You are now leaving the Bright website and entering a third-party website. Bright has no control over the content, products, or services offered, nor the security or privacy of information transmitted to others via their website. We recommend that you review the privacy policy of the site you are entering. Bright does not guarantee or endorse the products, information, or recommendations provided on any third-party website.

Choosing the Best Debt Consolidation Company" is important for those burdened with multiple high-interest debts. Selecting a debt consolidation company that aligns with your financial needs and goals. It addresses the complexities of consolidating various debts into one manageable loan, aiming to reduce your overall interest burden and simplify your monthly payments.

However, the crux lies in selecting the most suitable debt consolidation company, which demands meticulous analysis and a deep understanding of various financial nuances.

Let’s dive into it in detail.

What is the best debt consolidation company?

The best debt consolidation company varies based on individual needs and financial situations. However, Bright Money offers innovative solutions to help individuals manage and reduce debt. While Bright Money does not provide loans, it offers lines of credit and tools like Bright Credit, Bright Builder, and Bright Plan to aid in debt management and credit improvement. Other top debt consolidation companies include SoFi and Upgrade. It's essential to compare services, fees, and terms to find the best fit for your financial goals.

Understanding Your Debt Landscape

Firstly, check out your existing debt. This involves cataloging all debts, noting their nature (credit card debts, personal loans, or other unsecured loans), and understanding the interest rates applied to each.

This initial assessment forms the foundation for identifying a debt consolidation loan that offers lower interest rates and aligns with your financial situation.

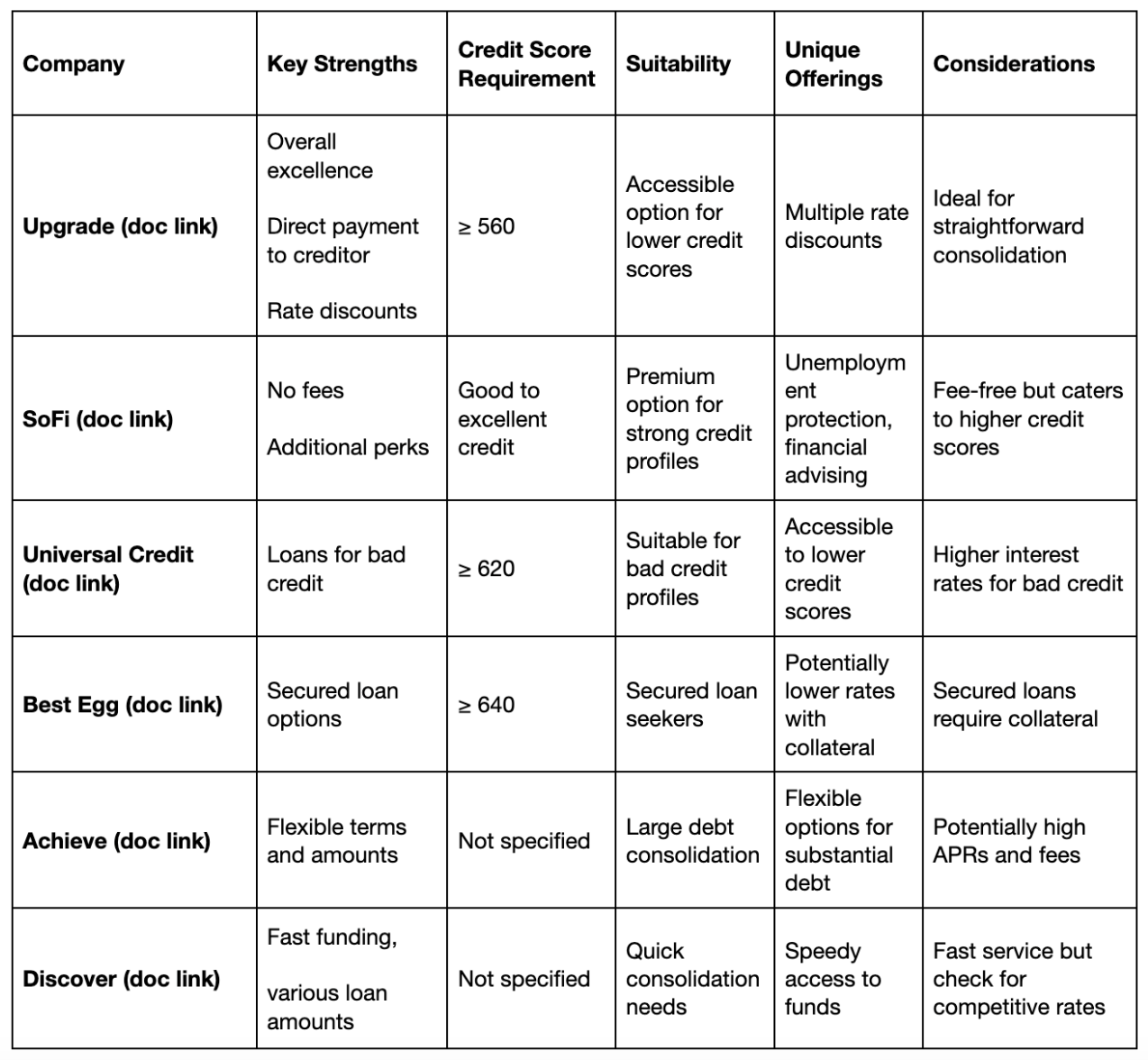

Here is a comparison between the personal loan companies

How to Identify which type of Loan Consolidation Offer you want?

When exploring debt consolidation options, scrutinizing the loan agreements is crucial. Key elements to examine include:

- Interest Rates: Compare various companies' rates to ensure you're getting a competitive deal.

- Repayment Terms: Look for terms that balance manageable monthly payments and the total interest paid over the loan's lifespan.

- Additional Fees: Be aware of origination fees, prepayment penalties, or hidden charges.

- Loan Flexibility: Consider the flexibility of repayment schedules, especially if your financial situation might change.

Credit Considerations

The impact of a debt consolidation loan on your credit score is a critical factor. Initially, your score might dip slightly due to the lender's credit check.

However, effective management of a consolidation loan can enhance your credit profile over time. Consistent, on-time payments reflect financial responsibility, potentially boosting your credit score.

Impact of Debt Consolidation on Your Credit Score

When considering debt consolidation, it's crucial to understand how it can affect your credit score. Let's look into some important aspects of it.

- Initial Impact: Applying for a debt consolidation loan can temporarily lower your credit score due to a hard inquiry from the lender. However, this is typically a minor dip and can be recovered relatively quickly.

- Credit Utilization Ratio: Consolidating your debt, especially with a balance transfer credit card or a personal loan, can improve your credit utilization ratio (the amount of credit you use compared to your available credit). A lower ratio is beneficial for your credit score.

- Payment History: Consistently making on-time payments on your consolidated debt can positively impact your credit score over time, as payment history is a significant factor in credit scoring.

- Diversification of Credit Types: If your debt consolidation involves a different type of credit (like turning revolving credit card debt into an installment loan), it can diversify your credit mix, positively influencing your score.

- Potential Risks: If you consolidate your debt but continue accumulating more debt or fail to make timely payments on the new loan, your credit score can suffer significantly. Closing old credit accounts after transferring balances can decrease your average account age, potentially lowering your score.

Choosing the Right Debt Consolidation Company

Selecting the best debt consolidation company transcends finding the lowest interest rate. It also involves:

- Customer Service Quality: Research the company's customer support system and responsiveness to client needs in detail.

- Market Reputation: Research the company's standing in the financial market and its track record in handling debt consolidation.

- Support Services: Look for companies that offer additional financial management tools or counseling services.

- Direct Payment to Creditors: Companies that pay creditors directly can simplify debt consolidation.

Conclusion

Selecting the right debt consolidation company is critical to effective debt management. This decision should be based on thorough research, focusing on interest rates, loan terms, customer service quality, and the company's overall reputation.

With the right choice and a disciplined approach, debt consolidation can be a key strategy in achieving financial stability and moving towards a debt-free life. Understand the power of responsible credit management with Bright Builder. Apply today and experience a hassle-free way to build your credit score and achieve your financial goals

Suggested readings

- Who has the best debt consolidation loans?

- The beginners’ guide to credit score

- From Debt to Prosperity: 5 Inspiring Stories of Building Credit

FAQs

1. Who's the Best Debt Consolidation Company?

When applying for a debt consolidation loan, the best company often depends on your financial situation, including your existing debt, credit profile, and ability to meet repayment terms. Look for a company that offers lower interest rates than your current high-interest debts, transparent loan agreements, and a good track record. It's a good idea to compare multiple options, as the right company for you should offer a solution that not only consolidates your debt but also saves you money on interest in the long run.

2. Which Debt Management Company is the Best?

The best debt management company is one that helps you effectively manage multiple debts and offers solutions tailored to your unique financial circumstances. These companies should provide clear information about their services, including the pros and cons of debt consolidation loans. Ensure they offer secured loans if you have collateral or unsecured loans if you're looking for a loan with bad credit. The ideal company will work with you to consolidate your debt and create a manageable repayment plan, potentially helping you pay off your debt faster.

3. Can Personal Loans be Included in Debt Consolidation?

Yes, personal loans can be included in debt consolidation. Many people choose to consolidate high-interest personal loans along with other debts. When you consolidate your debt, you combine multiple debts into a single loan, often with more favorable terms, such as lower interest rates or more manageable monthly payments. This can be particularly beneficial if the loan funds are used to pay off high-interest debts, ultimately saving you money and simplifying your finances.

4. Can I Get a Loan to Consolidate My Debts?

You can qualify for a debt consolidation loan to consolidate multiple debts into one, even if you have a less-than-perfect credit history. However, your credit profile will influence the loan terms, including the interest rate and repayment terms.

Some lenders specialize in offering debt consolidation loans to individuals with bad credit. It typically takes a few business days to process your application. Remember, while consolidating can simplify debt repayment and sometimes reduce your interest rate, it's important to consider the overall cost and effect on your credit score.

5. What is Better: Debt Consolidation or Personal Loan?

Deciding between debt consolidation and a personal loan depends on your financial goals. A debt consolidation loan might be a better option if you're looking to pay off multiple high-interest debts.

It consolidates various debts into one loan, potentially with a lower interest rate, saving you money on interest and help you pay off your debt faster. On the other hand, a personal loan is more versatile and can be used for various purposes, not just debt consolidation.

References

https://www.nerdwallet.com/best/loans/personal-loans/consolidation-loans

https://www.forbes.com/advisor/personal-loans/best-debt-consolidation-loans/

https://www.cnbc.com/select/best-debt-consolidation-loans-for-bad-credit/

https://www.foxbusiness.com/money/some-of-the-best-debt-consolidation-companies

Disclaimer: Bright credit is a line of credit that can be used to pay off your credit cards. Subject to credit approval. Variable APR ranges from 9% to 24.99%, and credit limits range from $500 to $8,000. Apr will vary based on prime rates. Final terms may vary depending on credit review. Monthly minimum payments are as low as 3% of the outstanding principal balance plus the accrued interest. Also, you can pay more than the minimum due if you