You are now leaving the Bright website and entering a third-party website. Bright has no control over the content, products, or services offered, nor the security or privacy of information transmitted to others via their website. We recommend that you review the privacy policy of the site you are entering. Bright does not guarantee or endorse the products, information, or recommendations provided on any third-party website.

You can barely go two whole years without reading a prediction of “imminent financial crisis.”

Shock. Horror. Brace yourself.

Newspapers, TV, politicians, economic pundits… they all have a view.

What are these mythical monsters of our economy all about?

As a broad definition: a financial crisis is when some part of our financial system stops working smoothly or has a sudden shock and comes to a standstill.

Globally there have been approximately 60 financial crises as we’ve been able to identify them.

The earliest of them took place as far back as the Byzantine Emperor Justinian II - in the 7th century CE. There was a crash of confidence in the coin currency of the day. It became public knowledge that Justininan’s government had been diluting the quantity of copper in coins, the currency of the time. There was a full-blown riot ending in Justinian having his nose cut off in front of a bloodthirsty group of spectators. Don’t mess with people’s money, even if you’re a Roman Emperor.

Then there’s the Dutch Tulip Mania of 1637. There was a rapid price increase and crash in the price of tulips. Yes, tulips, the flower. Was it that important? Not really. But it was the first notable market crash, driven by rampant speculation.

More substantially, in 1720 - two important companies crashed in Britain and France. The South Sea company in Britain and the Mississippi company in France. The resulting crisis of confidence had a deep impact on both countries. Some historians see this as a domino for the seismic French revolution of 1789, who’s effects lasted a full century, at least.

These are the OG examples. Since this, we have had 60-ish across the world. They have happened in the period of rapid economic growth since the 1750s, coinciding with our ability to capture good economic and financial data.

Of these 60 crises, no less than 24 have happened in the US.

But why so many in the US?

The US is one of the three countries that industrialized the fastest (along with the UK and France). This set of countries have had a long economic history as modern market economies, giving them opportunity for more financial crises.

The UK has similarly had 15 of these crises. Between the US and the UK, you have almost 70% of well-documented financial crises across the world.

Crises are most relevant to modern market economies where the flows of capital are determined by market places, meaning private investors and private companies (not governments) drive decisions responding to market dynamics and prices.

So what is a financial crisis?

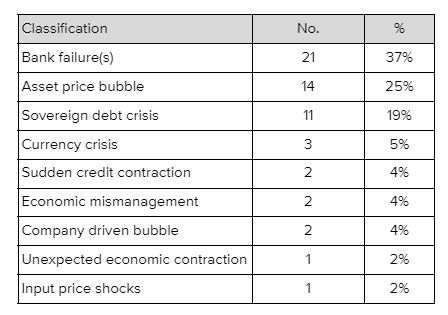

We have analyzed the 60 crises over the last 250 years that have happened across the world. Based on historical descriptions, we developed a classification to explain the underlying catalyst of each one.

You will see the top three reasons cover +80% of all cases:

- Bank failures

- Asset price bubbles

- Sovereign debt crisis

These three causes can come all together. One can precipitate the other in a spiraling domino.

We have classified each crisis based on our reading of original causes within their financial system.

Let’s explain each of these in turn and cover what makes them a financial crisis.

Bank failures

The financial system is at the heart of the economy. To understand why, read our article: The Economy Stack: Understanding financial services at the heart.

In a private sector-driven economy, private banks dominate the system. Banks have balance sheets of assets and liabilities. What makes a bank precarious as a company is that the asset-side of the balance sheet are primarily financial instruments that heavily depend on the behavior of other parties: loans they have provided to individuals and businesses. If the asset side of the balance sheet suddenly contracts due to a repricing or non-performing assets that have to be marked down, a bank can quickly become insolvent, where their liabilities are greater than their assets.

This causes banks to fail, needing them to go through bankruptcy, so all those with pending claims - holding the liabilities - can get what is left. When a bank or several banks fail, many people can lose wealth fast, if exposed to these liabilities.

Often this causes a contagion effect, when other banks are exposed to that liability and are then forced to mark down their own assets, resulting in a series of domino insolvencies. This is why bank failures can cause so much damage particularly if they are big banks, with large liabilities, with many other parties exposed to these. To understand how contagion has risked bringing down major economies in the last 20 years, there is no better account than Timothy Geithner’s Stress Test.

The disparaging quip that came from the 2008 crisis was “a bank too big to fail.” This was a reference to the contagion effect. The potential contagion from one or several banks failing can bring down the entire financial sector.

There were as many as 8 years of financial crises in the US that were triggered by bank failures: 1792, 1819, 1837, 1857, 1873, 1884, 1907, 1914. You can see many of them happened in the 19th century, when the US banking system was nascent, and even before the Fed was founded in 1913. The Fed needed to play the role of “lender of last resort.” to provide better stability to the private banking sector.

Asset price crashes

Assets are stores of our wealth. Some are stable and more predictable, e.g. the US dollar or gold, and some are highly volatile, like company stocks or crypto.

The value of an asset is determined by a prediction of how much cash it can generate in the future. The value of some assets - like company stocks - rely heavily on a long view of the future. If there is a sudden change in expectations or the costs/benefits associated with the future, the price of stocks can violently adjust.

Sometimes people have a very optimistic view of the future, which causes certain asset prices to increase too dramatically too fast, often beyond a sensible justification. It can be driven by market “herding effects” where people start behaving irrationally, seeing the behavior of others, which keeps pushing up the value of the asset. We can also refer to this as speculation.

Suddenly new information arrives, or there’s a change in the mood of the herd. What follows is a large number selling the asset in favor of other assets, causing a sudden crash in value.

Why do volatile asset prices cause a crisis?

Sometimes a lot of wealth has gone into a particular asset class, such that a sudden crash in its price considerably affects the wealth of people or investors. This affects the confidence of people to keep investing, with a stable belief in the future. This rapid pullback of investment activity, which can happen across asset classes, causes a crisis in the financial system.

Some asset classes have a big effect on consumer confidence. Like house prices. When house prices suddenly fall, consumers suddenly feel psychologically poorer leading them to spend less. We call this the “reverse wealth effect.” It can cause an economic slowdown, and sometimes recession.

There are many varied examples of asset price crashes in US history:

- Land speculation bubble of 1796-97

- Gold panic of 1869

- Railroad industry financing panic of 1893

- Stock market crash of 1929

- Stock market crash of 1987

- Dot com bubble crash of 2001

- Housing market crash of 2007-2008

Sovereign debt crises

Governments take on public debt to fund investment, to make the economy stronger and more productive in the future. For example: investing in education, infrastructure or healthcare. The primary logic of taking on public debt is that if good investments are made, the economy will grow faster and will increase the revenues of the government - its tax collection - making it easier to pay off this debt in the future. So public investment can pay for itself, providing it has indeed been investment well made that accelerates growth.

Often enough, governments go too far. They take on so much debt that their ability to continue to make payments against this debt is in doubt. The providers of the debt are private markets. When private markets become unsure, it crashes the perceived value of government debt, which is tradable in bond marketplaces. When that happens, it is much harder for the government to raise future debt and even to make payments on existing liabilities.

Governments can become stuck, where they can no longer raise money to meet obligations or to fund operations in leading the economy.

Examples of sovereign debt crises (which have only happened outside the US):

- France's financial and debt crisis (1783–1788)

- Latin American debt crisis (1980s, beginning in Mexico in 1982)

- Russian financial crisis in 1998

- Spanish financial crisis from 2008-2014

Are we in a crisis right now?

In the last 2 months, there has been turbulence in many financial markets and the economy. Let’s evaluate the US right now.

- Are there bank failures?

- Generally banks seem healthy. They are solvent. Their balance sheets are not under pressure. In fact, in many cases, they see record levels of earnings driven by rising credit spreads. The long tail of small banks and financial institutions in the US (up to 9,000) also have healthy balance sheets, with up to 20% of their assets not deployed as loans - a good reserve keeping them solvent.

- Is there an asset price crash?

- Stock markets have come down but have not significantly crashed, which we would define as a 30%+ drop year on year.

- Housing prices have downward pressures, but are not crashing. There are equal upward pressures on housing prices, given the shortness of housing supply and high rental costs.

- Government and high-grade corporate bond markets are healthy. Capital is flowing here due to the “correction period” for equities, in particular tech stocks and web3 assets.

- Are we in a sovereign debt crisis?

- The US public debt is increasing, especially post the fiscal stimulus of the pandemic. But the US is not at risk of defaulting on this debt. Tax revenues are high, and the “service cost” for its debt is less than 5% of annual tax revenue. Sovereign debt crises typically affect emerging markets more. It is relevant in Sri Lanka and Russia right at this moment, but they are much smaller economies in the global picture and will not substantially affect the US.

Thus, there are no signs we are in a financial crisis in the US right now - despite having seen stock markets drop by 10-15% (25% for the NASDAQ) since the beginning of 2022.

We might be entering an economic recession, which is a different phenomenon. So what’s the difference between an economic recession and a financial crisis, and do they come together?

To understand this question, read our article: “So you say we’re in a recession? What’s going on?!?”