You are now leaving the Bright website and entering a third-party website. Bright has no control over the content, products, or services offered, nor the security or privacy of information transmitted to others via their website. We recommend that you review the privacy policy of the site you are entering. Bright does not guarantee or endorse the products, information, or recommendations provided on any third-party website.

We've all been there: that heart-skip moment when you eagerly check your credit score, only to find it's taken an unexpected nosedive. It's a mix of surprise and concern, especially when you're not sure what's behind the drop.

Understanding the nuances of credit scores is vital for financial management and future planning. Today's discussion will revolve around those credit score fluctuations, offering tips to help you gain clarity and peace of mind.

How is Credit Score Calculated?

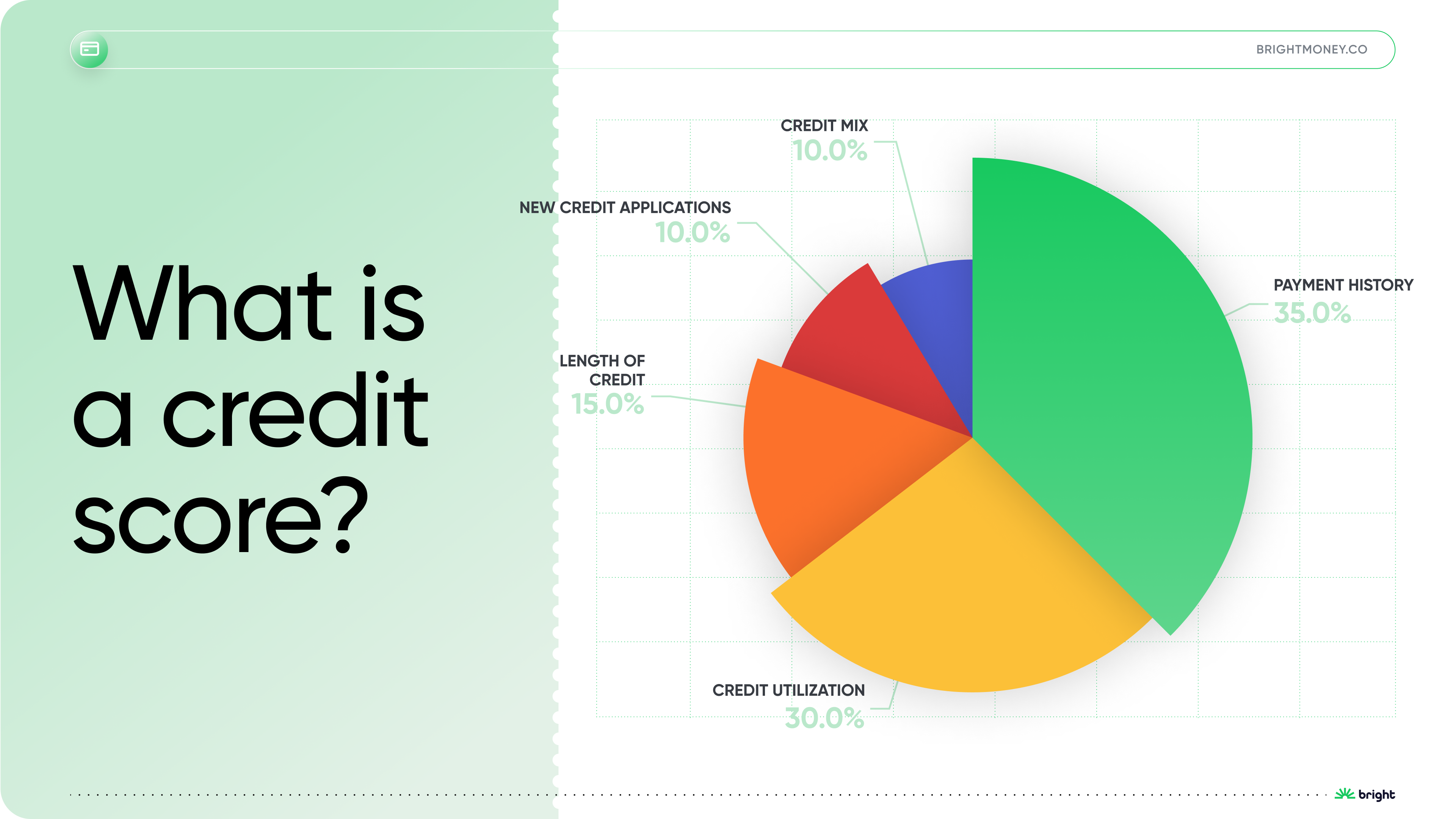

At the heart of your credit score lie five key pillars that determine its rise and fall:

- Payment History: Your track record of timely payments

- Credit Utilization: How much of your available credit you're using

- Length of Credit History: The age of your oldest and newest accounts

- New Credit: Recent credit inquiries and opened accounts

- Credit Mix: The variety of credit types you possess, from credit cards to mortgages

While these factors are universally recognized, it's worth noting that different credit bureaus might give them varied weights. The exact algorithms remain a well-guarded secret, but industry insiders have pieced together their significance over time.

Struggling with low credit scores? Explore how Bright Money can offer a flexible line of credit to manage your balances better.

Platforms to Check Your Credit Score:

- Credit Karma: A popular platform that offers free credit score checks and provides insights into what affects your score. They also offer credit monitoring and alerts

- Experian: One of the major credit bureaus, Experian offers both free and premium services. Their premium service provides a more in-depth look into your credit report and additional monitoring features

- Equifax: Another leading credit bureau, Equifax provides a comprehensive credit report along with your score. They also have monitoring services and identity theft protection

- TransUnion: This credit bureau offers a detailed credit report, credit score, and monitoring services. They also provide insights and recommendations to improve your score

- MyFICO: This platform provides scores from all three major bureaus. It's particularly useful for those looking to understand their FICO score, which is used by many lenders

What are Common Reasons for Credit Score Drops?

1. Late or Missed Payments

Payment history plays a pivotal role in determining your credit score. A single late payment, especially if it surpasses the 30-day mark, can lead to a noticeable drop in your score. The repercussions intensify with 60-day and 90-day late payments. Consistency in timely payments is crucial to maintain a healthy score.

2. High Credit Utilization

Credit utilization is the proportion of your current credit card balances to their respective credit limits. When this ratio climbs, particularly beyond the 30% threshold, it can be a warning sign of financial strain, leading to a dip in your credit score.

3. Closing Old Credit Cards

While it might seem like a step towards financial simplification, closing an old credit card can have unintended consequences. It reduces your overall credit availability, which can inadvertently hike your credit utilization ratio.

Additionally, it might shorten the length of your credit history, another vital component of your score.

4. Hard Credit Pull

Credit inquiries come in two flavors: soft and hard. While soft inquiries are benign, hard inquiries can chip away at your score. Multiple hard inquiries, like asking for multiple credit cards or loans in a short amount of time, can make lenders suspicious.

It's perceived as potential financial desperation. For a more detailed understanding of credit inquiries and their implications, Bright Money is here by your side. Check out our programs today!

5. Changes in Credit Mix

A diverse credit portfolio is appealing to lenders. They prefer to see a mix of credit types, from credit cards to auto loans. Adjusting this mix, either by opening or closing different types of accounts, can have a ripple effect on your score.

Lesser-Known Triggers for Credit Score Decline

Being aware of less obvious factors can equip individuals with the knowledge to manage and maintain a healthy credit score effectively. Some of them are listed below.

- Decrease in Credit Limit: A reduced credit limit can be initiated by lenders for various reasons, such as prolonged inactivity of an account or perceived increased risk. A lower limit can inadvertently raise the credit utilization ratio, negatively affecting the credit score.

- Taking on a Large Loan: Acquiring a significant loan, like a mortgage, can lead to a temporary decline in your credit score. This is due to the initial impact of new credit. However, with regular and timely payments, the score can recover and potentially improve.

- Unfamiliar Accounts or Charges: It's essential to routinely check credit reports. Any unfamiliar accounts or charges could indicate potential identity theft or fraud. Addressing these discrepancies promptly is crucial. For a comprehensive understanding of credit activities and their implications, Bright Money provides detailed insights.

Concerned about unfamiliar accounts affecting your score? Stay on top of your credit with Bright Money, your comprehensive solution to manage and wipe out debt.

What is the Role of Economic Factors and Lender Policies

Economic downturns often bring about a wave of caution in the lending world. Lenders, in their bid to mitigate risks, might tighten their belts by reducing credit limits or implementing more stringent lending criteria.

While these changes are aimed at safeguarding the lender's interests, they can inadvertently ripple down to individuals, manifesting as changes in their credit scores.

Moreover, the credit landscape is not static. Credit bureaus periodically refine their scoring models to capture a more accurate picture of an individual's creditworthiness. These updates aim for precision.

However, they can sometimes lead to unexpected score fluctuations for individuals. Staying informed and adapting to these shifts can help individuals navigate their credit journey with confidence.

How to Monitor and Address a Declining Credit Score

Tip #1: Regular Credit Report Checks

One of the first steps in credit management is staying informed. Every individual is entitled to a free annual credit report from each of the major credit bureaus. It's essential to review these reports meticulously. Spotting and disputing any discrepancies can prevent unwarranted score declines and protect against potential identity theft.

Tip #2: Setting Up Alerts

Real-time monitoring of credit activities has become more accessible than ever. Platforms like Bright Money offer tools that send instant alerts for significant changes in your credit profile. This proactive approach ensures you're always in the loop and can act swiftly if your score takes an unexpected dip.

Tip #3: Consulting with a Financial Advisor

While self-monitoring is crucial, some credit challenges might require expert intervention like Bright Money experts. If you're grappling with intricate issues like bankruptcy or tax liens, a financial advisor can provide tailored guidance. Their expertise can help you navigate the complexities and set you on a path to credit recovery. Simplify your journey with Bright Money debt builder programs today, tailored to your needs.

Tip #4: Maintaining Low Balances

A pivotal step in credit management is keeping your balances in check. Aim to clear off your dues monthly. If that's not feasible, strive to keep your balances below 30% of your credit limit. This not only boosts your score but also paints a picture of financial discipline to potential lenders.

Tip #5: Diversifying Credit Responsibly

A diverse credit portfolio can be a feather in your cap. However, it's essential to tread with caution. While different credit types can enhance your score, it's crucial not to take on debt without a clear purpose. Remember, responsible diversification is the key.

Conclusion

Credit scores, a numerical representation of one's financial responsibility, are influenced by a myriad of factors, from payment history to the type of credit utilized. It's imperative to grasp these determinants, as a robust credit score can pave the way for favorable financial opportunities, including preferential loan terms and competitive interest rates.

Proactively managing and monitoring one's credit can mitigate unforeseen declines and ensure optimal financial positioning.

For those seeking comprehensive and on-the-fly plans to enhance their financial trajectory, Bright Money has got you covered.

Suggested Readings

- How to increase your credit score by 100 points

- 5 Alternative Ways to Build Credit Before Turning 30

Frequently Asked Questions (FAQs)

- Can making a large purchase on a credit card cause my credit score to go down?

Yes, making a large purchase on a credit card can temporarily lower your credit score. It may increase your credit utilization ratio, which is the percentage of your available credit that you're using. A high utilization ratio can signal to lenders that you're over-reliant on credit, leading to a decrease in your score. It's often advisable to keep this ratio below 30% to maintain a healthy credit score.

- Why did my credit score drop after I paid off a loan?

Paying off a loan might unexpectedly cause a slight drop in your credit score. Closing an installment loan can reduce your credit mix, which is one of the factors credit bureaus consider.

Having a variety of credit types, such as credit cards, mortgages, and auto loans, can positively impact your score. Losing this diversity by paying off a loan might lead to a temporary dip in your score.

- Can checking my credit score too often cause it to go down?

Checking your credit score yourself, known as a soft inquiry, does not affect your credit score. However, if a lender or credit card issuer checks your credit as part of a lending decision, known as a hard inquiry, it may cause a small, temporary drop in your score.

Multiple hard inquiries in a short time can have a more significant impact, as they may signal to lenders that you are seeking excessive credit.

- Why did my credit score decrease even though I haven't made any significant financial changes?

Your credit score can decrease without significant financial changes due to various reasons. It might be related to a reporting error, an old account falling off your credit report, or changes in the credit scoring model.

Regularly monitoring your credit report and addressing any inaccuracies with the credit bureaus can help you understand and manage unexpected changes in your credit score.

If everything appears accurate, consulting with a credit expert might provide insights into the specific factors affecting your score.

References:

- https://www.creditkarma.com/credit/i/credit-score-drop#:~:text=Credit%20scores%20can%20drop%20due,applying%20for%20new%20credit%20accounts.

- https://www.experian.com/blogs/ask-experian/why-did-my-credit-score-drop/

- https://cred.club/check-your-credit-score/articles/why-is-my-credit-score-going-down-even-when-i-pay-on-time