You are now leaving the Bright website and entering a third-party website. Bright has no control over the content, products, or services offered, nor the security or privacy of information transmitted to others via their website. We recommend that you review the privacy policy of the site you are entering. Bright does not guarantee or endorse the products, information, or recommendations provided on any third-party website.

Imagine a world where you could access the tools you need to make those long-awaited purchases or pursue your dreams without being bound by the constraints of your bank account. Welcome to the realm of credit—the key to unlocking opportunities and empowering you on your journey to financial success.

Credit is a fundamental concept in the financial landscape, yet its true essence remains shrouded in mystery for many. This article will help you understand the basics of credit and shed some light on the types of credit.

What is a Credit?

A Credit essentially refers to a financial arrangement where a borrower is granted the ability to borrow money or access goods and services with the understanding that they will repay the borrowed amount or cost over time, typically with added interest or fees. It is a trust-based system that allows individuals, businesses, or governments to make purchases or investments that they might not be able to afford outright with their available funds.

When someone receives credit, they are essentially receiving a loan or line of credit from a lender, such as a bank, credit union, or financial institution. This borrowed money can be used for various purposes, like purchasing a home, a car, funding education, or meeting personal needs.

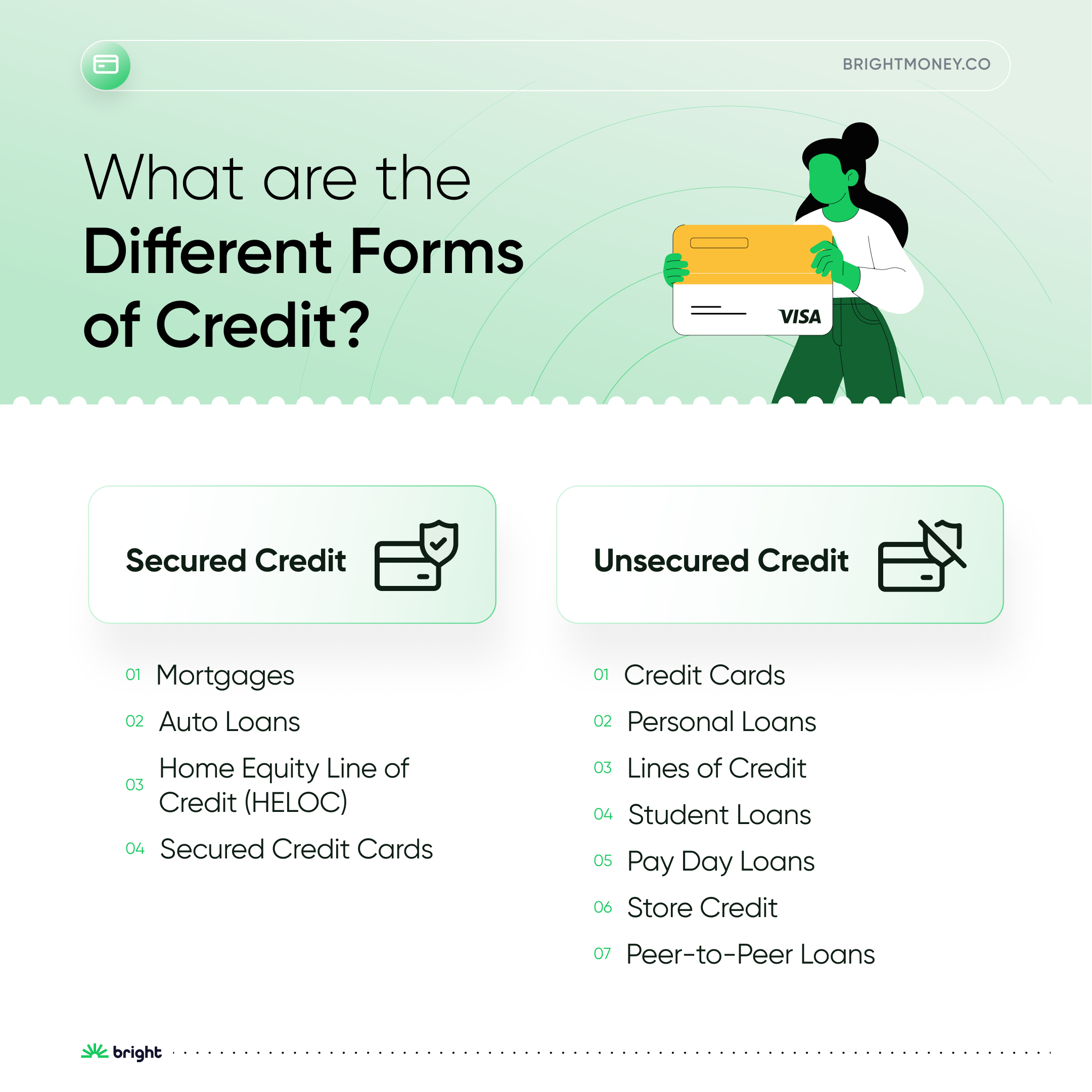

What are the Different Forms of Credit?

There are various forms of credit available to individuals to borrow money or access goods and services. They can generally be classified into secured and unsecured credit.

In secured credit, the loans are backed by collateral, such as the property in the case of mortgages and cars for auto loans, reducing the lender's risk. In unsecured credit, there is no collateral involved, making the loans riskier for lenders, often resulting in higher interest rates and stricter eligibility criteria.

Secured Credit:

1. Mortgages

Long-term loans used to finance the purchase of real estate, where the property itself serves as collateral.

The APR for mortgages can vary widely based on market conditions, loan terms, and individual credit profiles. For an average or good credit score (around 670-739), a typical APR might range from 3.5% to 4.5% for a 30-year fixed-rate mortgage.

To qualify for a mortgage, a minimum credit score of around 620 or higher is generally required. However, for more favorable terms and rates, a credit score of 720 or above might be preferred by lenders.

2. Auto Loans

Loans designed to finance the purchase of vehicles, with the car acting as collateral. For auto loans, the credit limit is determined based on the vehicle's purchase price, the borrower's creditworthiness, and the lender's policies.

Generally, auto loans may cover up to 80% to 100% of the car's value, with higher credit scores allowing for higher loan-to-value ratios. For an average or good credit score (around 670-739), a common credit limit might be $20,000 to $30,000 for a new car.

The APR for auto loans can also vary depending on the borrower's creditworthiness, the loan term, and current interest rates. For an average or good credit score (around 670-739), a common APR might range from 3.0% to 6.0% for a new car loan.

To qualify for an auto loan, a credit score of around 650 or higher is generally considered acceptable. However, a credit score of 700 or above is likely to lead to more favorable loan terms and lower APRs.

3. Home Equity Line of Credit (HELOC)

Borrowing against the equity in a home, providing a flexible revolving credit line often used for home improvements or major expenses.

The credit limit for a HELOC is calculated based on the appraised value of the home, the outstanding mortgage balance, and the borrower's creditworthiness. A general norm for an average or good credit score (around 670-739) might allow a credit limit of up to 80% to 85% of the home's equity. For example, if a home's appraised value is $300,000, and the outstanding mortgage balance is $150,000, the credit limit for a HELOC could be around $90,000 to $97,500.

For an average or good credit score (around 670-739), a typical APR for a HELOC might range from 4.0% to 6.0%. To qualify for a HELOC, a credit score of around 660 or higher is generally required. However, a credit score of 720 or above is likely to increase the chances of approval and secure more favorable terms.

4. Secured Credit Cards

Credit cards that require you to provide a cash deposit to use the card.

Secured credit cards, designed for individuals with lower credit scores or limited credit history, may have credit limits ranging from $200 to $500, depending on the size of the initial security deposit.

Secured credit cards generally have higher APRs, ranging from 20% to 25%, due to the perceived higher risk associated with these cards

Unsecured Credit:

1. Credit Cards

Revolving credit that allows users to make purchases up to a specified credit limit without requiring collateral. Users can choose to pay the balance in full or make minimum payments, incurring interest charges on the remaining amount. The credit limit, APR (Annual Percentage Rate), and credit score requirements depend on the individual's creditworthiness, income, and credit history. Higher credit scores generally lead to higher credit limits and better APRs.

For an average or good credit score (around 670-739), a common credit limit might range from $5,000 to $10,000 for an unsecured credit card. A common APR for unsecured credit cards might range from 15% to 20%.

To qualify for an unsecured credit card, a minimum credit score of around 670 or higher is generally preferred. However, some card issuers may offer cards to individuals with slightly lower credit scores, while others may require higher scores for premium cards with better rewards and benefits.

2. Personal Loans

Unsecured loans offered by banks, credit unions, or online lenders, providing a lump sum repayable in fixed installments over a specified period.

the average credit score required for a personal loan in the US typically ranged from 600 to 700. However, please note that lending criteria can vary among different lenders and financial institutions, and the exact credit score requirement may change over time.

Regarding the amount sanctioned in a personal loan in the US, it also varies based on factors such as the borrower's creditworthiness, income, and the lender's policies. Generally, personal loan amounts can range from a few hundred dollars to tens of thousands of dollars. Some lenders may offer loans up to $35,000 or more, while others might have higher or lower limits.

It's essential to check with specific lenders and their current offerings to get the most accurate and up-to-date information on credit score requirements and loan amounts.

3. Lines of Credit

A predetermined credit limit that borrowers can draw funds from as needed, only paying interest on the borrowed amount.

The average credit score required for a line of credit in the US typically ranged from 600 to 700. However, please note that credit score requirements can vary among different lenders and financial institutions. Some lenders may have more lenient criteria, while others may require a higher credit score to approve a line of credit.

Regarding the amount sanctioned in a line of credit in the US, it also varies based on several factors, including the borrower's creditworthiness and the lender's policies. Lines of credit can range from a few thousand dollars to tens of thousands of dollars or more. The specific credit limit for a line of credit is determined by the lender and is often influenced by the applicant's income, credit history, and other financial factors.

4. Student Loans

Loans designed to finance higher education expenses, often with flexible repayment terms, including deferred payments while the borrower is still in school.

5. Payday Loans

Short-term loans intended to provide quick cash until the borrower's next payday, typically accompanied by high-interest rates and fees.

the loan limits can vary by state and individual lender regulations. However, payday loans are typically small-dollar loans meant to cover short-term financial emergencies. Loan amounts are often in the range of $100 to $1,000, though some states may allow higher loan limits.

6. Store Credit

Credit lines offered by retailers, usable only at their specific stores to encourage customer purchases.

For store credit, the credit score requirements and the sanctioned credit limit vary widely depending on the store's policies and the creditworthiness of the customer. Some customers may receive relatively low credit limits, while others with better credit scores may be granted higher credit limits.

7. Peer-to-Peer (P2P) Loans

Obtained through online platforms that connect borrowers with individual investors, offering diverse borrowing options with varying interest rates and terms.

P2P loans typically range from a few thousand dollars up to tens of thousands of dollars. Some platforms may have a minimum loan amount, while others might have a maximum loan limit

Maintaining a good credit history is crucial as it influences an individual's or entity's creditworthiness. Creditworthiness determines the likelihood of being approved for future credit applications and affects the terms, interest rates, and borrowing limits offered by lenders.

When it comes to managing your finances and achieving your goals, having a guiding light like Bright Money can make all the difference.

Get the Bright Money App to get started on your credit journey!

Learn more about credit scores!