debt Consolidation loans:

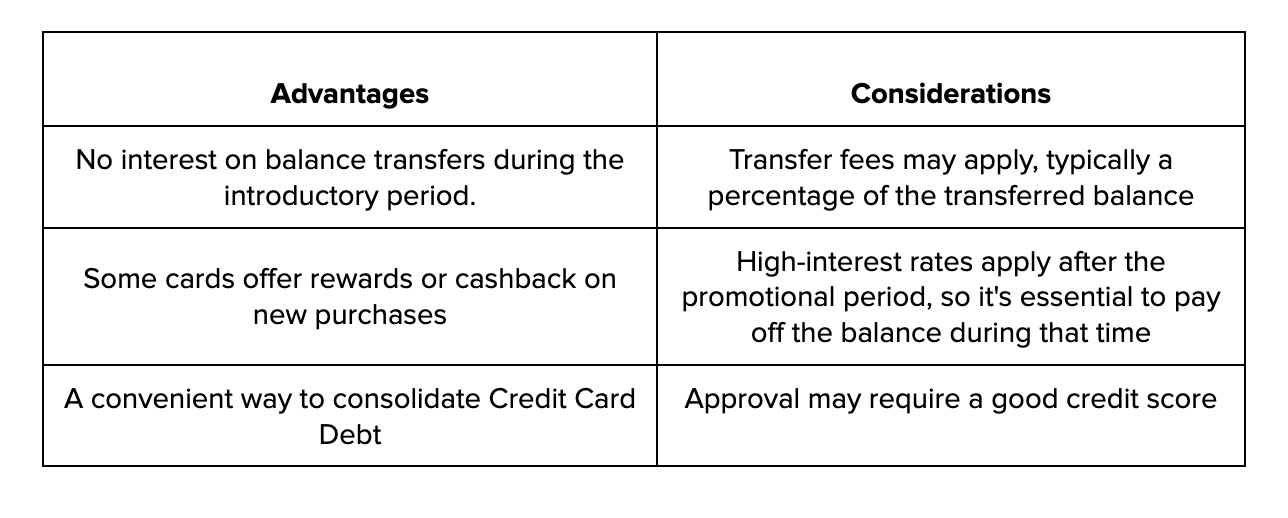

2. Balance Transfer Credit Cards

Balance transfer Credit Cards are another popular method for consolidating and refinancing Credit Card Debt. These cards offer an introductory 0% APR on balance transfers for a specific period, typically ranging from 12 to 18 months. During this promotional period, you can transfer your existing Credit Card balances to the new card without incurring any interest charges.[2]

- Introductory APR: 0% on balance transfers for 12 to 18 months

- Regular APR: Varies but often higher after the introductory period

- Credit Score Required: Good to excellent credit (usually 670 or higher)

Certainly, here's a table summarizing the advantages and considerations of balance transfer Credit Cards:

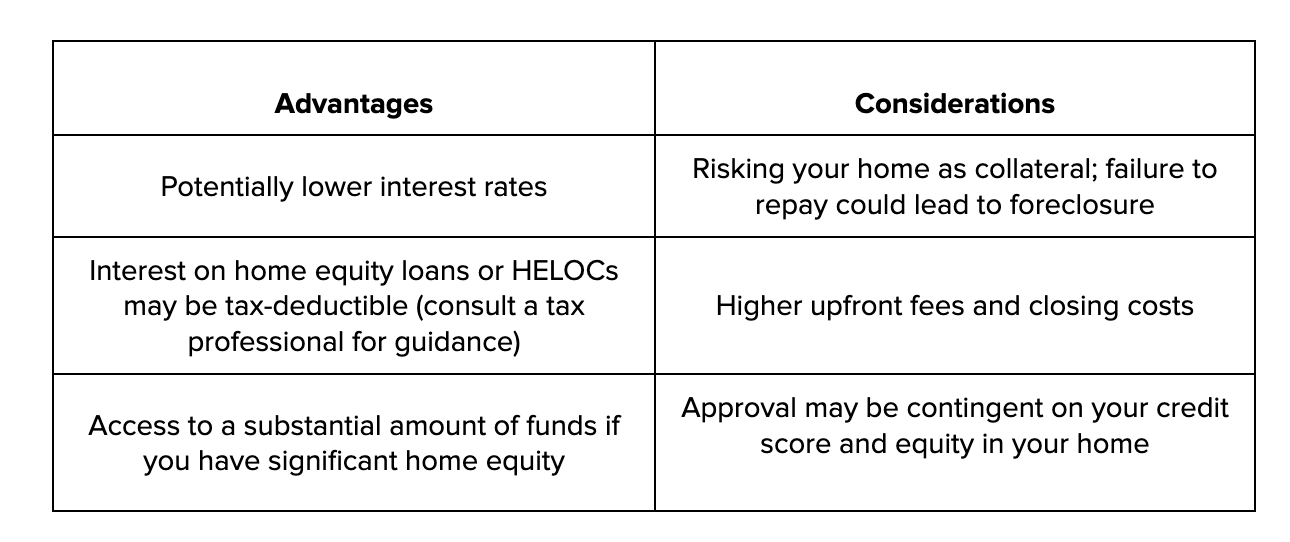

3. Home Equity Loans or HELOCs

If you're a homeowner with substantial equity in your property, you might consider using a home equity loan or a home equity line of credit (HELOC) to refinance your Credit Card Debt. These loans use your home as collateral, which can lead to lower interest rates compared to unsecured loans.[2]

- General APR: Typically lower than unsecured loans, around 4% to 8%

- Payback Time: Can extend up to 30 years

- Loan Amount: Depends on your home equity, usually up to 85% of the home's value

- Credit Score Required: Usually 620 or higher, but higher scores can secure better rates

Certainly, here's a table summarizing the advantages and considerations of home equity loans and HELOCs (Home Equity Lines of Credit):

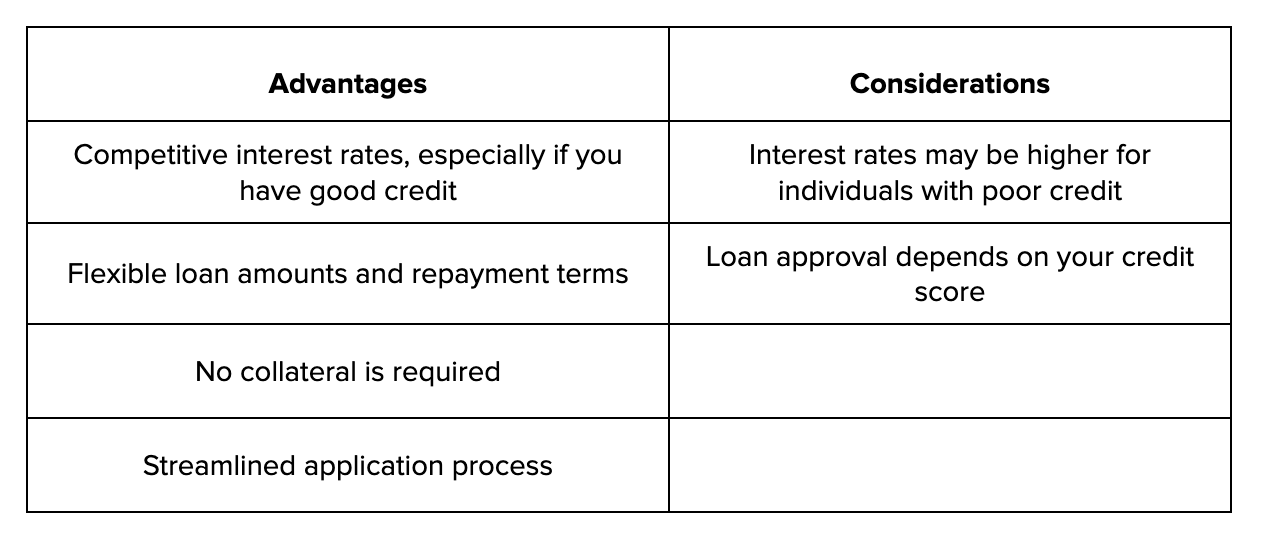

4. Personal Loans

Personal loans are a versatile option for refinancing Credit Card Debt. These loans are typically unsecured, meaning you don't need to provide collateral. They offer fixed interest rates, fixed monthly payments, and a set repayment term, making it easy to budget and plan your Debt payoff.[2]

- General APR: Varies widely, from 6% to 36%

- Payback Time: Typically 2 to 5 years

- Loan Amount: Ranges from $1,000 to $100,000 or more

- Credit Score Required: Generally 580 or higher for the best terms

Certainly, here's a table summarizing the advantages and considerations of unsecured personal loans:

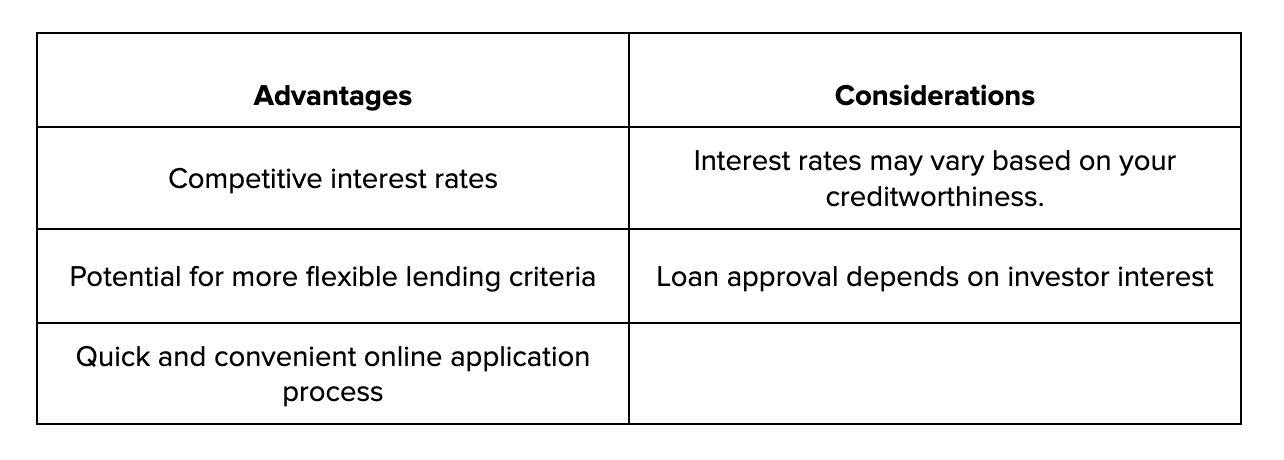

5. Peer-to-Peer (P2P) Loans

P2P lending platforms connect borrowers with individual investors willing to fund their loans. These loans often have competitive interest rates and can be used for various purposes, including refinancing Credit Card Debt.[2]

- General APR: Varies but often competitive, starting around 6%

- Payback Time: Typically 3 to 5 years

- Loan Amount: Varies, depending on the P2P platform and investor interest

- Credit Score Required: Some P2P lenders accept scores as low as 600, but better rates come with higher scores

Certainly, here's a table summarizing the advantages and considerations of peer-to-peer lending:

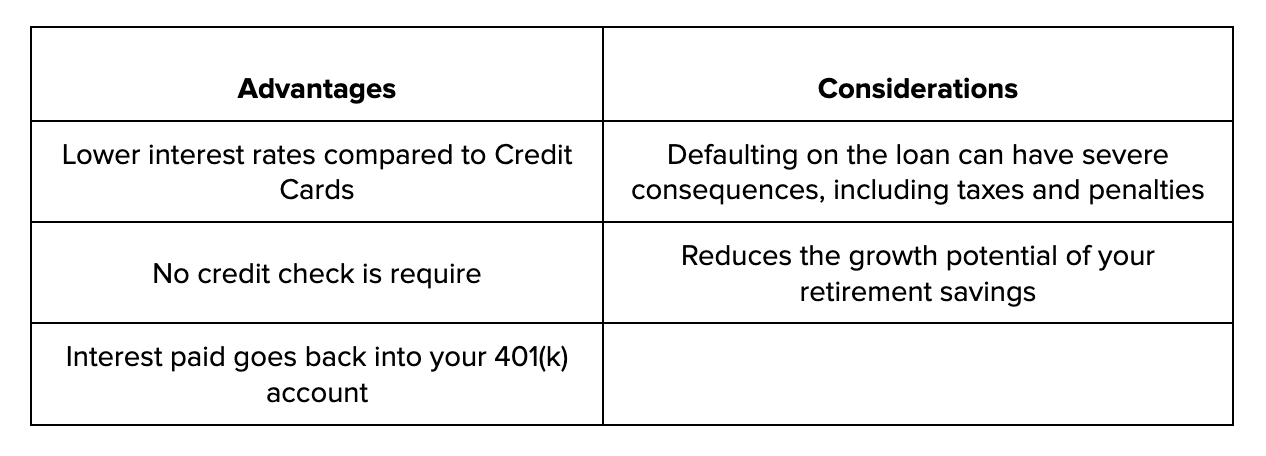

6. 401(k) Loans

If you have a 401(k) retirement account, you may have the option to borrow against it to refinance Credit Card Debt. 401(k) loans typically come with lower interest rates than Credit Cards; you're essentially borrowing from yourself.[2]

Certainly, here's a table summarizing the advantages and considerations of 401(k) loans:

Ready to Save Thousands of Dollars on Interest? Click Here to Sign Up with Bright Money and Begin Your Debt-Free Journey.

Choosing the Right Loan for Refinancing Credit Card Debt

Selecting the right loan to refinance your Credit Card Debt is like picking the perfect tool for a DIY project – it requires careful consideration. Here's a step-by-step guide using an example to make it crystal clear:

- Assess Your Credit Score

Think of your credit score as your financial report card. Imagine yours is excellent, say around 800, and that's like getting an A+. With such a score, you'll have access to the best deals – lower interest rates. But if it's not that great, let's say it's more like a C, around 650, consider doing some homework before applying. Work on improving your score, like paying bills on time or correcting any errors on your credit report.

- Calculate Your Debt and Monthly Payments

Imagine you have $10,000 in Credit Card Debt, and you can comfortably allocate $300 each month to repay it. Knowing these numbers helps you figure out what kind of loan you need and how long it will take to pay it off.

- Compare Interest Rates and Fees

Just like you'd shop around for the best price on a new gadget, do the same for loans. Interest rates aren't one-size-fits-all. They depend on your credit score and the type of loan. Also, watch out for any hidden fees. Imagine you find a personal loan with a 10% interest rate and no fees, while another one offers 8% interest but has a hefty origination fee – you'd need to calculate which one is truly the better deal.

- Consider Your Home Equity

Let's say you own a home. You might be tempted to use your home equity through a loan or a Home Equity Line of Credit (HELOC) to refinance your Credit Card Debt. These can offer even lower interest rates, like 4% or 5%. However, remember, your home is on the line here. If you can't make the payments, you could lose it. So, proceed with caution.

- Review the Terms and Conditions

Imagine you've found a loan that looks good on the surface. But now, it's time to read the fine print – the terms and conditions. What's the interest rate? How long do you have to pay it back? Are there any penalties for paying early or being late? Make sure you understand every detail.

- Create a Debt Repayment Plan

Once you've refinanced your Credit Card Debt, it is time to get down to business. Create a plan, like a roadmap, for paying off the loan. Imagine you've chosen a personal loan with a 3-year term and a fixed monthly payment of $350. Stick to your budget, cut unnecessary expenses, and stay disciplined. Imagine it's like a mission – you're on a quest to be Debt-free.

With these steps in mind, you'll be better equipped to choose the right loan to refinance your Credit Card Debt and pave the way to a more financially secure future.[3]

Experience Stress-Free Money Management with Bright Money. Sign Up Now for a Smarter, More Secure Financial Tomorrow.

Maximizing your financial potential with Bright Money

Bright Money is like having a financial guru in your pocket when it comes to refinancing Credit Card Debt. They've got your back with personalized insights and advice, making the whole process way less daunting. Think of it as your trusty sidekick on your journey to tackling Debt and improving your financial health.

With Bright Money's user-friendly tools and expert tips, you'll be better equipped to make smart decisions and save more. So, refinancing your Credit Card Debt becomes a breeze, and you can focus on what matters most – getting that Debt under control and achieving financial freedom.

Read more: 3 reasons to use personal loans to pay off Debt

Conclusion

Refinancing Credit Card Debt can be a game-changer for your financial well-being. By selecting the best loan option for your situation and diligently following a Debt repayment plan, you can take significant steps toward becoming Debt-free and achieving greater financial stability.

Remember that financial discipline and responsible credit management are key to successfully refinancing your Credit Card Debt. With the right strategy and commitment, you can reduce the burden of high-interest Credit Card balances and pave the way for a more secure financial future.

It's time to Put Your Money to Work for You. Join Bright Money Today and Start Making Your Financial Dreams a Reality.

References:

- https://www.credible.com/blog/personal-loan/credit-card-refinancing/#:~:text=But%20if%20you%20refinance%20your,Reduce%20your%20monthly%20payment.

- https://www.cnbc.com/select/best-loans-for-refinancing-credit-card-Debt/

- https://www.Debt.org/credit/cards/refinancing/

- https://financebuzz.com/how-to-refinance-credit-card-Debt

FAQs

Q. Can I refinance my Credit Card Debt with a bad credit score?

If you have a less-than-perfect credit score, you can still refinance your Credit Card Debt, but your options may be limited. Personal loans and balance transfer Credit Cards often require a good credit history for the best rates. However, some lenders specialize in loans for individuals with poor credit. These loans typically come with higher interest rates, so it's crucial to compare offers and consider the overall cost before committing. Alternatively, you may consider other methods, like Debt Consolidation or seeking a co-signer to improve your chances of approval and secure a better interest rate.

Q. What is the difference between a personal loan and a balance transfer Credit Card?

Two common options for refinancing Credit Card Debt are personal loans and balance transfer Credit Cards. Personal loans are installment loans with fixed monthly payments and interest rates, making it easier to budget. In contrast, balance transfer Credit Cards offer a promotional 0% APR on transferred balances for a limited time. Still, they may come with balance transfer fees and higher rates after the introductory period. Your choice depends on factors like your credit score, the amount of Debt you have, and your preferred repayment method.

Q. How much can I borrow when refinancing Credit Card Debt?

The amount you can borrow when refinancing Credit Card Debt depends on several factors, including your creditworthiness, the type of loan you choose, and the lender's policies. Personal loans typically offer loan amounts ranging from a few thousand dollars to tens of thousands, while balance transfer Credit Cards may limit your transfer based on your credit limit. Calculating your existing Credit Card Debt and choosing a loan that covers it while considering your ability to make monthly payments comfortably is essential.

Q. What happens to my Credit Card accounts after refinancing?

When you refinance Credit Card Debt, the original Credit Card accounts are usually closed. Your Credit Card balances are transferred to the new loan or Credit Card, and you'll make payments directly to the new lender. Closing these accounts can affect your credit score by reducing your available credit, potentially increasing your credit utilization rate. However, as you make on-time payments on the new loan or card, your credit score should improve over time, offsetting the initial dip caused by closing the old accounts.

Q. Is refinancing Credit Card Debt the right choice for everyone?

Refinancing Credit Card Debt is a viable solution for many, but it may not be the best choice for everyone. Before deciding, assess your financial situation, credit score, and ability to make consistent payments. Consider alternative Debt reduction strategies like creating a budget, increasing income, or negotiating with creditors. It's essential to choose a path that aligns with your financial goals and capacity to manage Debt effectively. Consulting with a financial advisor or credit counselor can provide personalized guidance on the best approach for your unique circumstances.