You are now leaving the Bright website and entering a third-party website. Bright has no control over the content, products, or services offered, nor the security or privacy of information transmitted to others via their website. We recommend that you review the privacy policy of the site you are entering. Bright does not guarantee or endorse the products, information, or recommendations provided on any third-party website.

Debt consolidation is a financial strategy that aims to streamline multiple debts into a single, more manageable payment. This approach can help individuals regain control over their finances by combining various outstanding balances into a single loan with a potentially lower interest rate. While debt consolidation offers the promise of financial relief, many wonder how long debt consolidation takes.

But before we get into the topic, it is recommended that you read in detail about the best debt consolidation loans of 2023 by Bright Money!

In this comprehensive guide, we will explore the factors influencing the timeline of debt consolidation and provide insights into the process.

How Long Does Debt Consolidation Take?

On average, applying for and receiving approval for a debt consolidation loan can take 2 to 4 weeks.

Factors Affecting Debt Consolidation Timelines

- Type of Debt Consolidation Method:

Debt consolidation can be achieved through various methods, each with its own timeline. Common approaches include debt consolidation loans like Bright Credit by Bright Money, balance transfer credit cards, and debt management plans. Debt consolidation loans typically involve applying for a new loan to pay off existing debts, and the approval and disbursement process can take several weeks. On the other hand, balance transfer credit cards may offer quicker results, as the transfer of balances can occur within a few weeks. Debt management plans, facilitated by credit counseling agencies, involve negotiations with creditors and may take several years to complete.

- Creditworthiness:

An individual's creditworthiness plays a significant role in determining the speed of the debt consolidation process. Those with a higher credit score are more likely to qualify for favorable loan terms and lower interest rates. Lenders may require time to assess an applicant's credit history, income, and overall financial situation before approving a consolidation loan.

- Documentation and Verification:

The documentation and verification process can impact the speed of debt consolidation. Lenders may require various documents, such as proof of income, credit reports, and information on existing debts. Delays can occur if the documentation is not provided promptly or if additional verification steps are necessary.

- Negotiations with Creditors:

The negotiation process with creditors can influence the overall timeline for individuals opting for debt management plans. Creditors may need time to review proposals and agree to modified repayment terms. Additionally, the coordination between the credit counseling agency and creditors may introduce delays.

- Individual Commitment and Discipline:

The effectiveness of debt consolidation is also contingent on an individual's commitment and discipline. Adhering to the agreed-upon repayment plan, budgeting wisely, and avoiding new debt is essential for successful consolidation. The timeline may be prolonged if individuals deviate from the plan or encounter financial setbacks during consolidation.

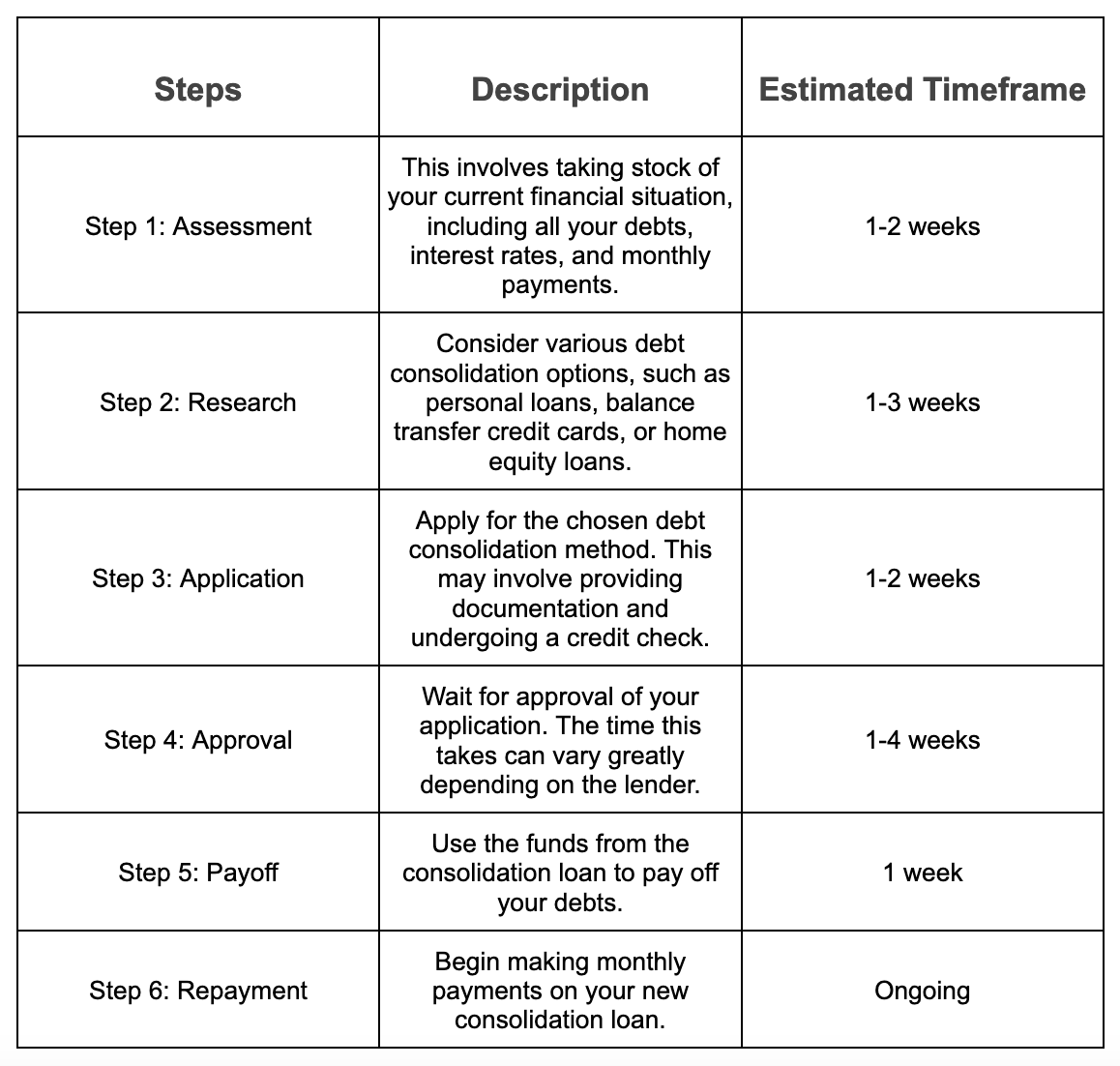

Steps Involved in Debt Consolidation and Their Timeframes

- Assessment and Planning (1-2 weeks):

The debt consolidation journey often begins with a comprehensive assessment of an individual's financial situation. This involves gathering information on existing debts, interest rates, and monthly payments. After evaluating the available consolidation options, individuals can formulate a debt repayment plan. This stage typically takes one to two weeks, depending on the complexity of the financial situation.

- Application and Approval (1-3 weeks):

The next step for those pursuing debt consolidation loans involves submitting applications to potential lenders. The approval process can take two to four weeks and includes thoroughly examining the applicant's creditworthiness, income, and overall financial health. During this time, lenders may request additional documentation for verification purposes.

- Disbursement of Funds (1-2 weeks):

Once the debt consolidation loan is approved, the funds are disbursed to pay off existing debts. This process generally takes one to two weeks, and the timing may vary depending on the lender's policies and procedures.

- Implementation of Balance Transfer (1-4 weeks):

Individuals opting for balance transfer credit cards will initiate the transfer of balances from existing credit cards to the new card. This process can take two to four weeks, including the time required for the new credit card issuer to process the transfers.

- Credit Counseling and Negotiations (1 week):

Debt management plans, facilitated by credit counseling agencies, involve negotiations with creditors to establish modified repayment terms. The duration of this stage varies depending on the responsiveness of creditors and the complexity of the negotiations. It can range from a few weeks to several months.

- Consistent Repayment (Ongoing):

The success of debt consolidation hinges on consistent and disciplined repayment. Individuals must adhere to the agreed-upon repayment plan, making timely payments to the new consolidation loan or credit card. The duration of this stage is ongoing and may last several months or years, depending on the terms of the consolidation plan.

Tips to Expedite Debt Consolidation:

1. Organize Financial Documents:

Importance: Well-organized financial documents are crucial for a smooth and speedy debt consolidation process.

Impact: Ready access to documents like income statements, loan agreements, credit reports, and other financial records can expedite the application process.

Action Steps:

- Gather all necessary documents in advance.

- Keep them organized and readily accessible when applying for a consolidation loan or balance transfer.

- Ensure all information is accurate and up-to-date to prevent delays or rejections.

2. Maintain Good Credit:

Importance: A higher credit score significantly influences the approval process and the terms lenders offer.

Impact: Good credit demonstrates financial responsibility, increasing the likelihood of quicker approval and more favorable consolidation terms.

Action Steps:

- Regularly monitor your credit score through reputable credit bureaus.

- Make timely payments on existing debts to maintain or improve your credit score.

- Rectify any errors on your credit report promptly to ensure accuracy.

3. Compare Lenders:

Importance: Different lenders offer varying terms, interest rates, and processing times for debt consolidation.

Impact: Researching and comparing multiple lenders allows you to find the most suitable one that offers favorable terms and quicker processing.

Action Steps:

- Research and compare lenders, including banks, credit unions, online lenders, and financial institutions.

- Consider factors like interest rates, fees, repayment terms, and customer reviews.

- Request quotes or pre-qualifications from multiple lenders to gauge the best options available.

4. Stay Informed:

Importance: Effective communication and staying updated with your lender are key to ensuring a smooth consolidation process.

Impact: Regular communication helps address potential issues or delays, keeping the process on track and efficient.

Action Steps:

- Maintain regular contact with your lender throughout the application and approval process.

- Clarify any doubts or questions about the consolidation terms or requirements.

- Promptly respond to any requests or queries from the lender to avoid delays.

Conclusion

In conclusion, the timeline for debt consolidation varies based on multiple factors, including the chosen method, creditworthiness, and negotiations with creditors. The process involves distinct stages, from assessment and planning to the ongoing commitment to a structured repayment plan. While debt consolidation offers numerous benefits, individuals should carefully weigh the potential challenges and risks before embarking on this financial journey.

Individuals can take meaningful steps toward achieving lasting financial stability by understanding the intricacies of debt consolidation and adopting responsible financial habits.

Transform your finances with Bright Money's powerful tools like Bright Credit and Bright Builder! Take control of your finances by downloading the Bright Money app.

Must Read:

3 reasons to use personal loans to pay off debt

Can I get a Debt Consolidation Loan with a 580 Credit Score?

FAQs

- Does the size of my debt impact the time it takes for consolidation?

Yes, the amount of debt you have can influence the duration of consolidation. Larger amounts of debt involve more documentation, evaluation, and longer negotiations with creditors, extending the overall consolidation timeline.

- Can my credit score affect the speed of debt consolidation?

Absolutely. A higher credit score often expedites the approval process for a consolidation loan or balance transfer card. A strong credit history may qualify you for better interest rates and terms, streamlining the consolidation process.

- Are there faster alternatives to traditional debt consolidation methods?

Yes, some methods offer quicker solutions. For instance, balance transfer credit cards can swiftly consolidate credit card debt by transferring balances to a new card with a lower interest rate, potentially taking a few weeks to complete.

References