You are now leaving the Bright website and entering a third-party website. Bright has no control over the content, products, or services offered, nor the security or privacy of information transmitted to others via their website. We recommend that you review the privacy policy of the site you are entering. Bright does not guarantee or endorse the products, information, or recommendations provided on any third-party website.

Debt can be overwhelming, impacting one’s financial stability and mental well-being. For those struggling with substantial debt, finding a solution becomes paramount. Two common approaches are debt consolidation and bankruptcy. Both aim to provide relief from debt, but they differ significantly in their mechanisms, implications, and long-term effects. According to a report, the average credit card debt per household with revolving credit was around $7,600.

But before we get into the topic, it is recommended that you read in detail about the best debt consolidation loans of 2023 by Bright Money!

This article will discuss whether debt consolidation is the same as bankruptcy and advise you on when to choose it!

Is Debt Consolidation The Same As Bankruptcy

No, debt consolidation and bankruptcy are not the same. Debt consolidation involves combining multiple debts into a single payment, often with a lower interest rate. On the other hand, bankruptcy is a legal process that involves either restructuring debts (Chapter 13) or discharging them (Chapter 7) under court supervision.

Debt Consolidation: An Overview

Debt consolidation involves merging multiple debts into a single loan, often with a lower interest rate. This method simplifies repayment by combining various debts like credit card balances, personal loans, or medical bills into one monthly payment. Borrowers can choose between different consolidation methods:

1. Consolidation Loans

This method involves taking out a new loan to pay off existing debts. It allows borrowers to manage their debt more effectively with a single payment and potentially lower interest rates. Bright Credit by Bright Money offers Debt consolidation loans and helps you rebuild your credit while paying off debt!

2. Balance Transfer Credit Cards

Another approach is transferring high-interest credit card balances to a single card with a lower interest rate or a 0% introductory rate for a specified period. This can save on interest payments during the promotional period.

3. Home Equity Loans or Lines of Credit

Homeowners may use the equity in their property to consolidate credit card debts. This method offers lower interest rates but risks the property if the borrower defaults.

Pros of Debt Consolidation

- Simplified Repayment: Consolidating debts streamlines payments into one, making it easier to manage finances.

- Potentially Lower Interest Rates: A consolidation loan or balance transfer card can offer reduced interest rates, saving money over time.

- Preservation of Credit Score: As long as payments are made on time, consolidation may positively impact credit scores.

Cons of Debt Consolidation

- May Require Collateral: Some methods, like home equity loans, require collateral, risking assets if payments are missed.

- Not Suitable for Everyone: Those with poor credit or excessive debt might struggle to qualify for favorable consolidation terms.

- Potential for Prolonged Repayment: Extending repayment terms can mean paying more interest over time.

Bankruptcy: An Overview

- Chapter 7 Bankruptcy (Liquidation):

In Chapter 7 bankruptcy, assets not protected by exemptions are sold to repay creditors, offering a fresh start by eliminating eligible debts. Certain assets, like primary residences, are exempt from liquidation, but non-exempt assets may be sold. However, some debts like taxes and student loans are typically not dischargeable.

- Chapter 13 Bankruptcy (Reorganization):

Chapter 13 bankruptcy allows individuals to reorganize debts into a manageable repayment plan spanning three to five years. Debtors can retain assets while repaying some of their debts according to a court-approved plan. This option suits those with regular income who want to protect assets while gradually eliminating debts.

Pros of Bankruptcy

- Immediate Debt Relief: Bankruptcy offers a swift resolution to overwhelming debt, providing relief from creditors' actions.

- Legal Protection: Bankruptcy comes with an automatic stay, preventing creditors from pursuing collection activities.

- Fresh Financial Start: Dischargeable debts are eliminated, allowing a chance to rebuild credit and finances.

Cons of Bankruptcy

- Long-Term Impact on Credit: Bankruptcy remains on credit reports for several years, affecting the ability to secure credit or loans. According to a report, individuals might see a drop of 130 to 240 points in their credit score after bankruptcy.

- Loss of Assets: Chapter 7 bankruptcy may involve liquidating non-exempt assets to repay creditors.

- Complex Legal Process: Bankruptcy involves legal procedures and associated fees, making it complex and costly.

Choosing Between Debt Consolidation and Bankruptcy

Debt Consolidation

Bankruptcy

When Debt Consolidation Might Be the Right Choice:

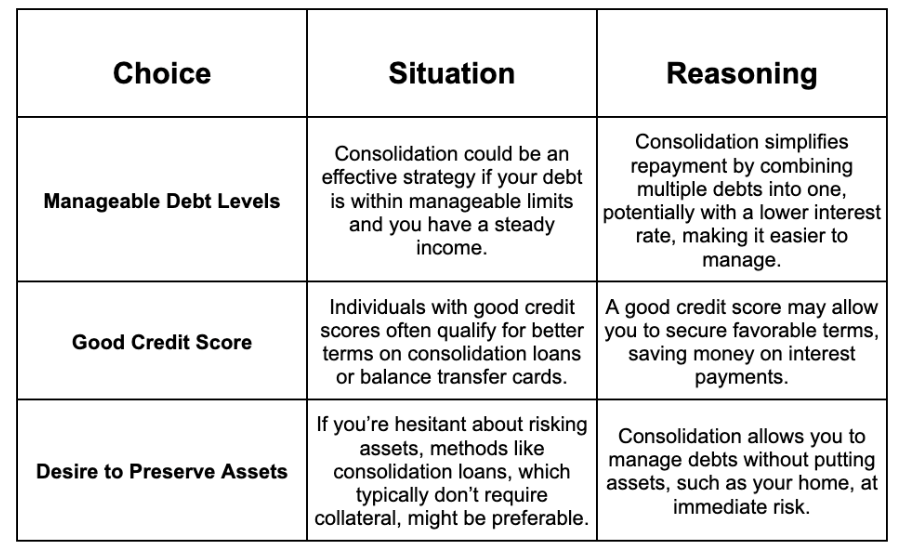

1. Manageable Debt Levels:

Situation: If your debt is within manageable limits and you have a steady income, consolidation could be an effective strategy.

Reasoning: Consolidation simplifies repayment by combining multiple debts into one, potentially with a lower interest rate, making it easier to manage.

2. Good Credit Score:

Situation: Individuals with a good credit score often qualify for better terms on consolidation loans or balance transfer cards.

Reasoning: A good credit score may allow you to secure favorable terms and save money on interest payments.

3. Desire to Preserve Assets:

Situation: If you're hesitant about risking assets, methods like consolidation loans, which typically don't require collateral, might be preferable.

Reasoning: Consolidation allows you to manage debts without putting assets, such as your home, at immediate risk.

When Bankruptcy Might Be the Right Choice:

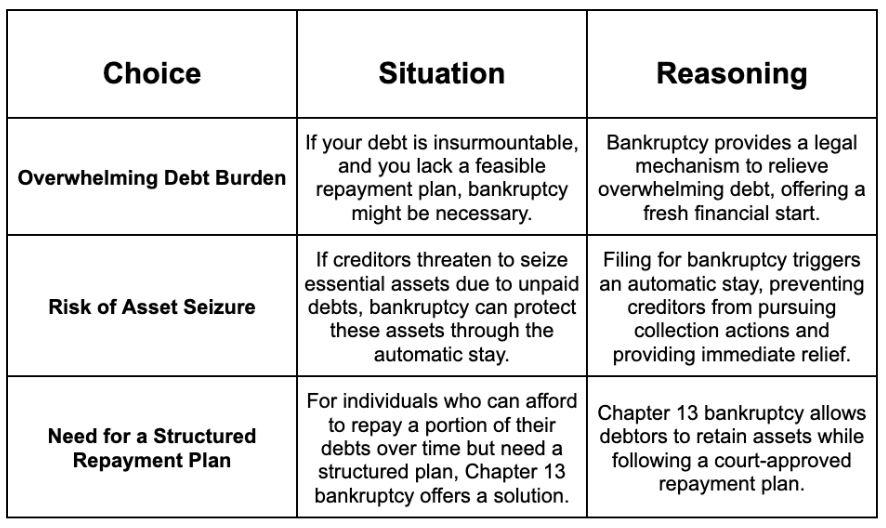

1. Overwhelming Debt Burden:

Situation: If your debt is insurmountable, and you lack a feasible repayment plan, bankruptcy might be necessary.

Reasoning: Bankruptcy provides a legal mechanism to relieve overwhelming debt, offering a fresh financial start.

2. Risk of Asset Seizure:

Situation: If creditors threaten to seize essential assets due to unpaid debts, bankruptcy can protect these assets through the automatic stay.

Reasoning: Filing for bankruptcy triggers an automatic stay, preventing creditors from pursuing collection actions and providing immediate relief.

3. Need for a Structured Repayment Plan:

Situation: For individuals who can afford to repay a portion of their debts over time but need a structured plan, Chapter 13 bankruptcy offers a solution.

Reasoning: Chapter 13 bankruptcy allows debtors to retain assets while following a court-approved repayment plan.

Conclusion

Choosing between debt consolidation and bankruptcy depends on individual financial circumstances. Debt consolidation offers a way to streamline payments and lower interest rates suited for those with manageable debt levels. On the other hand, bankruptcy provides immediate relief for those facing overwhelming debt or potential asset loss, but it comes with long-term credit implications.

Before deciding, seeking advice from financial advisors or credit counselors can provide valuable insights into the best course of action based on one's financial situation and goals.

Must Read

Does Credit Card Consolidation hurt your credit score?

Can I get a Debt Consolidation Loan with a 580 Credit Score?

FAQs

1. How does debt consolidation affect my credit score compared to bankruptcy?

Debt consolidation typically has a less severe impact on credit scores than bankruptcy. With consolidation, your credit may initially dip due to a new loan or credit inquiry, but it can gradually improve with timely payments. On the other hand, bankruptcy significantly lowers credit scores and remains on credit reports for several years.

2. Which option provides faster relief from debt: debt consolidation or bankruptcy?

Debt consolidation offers quicker relief since it immediately combines multiple debts into one, simplifying repayment. Bankruptcy, especially Chapter 7, offers swift relief by discharging eligible debts within a few months, but Chapter 13 involves a longer-term repayment plan.

3. Can I apply for debt consolidation if I've already filed for bankruptcy?

Yes, it's possible to pursue debt consolidation after bankruptcy. However, securing new credit, such as a consolidation loan or balance transfer card, might be challenging immediately after bankruptcy due to the impact on credit scores and financial history.

References