You are now leaving the Bright website and entering a third-party website. Bright has no control over the content, products, or services offered, nor the security or privacy of information transmitted to others via their website. We recommend that you review the privacy policy of the site you are entering. Bright does not guarantee or endorse the products, information, or recommendations provided on any third-party website.

Dealing with multiple debts can feel like being in a maze with no clear exit. Each debt, whether it's a credit card, student loan, or car loan, comes with its own set of rules – different interest rates, due dates, and payment amounts.

The question arises: is consolidating these debts into a personal loan a wise choice?

Debt consolidation through a personal loan can simplify your financial obligations into one manageable payment. However, it's not a universal solution.

The effectiveness of this strategy depends heavily on individual financial situations, the types of debt you have, and your ability to maintain financial discipline.

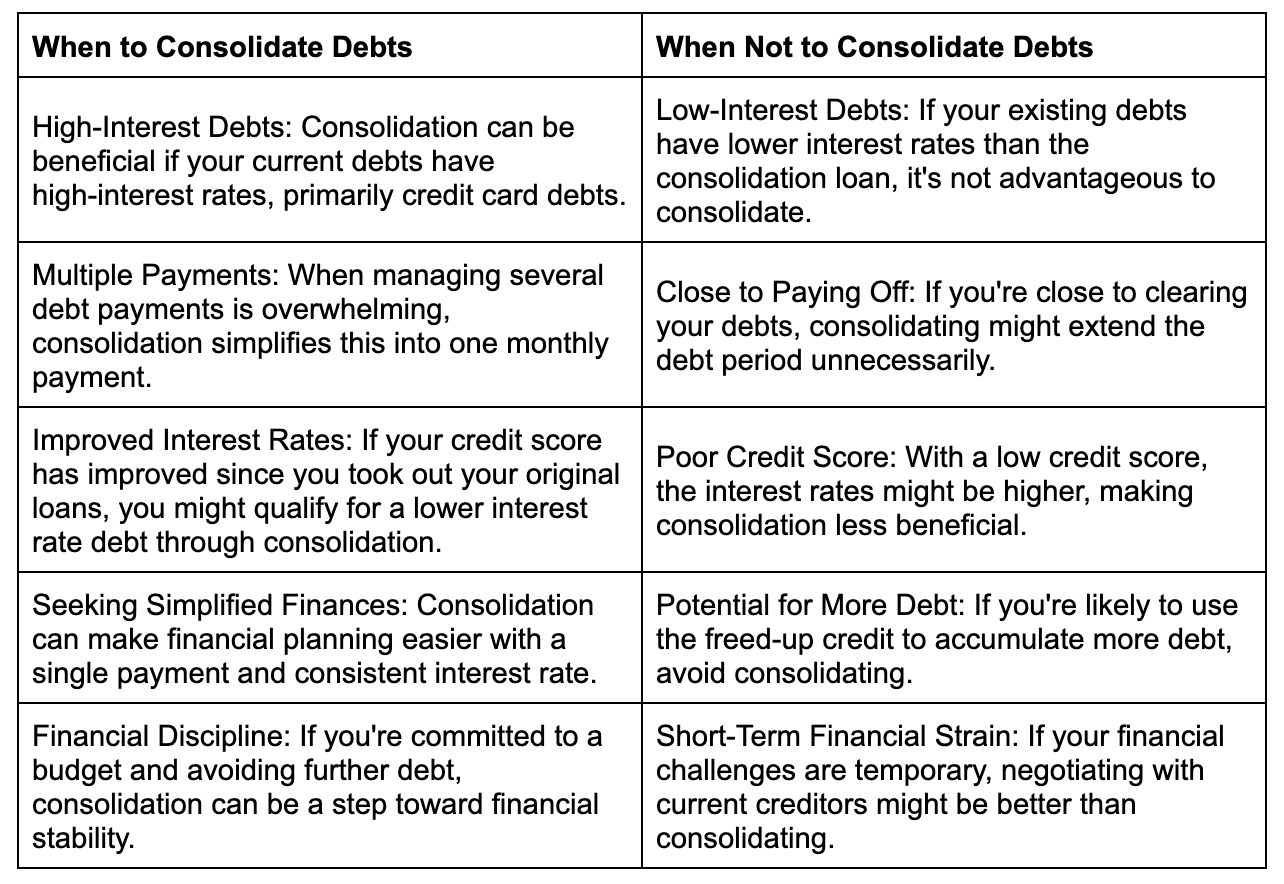

When should you consolidate your debts in a personal loan, and when not?

When considering consolidating your debts into a personal loan, it's important to weigh the pros and cons based on your financial situation. Not all scenarios are suited for applying to debt consolidation, and what works for one person might not be the best choice for another.

To help you decide, let’s look at a straightforward comparison.

Things to Keep in Mind While Consolidating Your Debts into Personal Loans

1. Personal loans can be a tool for debt consolidation

A personal loan allows individuals to pay off multiple smaller debts, leading to a single monthly payment. This simplification can result in more manageable financial planning and potentially lower overall interest payments.

2. Ensure that the loan's interest rate is lower than the rates on your current debts.

Be mindful of the loan's repayment terms, as longer durations could result in paying more interest over time. Always check for any origination fees or prepayment penalties.

3. Consolidating debts can temporarily impact your credit score.

Choosing a reputable lender is crucial to avoid any hidden terms or unethical practices. Additionally, maintain an emergency fund for unexpected expenses and thoroughly understand all terms and conditions of the loan agreement before committing.

What will happen if you consolidate your debts into a personal loan?

When you consolidate your debts into a personal loan, several things happen.

- Combining Debts: All your different debts, like credit card bills and student loans, get merged into one single loan. This is like putting all your eggs in one basket, making it easier to keep track.

- One Monthly Payment: Instead of dealing with multiple payments at different times, you'll only have one payment to remember. It's like having one bill to pay instead of several.

- Lower Interest Rate: Generally, the interest rate on a consolidated loan is lower than your original debts. This is like swapping expensive loans for cheaper ones, potentially saving you money over time.

- Longer Repayment Period: While your monthly payments might be lower, the time you take to pay off the loan could be longer. This means you might pay more in total interest.

- Short-Term Credit Score Impact: Your credit score might initially dip a bit due to the lender's credit check. It's a temporary effect as you start this new financial journey.

- Long-Term Credit Improvement: If you consistently make on-time payments. This shows you're managing your debt well.

How to consolidate debts into a personal loan

Step 1 - Evaluate Your Total Debt: Add up all your current debts, including credit cards, car loans, student loans, etc. This gives you a clear picture of what you owe in total.

Step 2 - Check Your Credit Score: Obtain your credit score to understand your eligibility for a personal loan. A higher score usually means better loan terms, like lower interest rates.

Step 3 - Compare Loan Options: Research different lenders and their personal loan terms. Focus on interest rates, loan duration, and any additional fees. This step is crucial for finding a loan that will save you money compared to your current debts.

Step 4 - Apply for a Personal Loan: Once you've chosen a lender, apply for a personal loan. Be prepared to provide financial documents and personal information.

Step 5 - Use the Loan to Pay Off Debts: Use the loan funds to pay off your debts faster if approved. This consolidates your multiple debts into one loan with a single monthly payment.

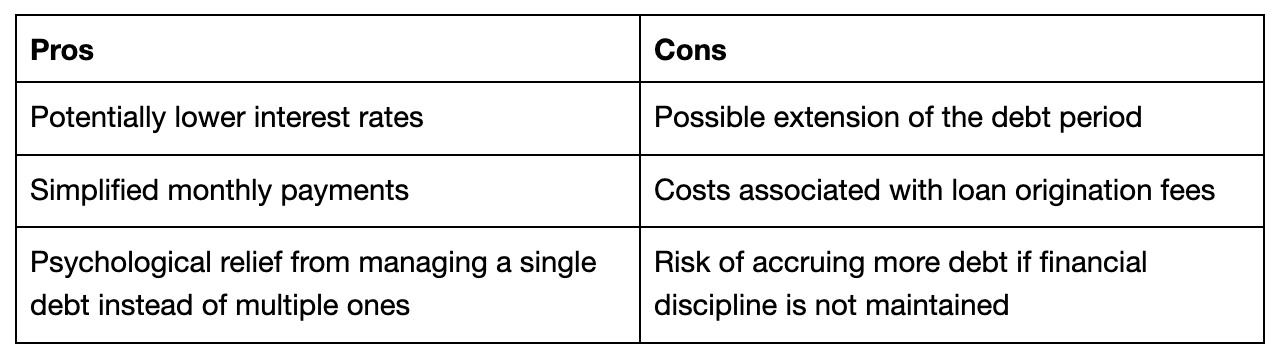

Pros and Cons of Debt Consolidation

Conclusion

Consolidating your debts into a personal loan can be a smart strategy. Still, it requires careful thought and disciplined financial management.

Moving forward, it's essential to maintain a budget that accommodates your new loan payment while addressing your other financial goals. Avoid accumulating new debt; the purpose of consolidation is to simplify and reduce your debt, not to create room for more.

Debt consolidation is a tool to help you regain control over your finances, but its success largely depends on your commitment to responsible spending and consistent payment habits. Stay focused on your long-term financial health, and use this opportunity to build a more secure financial future. Discover how Bright Money's smart technology and personalized approach can accelerate your path to financial freedom. Visit us now!"

Suggested readings

- Why loans don’t always work for debt consolidation

- Are Personal Loans a good option for Debt Consolidation?

- 14 Debt Pay-Off Tips You Can't Miss!

FAQs

1. Consolidating Debt vs. Paying Off Individually

Deciding between consolidating credit card debt and other loans or paying them off individually depends on your financial situation. Consolidation simplifies payments and may lower interest rates but often extends the repayment period, potentially increasing the total interest paid. Individual payments might be better for quickly clearing high-interest debts, provided you can manage multiple accounts effectively.

2. Disadvantages of Debt Consolidation

A significant downside to debt consolidation is the potential extension of your debt period, leading to more interest over time. Securing a consolidation loan might result in less favorable terms for those with bad credit. Additionally, loan agreements may include fees that increase overall costs.

3. Impact of Personal Loans on Credit

While a debt consolidation loan can initially lower your credit score due to the lender's credit check, it can improve your credit profile long-term. Consolidation can reduce credit utilization and streamline payment history. Still, it's crucial to use the loan responsibly and ensure all existing debts are paid off.

4. Debt Consolidation and Credit Score

Consolidating debt can drop your credit score slightly due to the required credit inquiry. However, if it leads to more disciplined debt management and reduced credit utilization (especially with credit card debt), it can positively affect your credit score. The improvement hinges on avoiding new debt accumulation during repayment.

5. Debt Consolidation vs. Debt

Debt consolidation combines multiple debts, like credit card debts, into one loan with potentially better terms to simplify repayment and reduce total interest. In contrast, 'debt' refers to the borrowed money itself. Consolidation is a strategy to re-organize debt, not an additional financial obligation.

References

- https://www.forbes.com/advisor/personal-loans/pros-and-cons-of-debt-consolidation/

- https://www.investopedia.com/terms/d/debtconsolidation.asp

- https://www.bankbazaar.com/personal-loan-for-debt-consolidation.html

- https://www.investopedia.com/terms/d/debtconsolidation.asp

Disclaimer: For debt pay-off related: Bright credit is a line of credit that can be used to pay off your credit cards. Subject to credit approval. Variable APR ranges from 9% to 24.99%, and credit limit ranges from $500 to $8,000. Apr will vary based on prime rates. Final terms may vary depending on credit review. Monthly minimum payments are as low as 3% of the outstanding principal balance plus the accrued interest. Also, you can pay more than the minimum due if you want to pay down the loan faster. The credit line originated by Bright or CBW Bank, a member of FDIC. Products and services are subject to state residency and regulatory requirements. Bright credit is currently not available in all states.