You are now leaving the Bright website and entering a third-party website. Bright has no control over the content, products, or services offered, nor the security or privacy of information transmitted to others via their website. We recommend that you review the privacy policy of the site you are entering. Bright does not guarantee or endorse the products, information, or recommendations provided on any third-party website.

Credit scores are the backbone of financial decisions, acting as a numerical summary of your creditworthiness. Among various credit scoring models, the FICO score stands out as the standard used by 90% of top lenders. In a nutshell, the FICO score is a nuanced tool considering various aspects of your financial behavior. It's not just about what you owe but how you manage it, the types of debts you have, and your recent financial actions. Moreover, there's more on the topic today, and understanding all these unique attributes can empower you to take control of your finances even better. Let's dig deep.

What Is the Genesis of the FICO Score?

The genesis of the FICO score began with the founding of the Fair Isaac Corporation by William Fair and Earl Isaac in 1956. Their mission was to create credit risk models for financial services, bringing a scientific approach to credit evaluation. But why was this needed? Before FICO, there was fragmentation in credit scoring methods.

The financial world was craving a standardized, unbiased credit evaluation system. The creation of the FICO scoring system was a turning point, setting a new standard that continues to shape the financial landscape today.

What Is the FICO Score Range and Why Is It Important?

The FICO score ranges from 300 to 850, categorized into:

- Poor (300-579)

- Fair (580-669)

- Good (670-739)

- Very Good (740-799)

- Excellent (800-850).

This score determines loan eligibility, interest rates, and even insurance premiums. Looking to manage your credit more effectively? Bright Credit offers flexibility in payments, allowing you to balance transfers as you pay down and maintain good to excellent scores. Discover more here.

What Factors Determine Your FICO Score?

FICO score is a summary of how you've managed your financial responsibilities. By knowing what factors influence your score and how they're weighted, you can take control of your finances. Here’s a complete rundown:

- Payment History (35%): This includes on-time payments, late payments, and collections. Paying on time shows you're reliable

- Amounts Owed (30%): This covers the total debt and credit utilization ratio, with the idea being below 30%. It's about managing what you owe

- Length of Credit History (15%): This considers the average age of accounts and the oldest account. It's a glimpse into your financial experience

- New Credit (10%): This includes recent credit inquiries and new accounts. It's about how you're expanding your credit landscape

- Types of Credit Used (10%): This looks at the mix of credit cards, mortgages, and installment loans. It's about diversifying your credit portfolio

What Are the Unique Attributes of the FICO Score?

The FICO score is not just a generic credit rating; it has unique attributes that set it apart. Here's a closer look:

- Credit utilization: This parameter carries a 30% weight in the FICO score. It's about how much of your available credit you're using. A high ratio can signal perceived risk, potentially lowering your score. Managing this aspect is crucial.

- Diversity in Debts: FICO distinguishes between revolving debts like credit cards and installment debts like mortgages and auto loans. Different debts have different impacts on creditworthiness. Understanding this can help you manage your debts more effectively. If you are looking to leave the stress bags of debt management for an improved credit score, Bright Money has got you covered! Check out our Bright Builder program today!

- Financial Behavior: Recent financial behavior matters. Recent credit applications, known as hard inquiries, can affect your score. Recent payments, whether on time or late, also play a role in shaping your payment history.

How Has the FICO Score Evolved Over Time?

The FICO score has seen significant evolution since its inception, adapting to the changing financial landscape and consumer behaviors.

One of the most notable changes came with FICO Score 9, where medical debt became less influential, reflecting the understanding that medical debt doesn't necessarily indicate financial irresponsibility. Additionally, rent payments started to be considered, providing a more comprehensive view of financial behavior.

The journey from the original model to FICO Score 9 also saw changes in weightings and the treatment of unpaid collections. These adjustments have made the scoring model more nuanced and aligned with modern financial practices.

Navigating through the complexities of evolving credit scores? Bright Debt Plan offers everything you need to manage and wipe out debt. Get started on your journey to financial freedom here.

The evolution in credit scores can be overwhelming. Explore your financial journey with Bright Debt Plan, the comprehensive solution to manage and eliminate debt. Start here

Why Do Lenders Rely on the FICO Score?

Lenders gravitate towards the FICO score for its predictive accuracy. It offers a consistent measure across lenders, allowing for a standardized evaluation of credit risk. This consistency has led to widespread adoption by major financial institutions, making it a trusted tool in the lending process.

Furthermore, lenders trust FICO, but managing multiple credit cards can be challenging. Explore Bright Money's credit card solutions to streamline your finances here.

Influence over loan approvals and interest rates

The FICO score plays a vital role in risk assessment. Higher scores indicate lower risk, often leading to favorable loan terms and interest rates. Conversely, lower scores may result in higher interest rates or even loan denial.

The FICO score provides a reliable and efficient way to assess creditworthiness. It's a bridge between lenders and borrowers, facilitating understanding and trust. Whether you're seeking a mortgage, auto loan, or credit card, the FICO score is often the key that unlocks those financial doors.

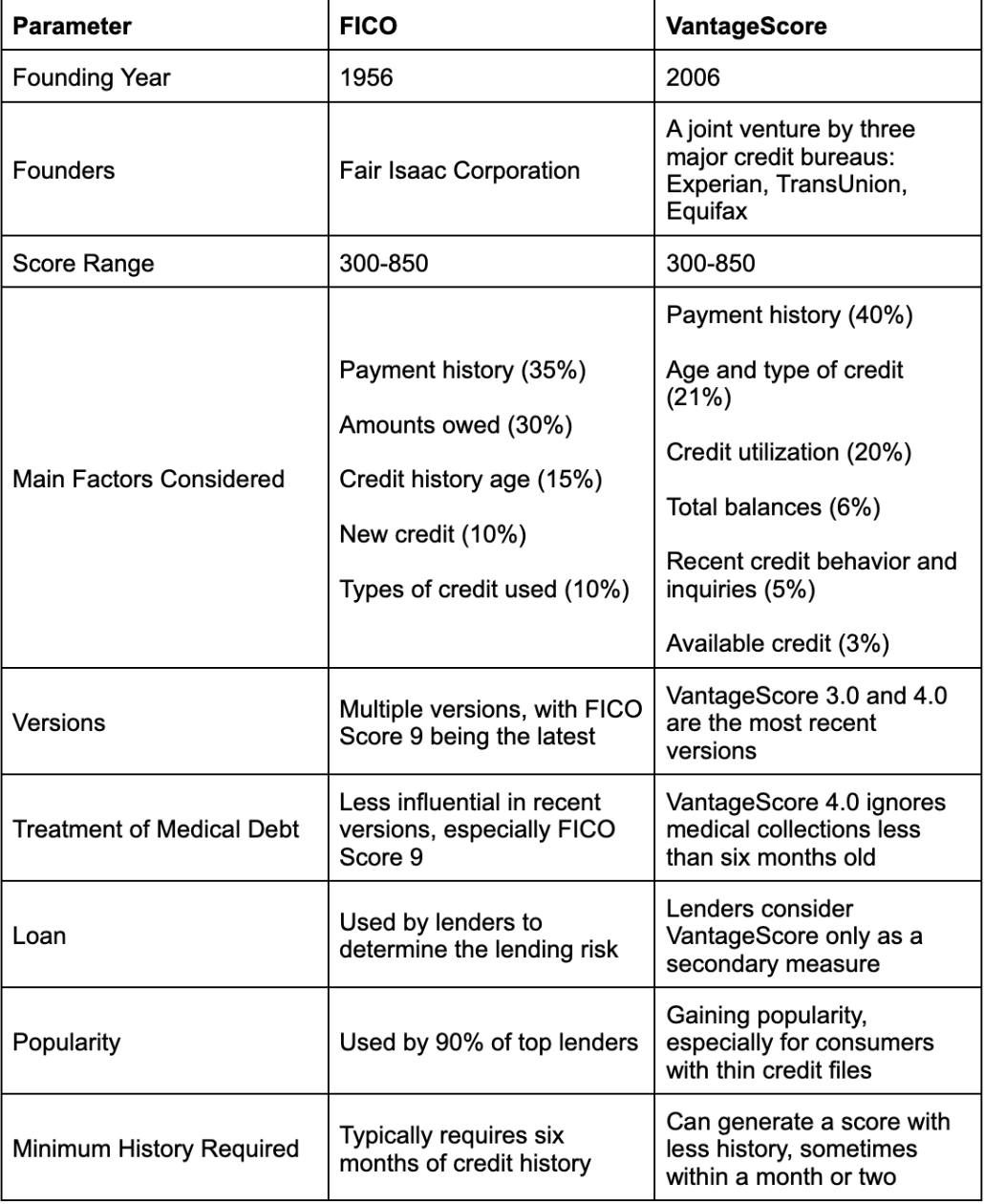

How Does the FICO Score Compare to Other Scoring Models?

While both FICO and VantageScore operate within the same range (300-850), they differ in several ways.

Moreover, FICO's legacy, trust, and specific methodologies set it apart. Its long-standing reputation and precise approach to credit scoring have made it a go-to for financial institutions.

While other models like VantageScore offer alternatives, FICO's position in the credit industry remains strong and superior in present times. No matter which credit score you are planning to improve, or even if you both, you can ease it with Bright Money’s personalized offerings tailored to your unique situation. Start improving your score today.

How Can You Access and Interpret Your FICO Score?

Finding your FICO score is easier than ever. Many banks and credit card issuers provide it for free as a part of their service.

If you want a more detailed analysis, there are paid services that offer comprehensive reports. It's not hidden away; it's right there for you to access, helping you keep tabs on your financial health. You can check your score on Experian, Equifax, or TransUnion.

How Can You Understand Your FICO Score Breakdown?

To understand it, you'll want to look at its components, such as payment history, credit utilization, and the length of credit history. Knowing what each part means and how it impacts your overall score can guide you in making smarter financial decisions.

There are guides available that break down these elements, offering strategies to improve areas where you might be lagging.

By knowing where to find it and how to interpret what it's telling you, you're taking an essential step in managing your financial life. It's not a mystery; it's a tool, and it's there for you to use.

Conclusion

The FICO score stands unparalleled in the credit scoring landscape due to its continuous innovation, pinpoint accuracy, and the trust it has garnered within the industry.

Understanding your FICO score opens doors to loan opportunities and empowers you to manage your credit with confidence. Understanding your FICO score is the first step toward better financial decisions. Ready to take control of your financial future? Discover all the solutions Bright Money offers to guide you on your journey.

Stay informed about your FICO score – it's more than a number. It's a key to unlocking your financial potential and a pathway to achieving your financial goals.

Further reading

FAQs

- How does marital status influence the FICO score?

While marital status itself doesn't directly impact your FICO score, the financial behaviors and decisions that sometimes accompany marriage can. For instance, if spouses become co-signers or joint account holders, the financial habits of one can affect the credit report of the other.

- How does the mix of credit types influence the FICO score?

While much emphasis is placed on payment history and credit utilization, the variety of credit types you have (credit cards, retail accounts, installment loans, mortgages, etc.) makes up about 10% of your FICO score. Having a diverse mix can be beneficial, as it shows lenders you can handle different types of credit responsibly. However, it's not advisable to take on unnecessary credit just to diversify.

- Do medical debts have a unique impact on the FICO score?

Medical debts are treated a bit differently. Recognizing the often unexpected nature of medical expenses, newer FICO models (like FICO Score 9) give less weight to unpaid medical collections compared to other types of collections. Furthermore, there's typically a grace period before medical debts appear on your credit report, giving individuals time to resolve any insurance disputes or payment issues.