You are now leaving the Bright website and entering a third-party website. Bright has no control over the content, products, or services offered, nor the security or privacy of information transmitted to others via their website. We recommend that you review the privacy policy of the site you are entering. Bright does not guarantee or endorse the products, information, or recommendations provided on any third-party website.

Introduction

Do you ever juggle your finances, trying to make ends meet between paychecks? Or perhaps you're eyeing that new gadget or a dream vacation but don't want to pay for it all at once? Either way, a credit card with a generous interest-free period can be your financial lifesaver. It can give you the breathing space to manage your expenses or make a significant purchase without incurring hefty interest charges. But which credit card provides the maximum interest-free period?

In this article, we'll dive deep into the world of credit cards to discover the best options for those seeking to maximize their interest-free window.

Read more: What is interest, and how does it work?

Which Credit Card Offers the Maximum Interest-Free Period?

The credit card that offers the most extended interest-free period is the HSBC Platinum Credit Card. With up to 55 days interest-free on purchases, it gives cardholders a generous window of time to pay off their balances without incurring any interest charges.

Now, let's learn more about credit cards, uncover the details, and understand the factors determining the interest-free period's length.

Keep your debt in check! Sign up with Bright Money for a smarter way to pay off your debt on high-interest credit cards. It's time to build wealth and improve credit. Join us now!

Factors That Determine the Length of the Interest-Free Period

Now, let's dig into the factors that influence the length of the interest-free period. Credit card companies set their policies and terms so that the specifics may vary from one issuer to another. However, here are some key factors that commonly affect the length of the grace period:

- Billing Cycle: The billing cycle is between two consecutive credit card statements. Typically, it lasts for about 30 days. The interest-free period starts on the day your statement is generated and ends on the statement's due date. Therefore, a longer billing cycle means a more extended interest-free period.

- Statement Date: The day your credit card statement is generated can impact the length of your interest-free period. If your statement date falls on the 1st of the month and your due date is the 25th, you have 24 days of interest-free credit for that billing cycle.

- Due Date: The due date is the deadline for making your minimum payment or paying off your entire balance to avoid interest charges. A due date later in the billing cycle can extend your interest-free period.

- Terms and Conditions: Credit card issuers can set their terms and conditions, including special promotions or introductory offers. These can temporarily extend your interest-free period beyond the standard terms.

- Payment Habits: Your payment habits play a significant role in determining your effective interest-free period. You can maximize the interest-free time window if you consistently pay your balances in full and on time. However, if you carry a balance from month to month, you may lose the benefit of the grace period.[1]

Let's further break down these factors with real-life examples to help you understand how they work in practice.

Don't let financial stress hold you back. Bright Money is here to help you build a brighter financial future. Sign up now and start your path to financial wellness. Your brighter tomorrow begins today!

Real-Life Examples

- Scenario 1: Sarah's credit card statement is generated on the 5th of every month, and her due date is the 25th. This gives her a 20-day interest-free period for each billing cycle. She diligently pays her balance in full each month, ensuring she enjoys the benefits of the full grace period.

- Scenario 2: John's credit card statement is generated on the 15th of every month, and his due date is the 10th of the following month. He has a more extended interest-free period of 26 days. However, John sometimes carries a balance from one month to the next, incurring interest charges.

Now that you understand the factors influencing the interest-free period let's check out credit cards that offer impressive grace periods and the benefits they provide.

"Don't let debt hold you back! Opt for Bright Credit by Bright Money to refinance your high-interest credit card debt. Sign up today and take the first step towards financial freedom."

Credit Cards with Extended Interest-Free Periods

Here are some credit cards known for their generous interest-free periods:

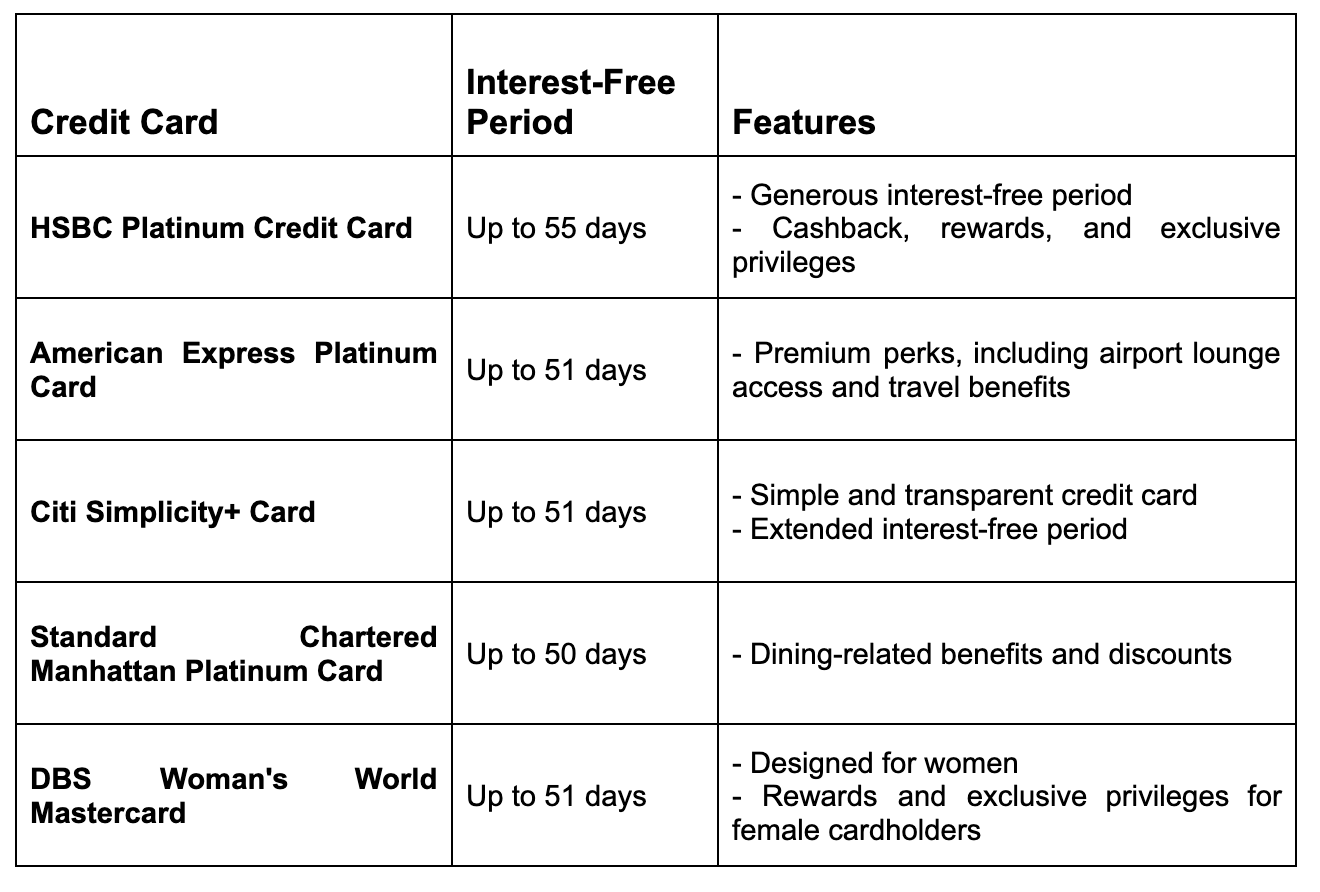

1. HSBC Platinum Credit Card

- Interest-Free Period: Up to 55 days on purchases

- Features: The HSBC Platinum Credit Card is renowned for its lengthy interest-free period. It offers up to 55 days on purchases, giving cardholders ample time to settle their balances without incurring interest charges. Additionally, this card comes with various benefits, such as cashback, rewards, and exclusive privileges.[2]

2. American Express Platinum Card

- Interest-Free Period: Up to 51 days on purchases

- Features: The American Express Platinum Card gives cardholders a generous interest-free period of up to 51 days on purchases. It is known for its premium perks, including access to airport lounges, travel benefits, and rewards programs.[3]

3. Citi Simplicity+ Card

- Interest-Free Period: Up to 51 days on purchases

- Features: The Citi Simplicity+ Card offers a straightforward approach to credit with an extended interest-free period of up to 51 days on purchases. It is designed for those who value simplicity and transparency in their credit card experience.[4]

4. Standard Chartered Manhattan Platinum Card

- Interest-Free Period: Up to 50 days on purchases

- Features: The Standard Chartered Manhattan Platinum Card offers a competitive interest-free period of up to 50 days on purchases. It is tailored for those who enjoy dining out, offering attractive dining-related benefits and discounts.[5]

5. DBS Woman's World Mastercard

- Interest-Free Period: Up to 51 days on purchases

- Features: The DBS Woman's World Mastercard is designed for women and provides an interest-free period of up to 51 days on purchases. It offers rewards and exclusive privileges geared towards female cardholders[6]

Here's a table summarizing the credit cards with extended interest-free periods:

Read more: How to Lower Credit Card Interest & Processing Fees

Conclusion

In credit cards, the interest-free period is a valuable feature that can significantly impact your finances. The HSBC Platinum Credit Card is a top choice, offering up to 55 days of interest-free purchases. However, it's important to remember that your effective credit period depends on various factors, including your billing cycle and payment habits.

"Ready to pay off the debt on your high-interest credit cards? Bright Money is here to help. Sign up now for debt consolidation and credit card refinance."

References

https://www.investopedia.com/insights/forces-behind-interest-rates/

https://www.hsbc.co.in/credit-cards/products/visa-platinum/

https://www.americanexpress.com/in/charge-cards/platinum-card/

https://www.citi.com/credit-cards/citi-simplicity-credit-card

https://www.sc.com/in/credit-cards/manhattan-platinum/

https://www.dbs.com.sg/personal/cards/credit-cards/dbs-woman-mastercard-card

FAQs

1. How does the interest-free period on credit cards work?

The interest-free period on credit cards is when you can make purchases without incurring any interest charges. It typically starts on the day your credit card statement is generated and ends on the statement's due date.

2. What happens if I don't fully pay my credit card balance during the interest-free period?

If you don't pay your credit card balance in full before the due date, you'll incur interest charges on the remaining balance. These interest charges can quickly add up, making your purchases more expensive.

3. Do all credit cards offer the same interest-free period?

No, not all credit cards offer the same interest-free period. The length of the grace period can vary significantly between credit card issuers and even among different card products from the same issuer.

4. How do credit card companies calculate the interest-free period?

Credit card companies typically calculate the interest-free period based on your billing cycle. The period begins on the day your credit card statement is generated and ends on the statement's due date.