You are now leaving the Bright website and entering a third-party website. Bright has no control over the content, products, or services offered, nor the security or privacy of information transmitted to others via their website. We recommend that you review the privacy policy of the site you are entering. Bright does not guarantee or endorse the products, information, or recommendations provided on any third-party website.

Introduction

Are you stressing to make payments on a number of high-interest bills, worried by the constant threat of having negative credit? Then you are not by yourself. A lot of people struggle with money problems that make it hard for them to fulfill their responsibilities, which lowers their credit scores. Debt consolidation loans, on the other hand, offer a lifeline in the shape of a route back towards financial stability.

This guide delves into the best debt consolidation loans for those grappling with bad credit in 2024. Let's explore how these financial tools can offer a beacon of hope for those seeking to untangle their financial woes.

Read more: Who has the best debt consolidation loans?

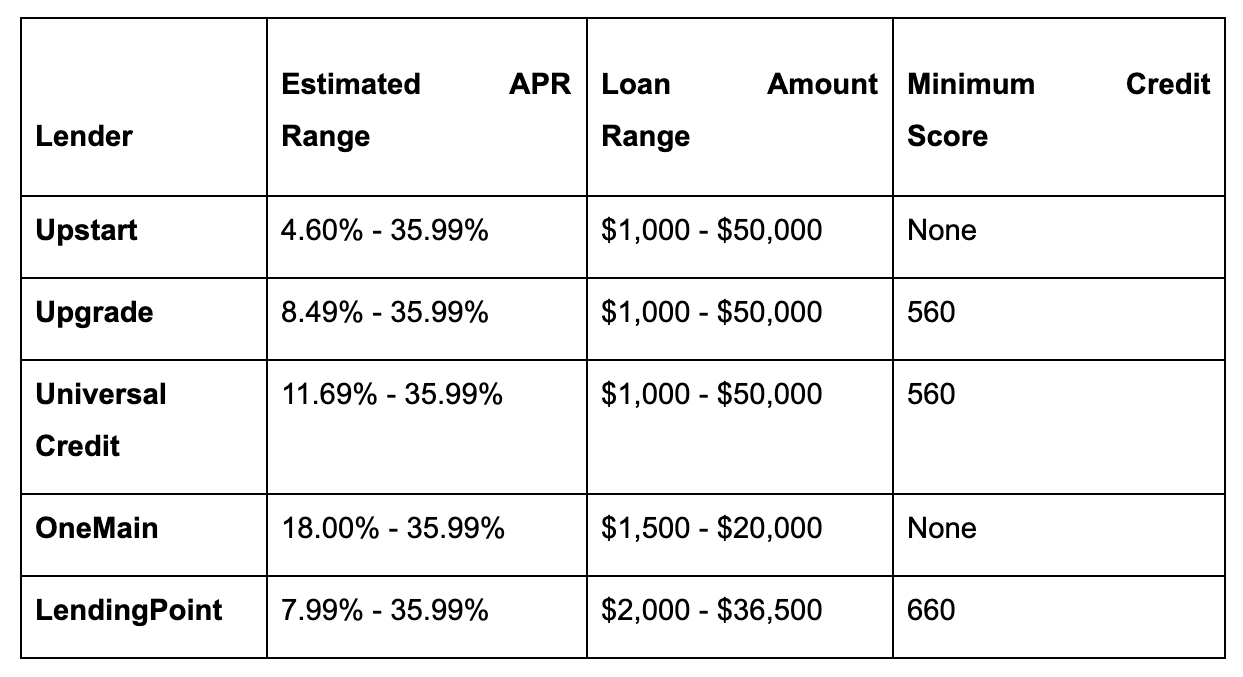

This table provides a quick overview of key information for each lender.[1]

In the ever-shifting landscape of personal finance, finding the right debt consolidation loan can be akin to navigating a maze. But fear not; we're here to shed light on the top contenders in 2024 that can potentially reshape your financial journey.

Sign up with Bright Money and take control of your credit. Let's build healthy financials together!

1. Upstart: A Fresh Perspective on Debt Relief

Among the leading players in the debt consolidation game is Upstart. What sets Upstart apart is its unique approach to evaluating creditworthiness. Unlike traditional lenders fixated on credit scores, Upstart considers various factors, employing artificial intelligence to analyze non-traditional data.

This inclusive approach enables Upstart to extend its reach to individuals with no credit history. The estimated APR ranges from 4.60% to 35.99%, offering a competitive edge in the market. With loan amounts ranging from $1,000 to $50,000 and no minimum credit score requirement, Upstart provides a promising solution for those seeking a fresh financial journey.[1]

Join Bright Money now to access exclusive ways to go debt-free and build healthy credit. Don't miss out on the journey to a brighter, stress-free financial life!

2. Upgrade: Elevating Your Financial Standing

Upgrade, another prominent player in the debt consolidation arena, brings a unique proposition. With an estimated APR ranging from 8.49% to 35.99%, Upgrade positions itself as a reliable option for those with a minimum credit score 560.

The loan amounts, mirroring Upstart's range, extend from $1,000 to $50,000. The distinguishing factor here lies in Upgrade's commitment to aiding individuals with a slightly higher credit score, making it an accessible option for those on the cusp of credit improvement.[1]

3. Universal Credit: Bridging Gaps with Flexibility

If your credit score falls within the 560 range, Universal Credit could be the bridge you need to traverse the turbulent waters of bad credit. Universal Credit stands out for its flexible approach with an estimated APR ranging from 11.69% to 35.99% and loan amounts mirroring those of its competitors.[1]

Recognizing the multifaceted nature of financial struggles, Universal Credit extends a helping hand to those with a less-than-perfect credit history.

Become a Bright Money member and gain access to exclusive perks, expert advice, and cutting-edge financial tools. With Bright Builder, you can build your credit on the go!

4. OneMain: A Stalwart in Debt Consolidation

For those without a minimum credit score to flaunt, OneMain emerges as a robust choice in debt consolidation. With an estimated APR spanning from 18.00% to 35.99%, OneMain acknowledges the challenges those with rocky credit histories face.

The loan amounts, ranging from $1,500 to $20,000, cater to a slightly more modest spectrum, making it an attractive option for individuals seeking a consolidation solution tailored to their needs.[1]

5. LendingPoint: Scaling Heights with Credit Rehabilitation

LendingPoint steps into the arena with a focus on individuals looking to rebuild their credit. While the estimated APR varies from 7.99% to 35.99%, LendingPoint requires a minimum credit score of 660, setting a higher bar for eligibility.[1]

However, LendingPoint opens doors to loan amounts ranging from $2,000 to $36,500 for those who meet this criterion. This targeted approach makes LendingPoint a potential game-changer for individuals on the path to credit recovery.[1]

Say Goodbye to Money Stress - Sign up with Bright Money and take control of your finances. You can easily increase your credit using Bright Builder by Bright Money and enjoy all the exclusive perks.

How do you choose the right debt consolidation loa

Now that we've introduced you to the top players in the field, the question arises: How do you choose the right debt consolidation loan for your specific situation? The answer lies in a thoughtful evaluation of your financial landscape.

- Consider Your Credit Score: Start by understanding your credit score. While some options like Upstart welcome individuals with no credit history, others like LendingPoint set a higher threshold. Knowing your credit score will help you narrow down the options that align with your financial standing, as a score of 740 or higher will qualify you for the best interest rates, followed by a score of 739 or lower [3][1].

- Assess Your Financial Goals: What are you aiming to achieve with a debt consolidation loan? Whether it's lowering your overall interest rates, simplifying payments, or focusing on credit repair, identifying your goals will guide you toward the lender that best suits your needs.

- Compare Interest Rates and Terms: The devil is in the details, and this holds for loan terms and interest rates. Scrutinize the APR, repayment terms, and any additional fees associated with each lender. For example, the APR for LendingPoint starts from 7.99%, and the APR for OneMain starts from 18%. A lower APR might be enticing, but be sure to consider the overall cost of the loan.[1]

- Examine Loan Amounts: Different lenders offer varying loan amounts. For example, Upstart has a loan amount limit of $50,000, but OneMain has a maximum limit of $20,000. Ensure that the loan you choose covers your existing debts while providing room for any additional expenses or emergencies. Striking the right balance is crucial for a successful debt consolidation strategy.[1]

- Explore Reviews and Testimonials: The experiences of others can be invaluable in making an informed decision. Look for reviews and testimonials from individuals who have used the services of the lenders you're considering. This firsthand insight can offer valuable perspectives on customer service, transparency, and overall satisfaction.[2]

Read more: Do consolidation loans hurt your credit?

Conclusion

Navigating the complex world of debt consolidation loans for bad credit can be daunting, but it's not insurmountable. The key is to approach the journey with a clear understanding of your financial goals, credit profile, and the offerings of each lender.

Upstart, Upgrade, Universal Credit, OneMain, and LendingPoint are beacons of hope, each with strengths and tailored solutions. By carefully weighing your options and considering the human stories behind the numbers, you can make an informed decision that paves the way for a brighter financial future.

Sign up with Bright Money now to begin your journey to sound credit! Bright Builder offers you a hassle-free way to improve your credit without burning a hole in your pocket.

References

- https://www.nerdwallet.com/best/loans/personal-loans/best-debt-consolidation-loans-for-bad-credit

- https://www.bankrate.com/loans/personal-loans/how-do-i-choose-the-best-debt-consolidation-lender/

- https://www.equifax.com/personal/education/debt-management/articles/-/learn/what-is-debt-consolidation/

FAQs

1. Can I qualify for a debt consolidation loan with no credit history at all?

Absolutely. Upstart specializes in considering various factors beyond traditional credit scores. Their use of artificial intelligence allows them to evaluate non-traditional data, making it a viable option for individuals with no credit history.

2. How does Universal Credit stand out in terms of flexibility for borrowers facing credit challenges?

Universal Credit distinguishes itself by embracing a flexible approach. Even if your credit score is as low as 560, Universal Credit acknowledges the multifaceted nature of financial struggles, providing an inclusive solution for those with less-than-perfect credit histories.

3. What makes LendingPoint an ideal choice for those aiming to rebuild their credit?

LendingPoint focuses on credit rehabilitation by requiring a minimum credit score of 660. If you're on the path to rebuilding your credit, the competitive APR and targeted approach of LendingPoint can be a game-changer in your financial recovery journey.