You are now leaving the Bright website and entering a third-party website. Bright has no control over the content, products, or services offered, nor the security or privacy of information transmitted to others via their website. We recommend that you review the privacy policy of the site you are entering. Bright does not guarantee or endorse the products, information, or recommendations provided on any third-party website.

Did you know that about 15% of Americans said they had been sued by a debt collector, according to a 2017 Consumer Financial Protection Bureau report? Dealing with debt collectors can be a challenging experience for many individuals. The fear of being sued by debt collectors is a common concern among debtors.

It is recommended to read about the 5 Inspiring Stories of Building Credit with Credit Cards by Bright Money App before we dive more into the topic!

In this comprehensive article, we will be exploring the topic of whether debt collectors can sue you. We will address various aspects related to debt collection lawsuits, your rights as a debtor, strategies to protect yourself, and alternative solutions to legal action.

The Fair Debt Collection Practices Act (FDCPA)

In the United States, the Fair Debt Collection Practices Act (FDCPA) protects consumers against unfair debt collection practices. Enforced by the Federal Trade Commission (FTC), this act lays down strict guidelines that debt collectors must adhere to when attempting to collect debts. These guidelines aim to prevent harassment, deception, and abuse in the debt collection process.

Can Debt Collectors Sue You?

Yes, debt collectors can sue you under certain circumstances when you owe unpaid debts. Roughly one in three Americans with a credit history have had debt in collections, according to the Urban Institute, so there are high chances of debt collectors suing you! Debt collectors are entities or individuals creditors hire to collect outstanding balances on their behalf. While their primary goal is to recover the owed money, there are specific scenarios that may lead them to take legal action against you. Let's explore different scenarios when debt collectors can sue you.

What are the Scenarios When Debt Collectors Can Sue You?

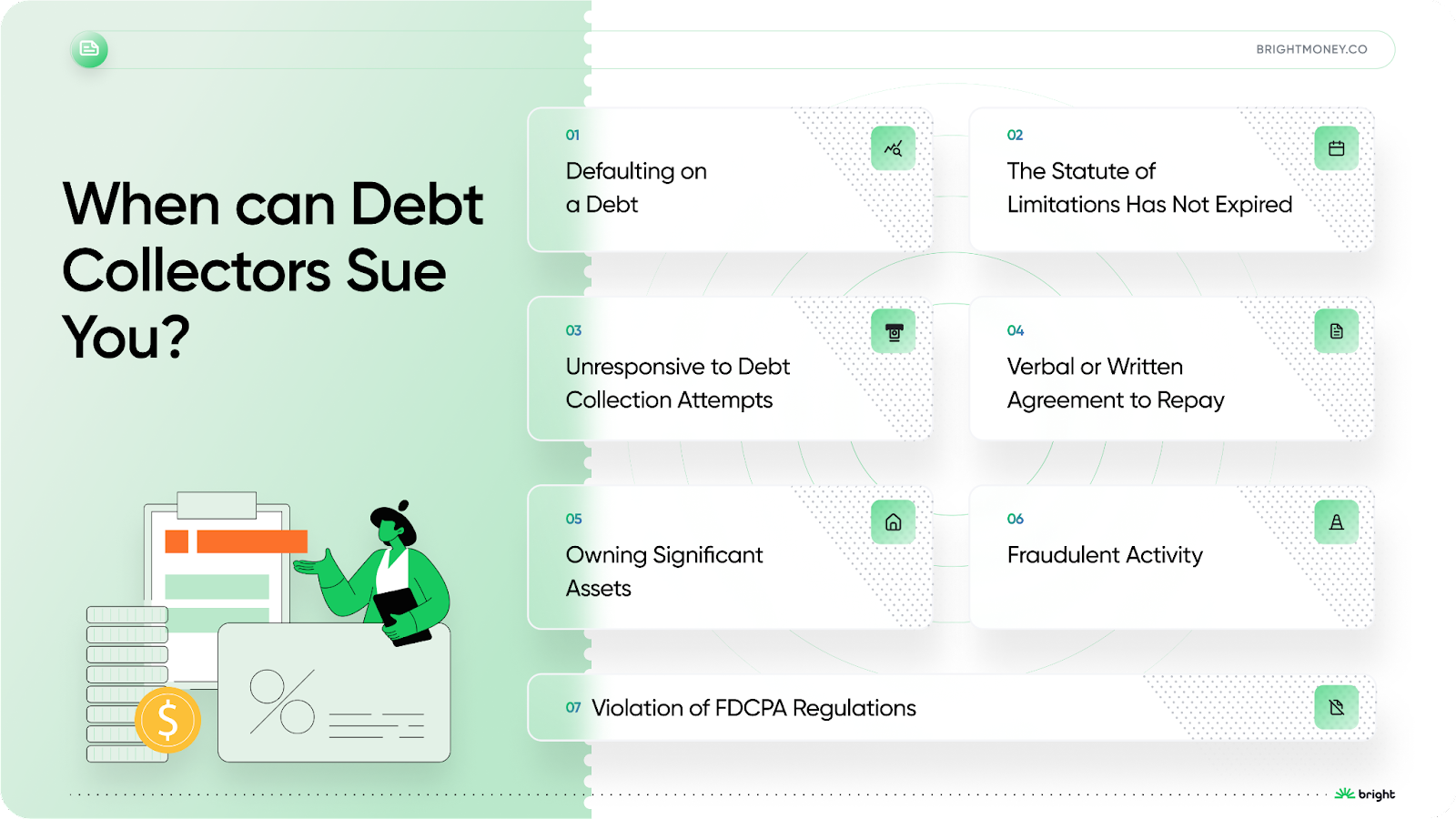

1. Defaulting on a Debt

One of the most common scenarios that can lead to debt collectors suing you is defaulting on a debt. When you fail to make payments according to the agreed-upon terms, the creditor may consider your account in default. After numerous attempts to collect the debt, the creditor may decide to transfer your account to a debt collection agency.

2. The Statute of Limitations Has Not Expired

Every state has a statute of limitations, which is the legal time frame within which creditors or debt collectors can sue you for a debt. Once the statute of limitations expires, the debt becomes "time-barred," and debt collectors lose their right to take legal action. However, it's crucial to note that the statute of limitations varies by state and type of debt.

3. Unresponsive to Debt Collection Attempts

Ignoring debt collection attempts will not make the debt go away. On the contrary, avoiding communication with debt collectors may lead them to take more aggressive actions, such as filing a lawsuit against you. Responding to debt collection efforts, even if you dispute the debt, is essential to avoid potential legal consequences.

4. Verbal or Written Agreement to Repay

If you have entered into a verbal or written agreement with a debt collector or creditor to repay the debt, failing to honor that agreement can give the debt collector grounds to sue you for breach of contract. It's crucial to be honest about your financial situation and only makes promises you can keep.

5. Owning Significant Assets

Debt collectors may be more inclined to sue debtors who own valuable assets. If they obtain a judgment against you, they may be able to place liens on your property or garnish your wages. Therefore, having valuable assets could increase the likelihood of facing a lawsuit.

6. Fraudulent Activity

If you engaged in fraudulent activity related to the debt, such as providing false information or identity theft, debt collectors may take legal action against you. Fraudulent actions can significantly complicate your situation, leading to more severe consequences.

7. Violation of FDCPA Regulations

While debt collectors have the right to pursue legitimate debts, they must do so within the boundaries set by the FDCPA. If they engage in prohibited practices, such as making false statements, threatening violence, or contacting you at inappropriate hours, you may have grounds to counter-sue them for violating your rights.

How to Protect Yourself?

When facing debt collection efforts or the possibility of a lawsuit, it's crucial to protect yourself and your rights as a debtor. Here are some essential steps to consider:

1. Know Your Rights

Familiarize yourself with the FDCPA guidelines and your state's laws concerning debt collection and the statute of limitations. Understanding your rights can help you respond appropriately to debt collectors' actions.

2. Validate the Debt

If you believe the debt is not legitimate or you dispute the amount owed, you have the right to request debt validation from the collection agency. Under the FDCPA, they must provide proof that you owe the debt before continuing their collection efforts.

3. Communicate in Writing

When dealing with debt collectors, it's advisable to communicate in writing rather than over the phone. Written communication allows you to keep a record of all interactions and provides a level of protection against harassment.

4. Seek Legal Advice

If you're facing a debt collection lawsuit or believe your rights have been violated, consider seeking legal advice from a qualified attorney, who specializes in consumer debt and FDCPA regulations.

5. Settle or Negotiate

If the debt is valid and you can afford to pay, consider negotiating a settlement with the debt collector. They may be willing to accept a reduced lump-sum payment or set up a reasonable payment plan.

Debunking Common Myths

There are several myths and misconceptions surrounding debt-collection lawsuits. Let's debunk a few of them:

Myth: Debt collectors can throw you in jail for unpaid debts.

Truth: Debtors' prisons are illegal in the United States. You cannot be incarcerated simply for owing money.

Conclusion

Dealing with debt collectors and the potential of being sued can be stressful. However, understanding your rights, the legal process, and available strategies can empower you to navigate these situations effectively and become debt free with the help of Bright Money! Remember to stay proactive, communicate clearly, and seek professional advice when needed. By taking the necessary steps, you can protect yourself and work towards resolving your debts.

Reference:

- https://www.urban.org/research/publication/delinquent-debt-america

- https://files.consumerfinance.gov/f/documents/201701_cfpb_Debt-Collection-Survey-Report.pdf

- https://www.consumerfinance.gov/ask-cfpb/can-debt-collectors-collect-a-debt-thats-several-years-old-en-1423/

- https://www.lendingtree.com/debt-consolidation/sued-by-a-debt-collector/#:~:text=You%20must%20respond%20to%20the,debt%20collector%20can%20sue%20you.

Frequently Asked Questions

1. Can debt collectors sue for old debts?

A: Debt collectors may still attempt to collect on old debts, but the statute of limitations may limit their legal options.

2. Can you go to jail for not paying debt collectors?

A: No, you cannot be imprisoned for unpaid debts. However, failure to comply with court orders related to debt collection lawsuits can result in contempt of court charges.

3. What will happen if you ignore a debt collector?

A: Ignoring a debt collector can have consequences, including potential legal action. It's best to address the situation proactively and seek a resolution.

4. Can a debt collector garnish your wages?

A: In certain circumstances, a debt collector can obtain a court order to garnish your wages. The specific rules and limitations vary by jurisdiction.

5. How long can debt collectors legally pursue you?

A: The timeframe for debt collection lawsuits depends on the statute of limitations for your jurisdiction and the type of debt.

6. Can debt collectors contact your family members?

A: Debt collectors are generally prohibited from disclosing your debt to third parties. However, they may contact family members to obtain your contact information.

7. Can you be sued for credit card debt?

A: Yes, credit card debt can be subject to debt collection lawsuits if it remains unpaid.

8. How can you avoid being sued by a debt collector?

A: Promptly respond to debt collection notices, validate the debt, negotiate repayment plans, and seek legal advice if necessary.

9. Can debt collectors take your tax refund?

A: In some cases, debt collectors can intercept your tax refund to satisfy an outstanding debt. However, specific rules and limitations apply.

10. Should you hire an attorney if sued by a debt collector?

A: It's highly recommended to consult with an attorney if you're facing a debt collection lawsuit. They can provide legal guidance and help protect your rights.

*Bright customers paid off their credit card debt 4x faster using Bright membership than they would by only paying their minimum dues. These customers included all users using Bright before Feb 2023, having a minimum of $500 credit card debt, and having used Bright services for a year. Actual payoff rates may defer based on individuals.