.jpg)

You are now leaving the Bright website and entering a third-party website. Bright has no control over the content, products, or services offered, nor the security or privacy of information transmitted to others via their website. We recommend that you review the privacy policy of the site you are entering. Bright does not guarantee or endorse the products, information, or recommendations provided on any third-party website.

Having a good credit score in today’s world gives you just the edge you need to be one step ahead of your peers. Especially, if you are somebody willing to build and improve your credit score one step at a time. Your effort will pay off when you see how it will positively impact your financial well-being in the future.

You will need a car loan, a credit card, or a mortgage at some point in life. Lenders will assess your credit score first to determine your creditworthiness. If you have good credit, it opens up many opportunities for you.

Positive financial habits and discipline are what it takes to build and maintain a strong credit score. It is a gradual process and does not happen overnight.

The Significance of Your Credit Score represents your creditworthiness numerically. This score usually will range from 300 to 850 based on your financial behavior and credit history. Lenders will use this score to determine the risk of giving you credit. The higher your score, the lower the risk, that is how lenders will see it. Thus, making it easy for you to qualify for loans or credit cards with favorable interest rates.

The Power of Financial Habits on Your Credit Score

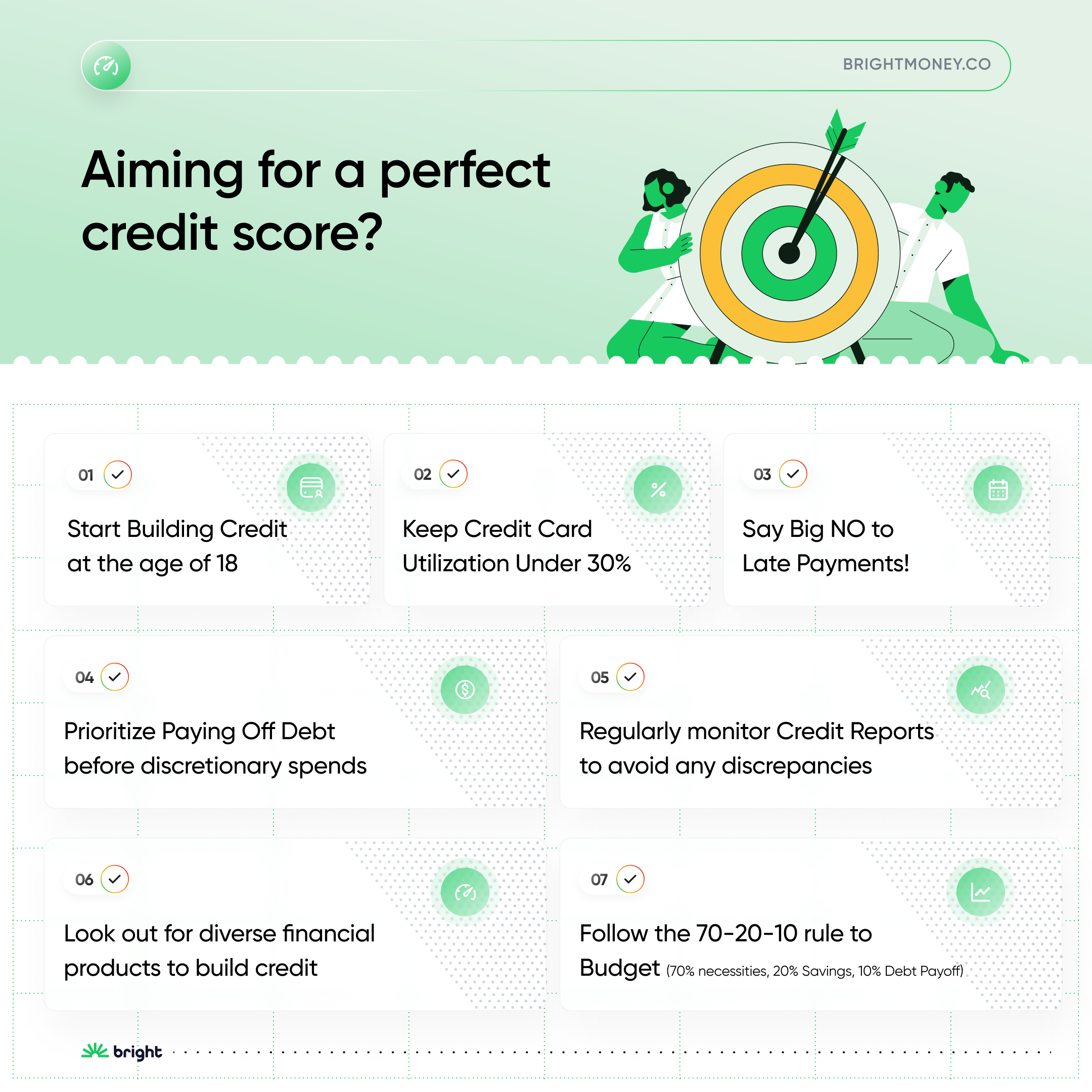

1. Start with Building a Strong Foundation

Credit can be established at an early age. What this means is that you can start working towards building your credit profile and credit history from a young age.

You can start building credit from the young age of 18 with something as simple and fundamental as co-signing on a student loan. But also note the different restrictions which differ from state to state.

You can do so by opening credit accounts but being responsible and managing them well. This could be you taking a small loan or getting a credit card. Prove your reliability by being consistent with your management and making timely payments.

Do this well and you will build a positive credit history early on which will become a testament to your ability to manage credit responsibly, laying a strong foundation for a good credit score in the coming years.

It can also be helpful for youngsters in developing and demonstrating their capability to be financially responsible and as they progress through life, their chances of getting approved for loans much larger will be higher and with less hassle.

This is a crucial age and hence young adults need to avoid accumulating too much debt, beyond what they can handle. It is better if they use credit wisely.

2. Opting for a Credit Card is Fine, but Only if You can Use it Responsibly

The responsibility that comes with owning a credit card cannot be exaggerated as this financial product can play a pivotal role in shaping your credit history and score. They can be a powerful financial tool that provides convenience, security, and means to build positive credit.

Your credit utilization ratio shows lenders your ability to manage your existing debts. It is preferred that you use no more than 30% of your credit.

Making timely payments and ensuring your credit card balances are low is the first step to being responsible. It increases your creditworthiness. You can use your credit card and improve your credit steadily. Use it right and you will gain access to favorable credit opportunities, especially since you have no prior credit history, you are starting with a clean slate.

It’s not easy, but avoid giving in to your impulses and going down the retail therapy rabbit hole. Unnecessary purchases with your credit card can harm more important life requirements. Ensure you have a budget and you are sticking with it while using your credit card.

You will have some perks too. By managing your credit cards well and paying off balances (preferably in full) each month, cardholders may enjoy these perks like big discounts and freebies, which are great!

Be regular in reviewing your credit card statements and stay vigilant. There could be fraudulent charges on your card or even errors may occur. It is your responsibility to report this promptly.

3. Budget, Budget, Budget!

You should be hyper-aware of your monthly expenditure and income. Calculate this accurately and include your side hustles, main salary, and other sources of income. Once you have this number, list all your essential expenses like utilities, groceries, rent or mortgage, transportation, and debt payments.

The moment your income hits your bank account, a portion of it should be moved into emergency funds which you should not touch. This amount should be a standard amount as long as your income remains the same. If there are any variations, you can be flexible to adjust the amount you save, but you should save nevertheless, each month.

The 70-20-10 budget seems to be an adequate choice where you would be required to allocate 70% of your monthly income to spend on necessities, 20% to saving, and 10% to debt payoff.

‘Discretionary spending’ which includes things like your Netflix subscription or eating out is fine. It’s a part of life and we work hard to enjoy the good times, so you can do that but as long as it is within your budget and does not cross reasonable limits.

4. Allocate Funds for Your Debt Properly

Paying off your debt is a sure-shot way into improving your credit score. This will need some planning. Start by listing all the debts you have, including your loans, credit cards or anything else that is an outstanding balance.

Prioritization is key. Do this by arranging them in terms of interest rates and the level of urgency of repayment. Focus on the higher interest rates first, if possible. Another way would be to focus on the smaller debts first to get them out of your way. Look up ‘Debt Avalanche’ or ‘Debt Snowball’ methods.

Like you will do for your savings, you will also start allocating a certain amount of money from your income specifically to repay debt. This is to be done without hindering your plans of meeting your other financial goals and obligations.

With debt repayment on your mind, it will benefit you to cut back on your non-essential expenses so you have more funds to allocate towards debt repayments. With consistency, you will be able to remain motivated and eventually, will become debt-free.

Ready to take charge of your financial future? Visit Bright Money now and unlock the secrets to brighter financial success. Don't wait - start building a stronger credit score and healthier financial habits today!

5. Late payments are a bigger deal than you think

You have gotta start paying your bills on time. Defaults are a terrible look on your credit report. The daily hustle and bustle of life can be distracting. A simple way to ensure you never miss a payment again is to set up payment reminders. Financial apps and services now come with an auto-debt payment feature, use this.

A single late payment could result in your credit score dropping, and the more frequent and recent the late payment/payments, the greater the negative impact it will have on your credit. And sadly, this track record will form and stay on your credit report for nearly seven years and will make it significantly difficult for you to qualify for loans, or credit cards and to get favorable interest rates.

Consistent late payments can have harsh consequences such as having to pay late fees all the time (which amounts to a very large sum over time), your interest rate will rise, your credit report takes a significant hit and your credit score will see decrease. As a result of all this, the financial opportunities you otherwise would have had will slip your fingers.

6. Credit Monitoring is a Great Habit to Have

There are credit monitoring services out there that you could explore. It helps in multiple ways. The three most popular credit bureaus are Experian, Equifax, and TransUnion.

You will be able to detect errors early on by monitoring your credit. These inaccuracies in your report can be addressed promptly as a result. You must dispute them before they make a significant negative impact on your credit score.

Suspicious activities in the finance world happen all the time. You don’t want to be a victim of identity theft. By monitoring your credit, you can catch these activities or unauthorized accounts and take swift action against them to stop fraud attempts or identity theft.

Monitor to observe real-time changes and updates on your credit score. This will make you more aware and it will provide you with insights on your financial health. You can use these to plan your future financial actions and figure out what additional habits you need to build.

7. Build Credit Through Diverse Financial Products

This typically involves using various credit types strategically to establish a robust credit history. By managing credit cards, car loans, student loans, and retail accounts responsibly. Here, you showcase your ability to manage different credit responsibilities by having a mix of credit types. It impacts your credit score positively.

Secured credit cards are a good starting point if you are someone with limited credit history. Installment loans can contribute to your long-term credit-building effort. Retail accounts further diversify your credit profile but manage these prudently for a well-rounded credit history.

A great start is to check out Bright Money. Bright provides a secured loan starting at $50 after you deposit at least $50. This is held in a Savings Account for your benefit. You clear the minimum amount due on this small loan every month. Your payments are then reported to the credit bureaus to help you build positive credit history.

Long-Term Financial Habits for Lasting Credit Score Improvement

1. Set long-term financial goals

Envision and plan for your financial future. You can start by defining specific and clear objectives like having enough money by the time you retire. Or want to buy a home. These goals should be broken down into actionable steps with a clear timeline for completion.

You must consider factors like your current financial situation, the growth of your income, and how you plan to invest. This should be reviewed regularly so you can adjust your goals as per situational change.

Celebrate important milestones while you embark on this journey. Long-term goals always provide direction and it helps to stay motivated. You are working towards creating financial stability and securing your future.

2. Save, it impacts your credit health

You need a safety net in life, this is something savings provide. This makes you less reliant on credit cards or loans in unforeseen circumstances. When you save, you can also make timely payments so you won’t be wasting money on late fees and can save your credit score from being negatively impacted.

Not to mention, savings makes you look good to lenders. It is a sign of stability. So, you will be set for future credit applications without having to turn to high-interest rates. With your savings, you can set down payments on your major purchases like a house or a car easily. Chances of you qualifying for better loan terms are higher.

You have peace of mind and the financial confidence that you can deal with unpredictable situations. You won’t have to worry or stress about emergencies. Your overall financial well-being will be improved which influences your credit health.

3. Embrace change, and be ready for life

It is necessary to regularly review and reassess your financial habits. Our financial situations are subject to change in life. It could take a turn for the better or the worse. So, it is important to be adaptive.

Adjust your financial habits when things change. This involves embracing life changes and accepting that it will impact your finances. Life changes included getting a promotion at work or starting a family - these impact your finances.

This is when you reevaluate your budget, investing, debt management, and saving strategies. You have to be proactive in adjusting your financial habits, otherwise, you will have trouble staying on track with your long-term goals.

Stay flexible and open-minded and it will create a healthy financial outlook for life.

4. Finances test your patience, and Life tests your perseverance

Understand that improving your credit score takes time. It cannot be done at the drop of a hit. It takes hard work and dedication in action and planning. Many times, life will throw curve balls at you and you might have to deviate from your money strategy.

However, keeping the big picture in mind always helps in staying motivated. The path to financial success is an arduous one but it will be worth it when you get to the destination. Seek support from your family and friends, professional financial advisors who can help you stay on track.

Parting Thoughts

It is worth it and it is possible to start building positive financial habits at a young age. By the time you hit 30, you would have made a significant positive impact on your financial future.

By adopting responsible financial habits, understanding credit scores well, and seeking professional support when necessary, you will be able to build a strong foundation for a good financial future.

These habits will help improve your credit score and will also equip you with the tools, awareness, and knowledge you will need to navigate your financial journey with assurance in your skills. ,

It might all seem complex but keep in mind that positive financial habits have the power to shape your financial life and take you toward a more secure and bright future.