You are now leaving the Bright website and entering a third-party website. Bright has no control over the content, products, or services offered, nor the security or privacy of information transmitted to others via their website. We recommend that you review the privacy policy of the site you are entering. Bright does not guarantee or endorse the products, information, or recommendations provided on any third-party website.

Managing debt can be a challenging task, especially when you have multiple loans or credit card balances with varying interest rates and due dates. Two common methods for simplifying and potentially reducing debt are debt consolidation loans and balance transfer credit cards. Each of these financial tools has its advantages and disadvantages, and choosing the right one for your specific situation is crucial.

In this guide, we explore the details of debt consolidation loans and balance transfer credit cards to help you make decisions judiciously.

Introduction

Debt can accumulate for various reasons, such as unexpected medical expenses, job loss, or overspending. Regardless of the cause, when faced with mounting debts, it is essential to have a clear strategy for tackling them. Two popular methods for managing and paying off debt are debt consolidation loans and balance transfer credit cards.

These options offer the promise of simplifying your debt repayment plan and potentially reducing your interest costs. However, they differ in several ways, including their eligibility criteria, interest rates, and repayment terms. To make an informed choice, it is vital to understand the nuances of each option and assess which one aligns better with your financial goals and circumstances.

Read more: What is a balance transfer?

Debt Consolidation Loan vs. Balance Transfer Credit Card: Which is Right for You?

Choosing between a debt consolidation loan and a balance transfer credit card depends on your specific financial situation. If you have high-interest credit card debt and want to simplify payments while potentially saving on interest, a balance transfer credit card can be a suitable choice. On the other hand, if you have multiple types of debt or need a more extended repayment period, a debt consolidation loan may be the better option. It's essential to evaluate factors like your credit score, the amount of debt you have, and your repayment capabilities to determine which solution aligns best with your needs.

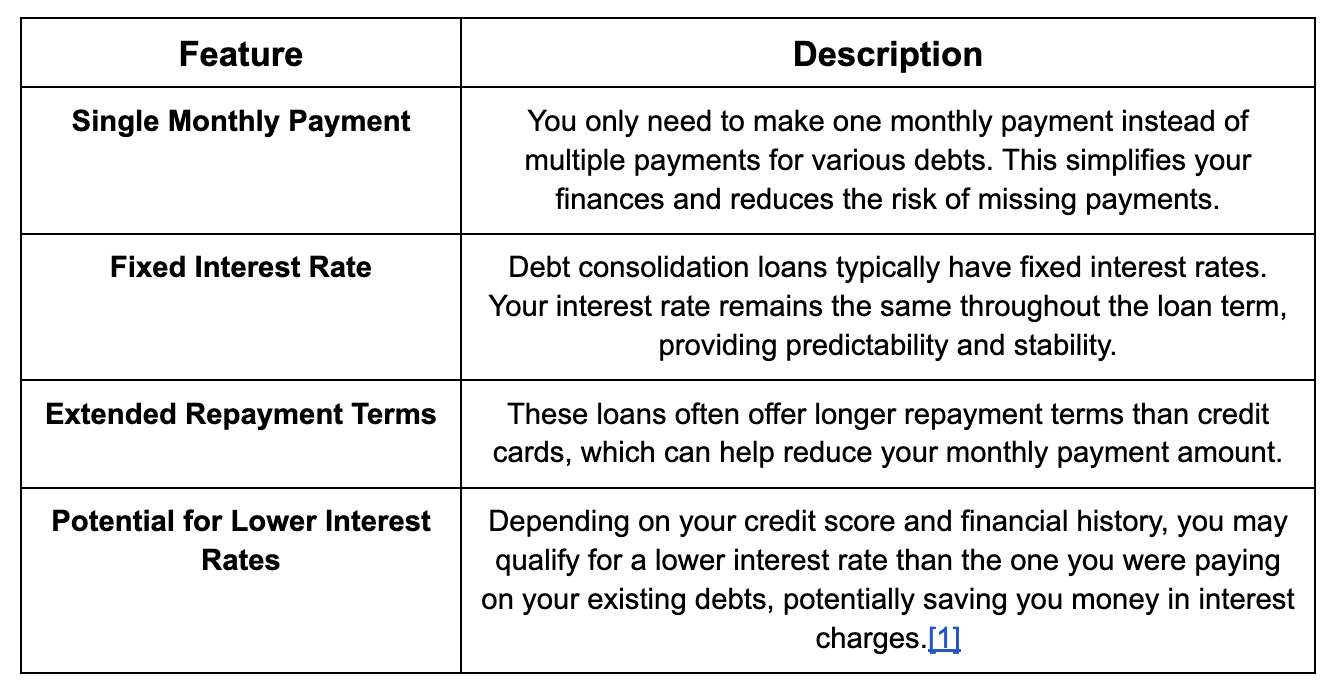

What is a Debt Consolidation Loan?

A debt consolidation loan is a financial product designed to help borrowers streamline their debts by combining multiple loans or credit card balances into a single, manageable loan. The key features of debt consolidation loans include:

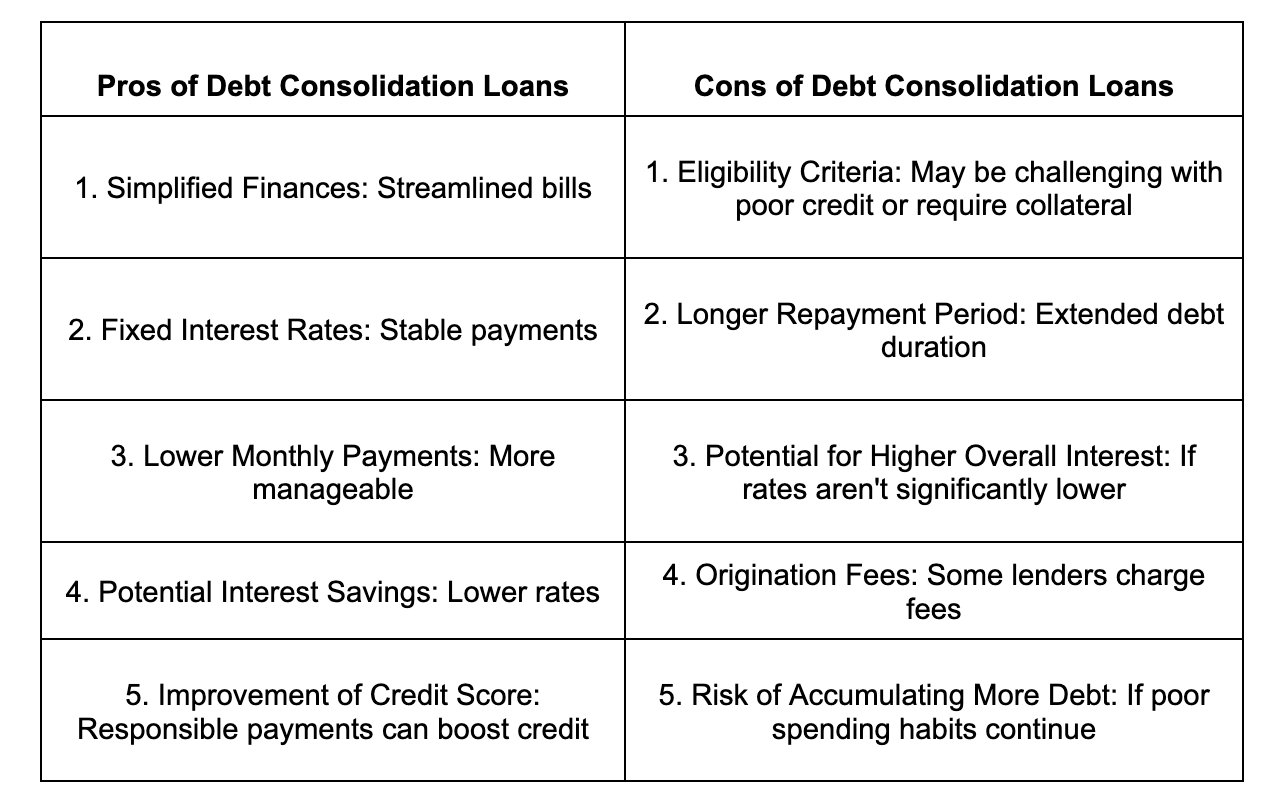

Certainly, here's a table summarizing the pros and cons of debt consolidation loans:

Don't wait any longer to transform your future – unlock the doors to financial freedom today by signing up for Bright Money, your trusted partner on the path to financial well-being.

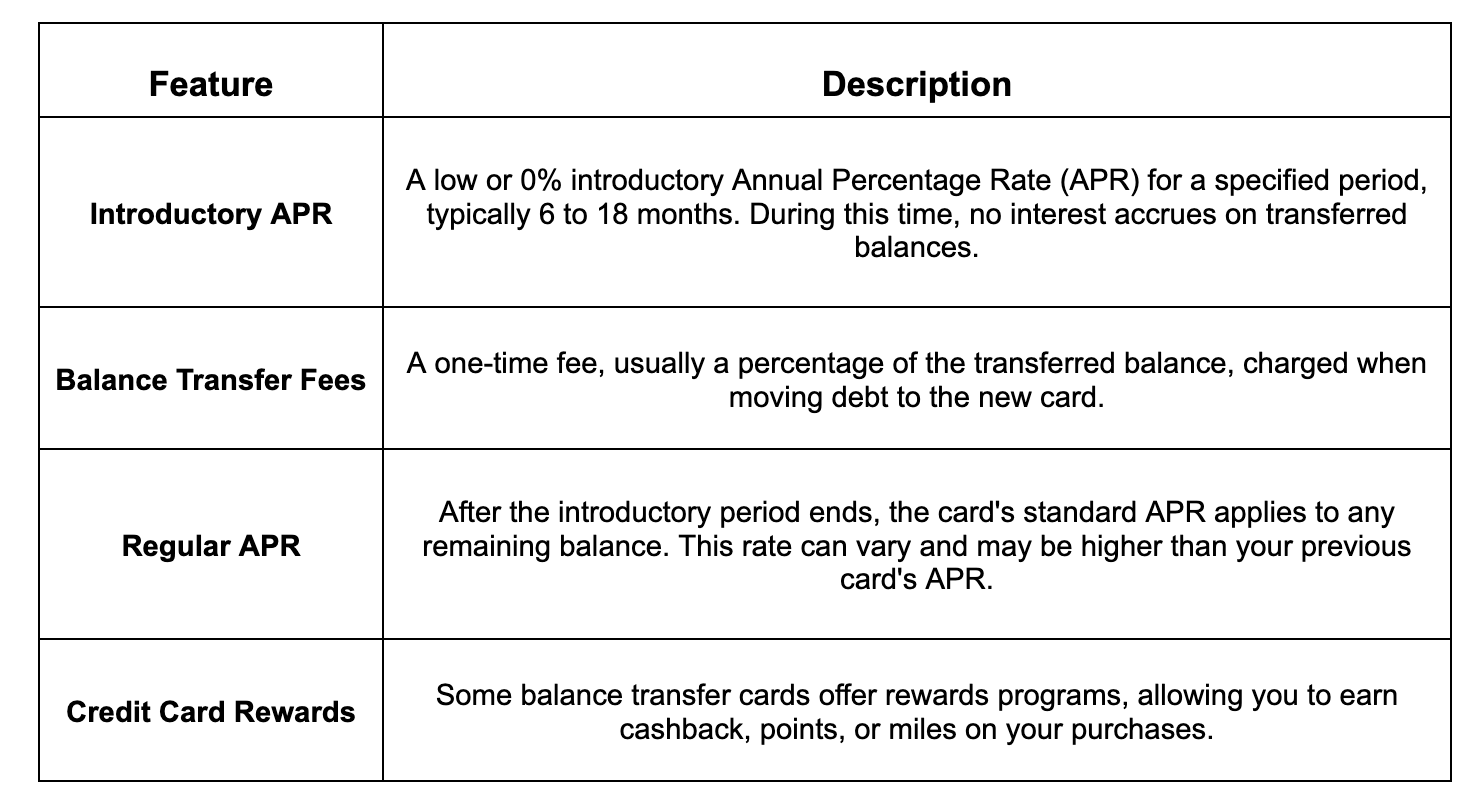

What is a Balance Transfer Credit Card?

A balance transfer credit card is a credit card that allows you to transfer existing credit card balances from one or more cards onto the new card. These cards typically come with promotional periods during which you can enjoy a low or 0% introductory APR (Annual Percentage Rate) on the transferred balances. Key features of balance transfer credit cards include:[2]

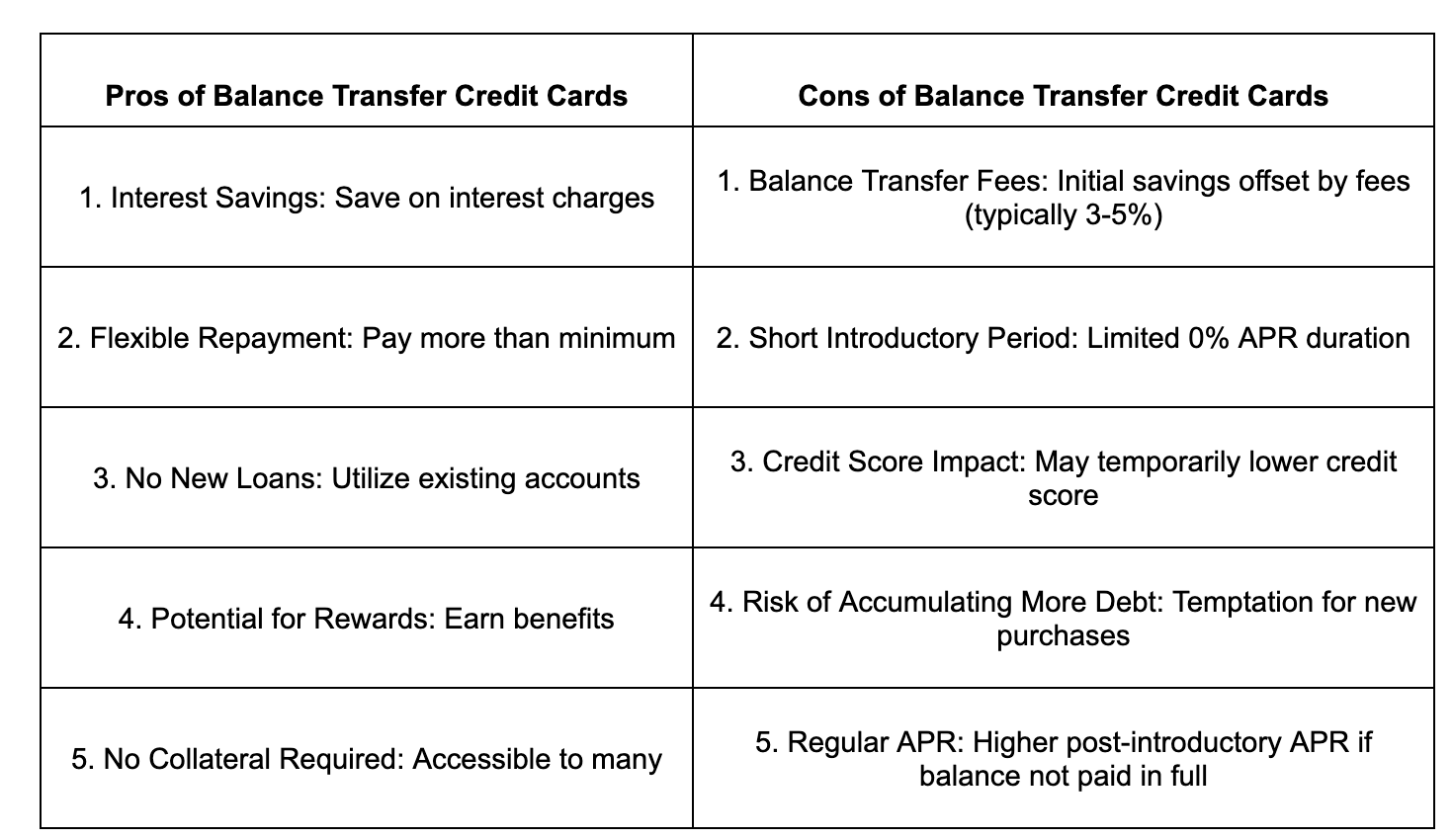

Certainly, here's a table summarizing the pros and cons of balance transfer credit cards:

Join the growing community of thousands of smart savers who have already taken the first step toward financial empowerment. Get started with Bright Money and experience the difference for yourself.

Choosing Between Debt Consolidation Loans and Balance Transfer Credit Cards

Now that we've explored the features, pros, and cons of both debt consolidation loans and balance transfer credit cards, the next step is to determine which option is right for you. Making this decision involves evaluating your financial situation, goals, and preferences.

Consider Debt Consolidation Loans if:

- You Have Multiple Types of Debt: Suppose you're dealing with credit card balances, a personal loan, and medical bills. A debt consolidation loan can bundle all these debts into a single, manageable loan

Example: You owe $5,000 on a credit card, $10,000 as a personal loan, and $3,000 in medical bills. With a debt consolidation loan, you can combine them into one $18,000 loan, simplifying your payments.

- You Prefer Predictable Payments: You value the stability of knowing exactly how much you'll pay each month. A debt consolidation loan with a fixed interest rate provides this predictability

Example: Your monthly payments are $350 for the entire loan term, making budgeting more straightforward.

- You Want a Longer Repayment Term: If lowering your monthly payment is essential, a debt consolidation loan can extend the repayment term

Example: Your original credit card payments totaled $500 per month. After consolidation, your monthly payment drops to $350.

- You Have a Good Credit Score: A higher credit score qualifies you for a lower interest rate on a consolidation loan

Example: With a good credit score, you secure a 6% interest rate, saving money on interest payments compared to your previous credit cards.

- You're Committed to Responsible Spending: If you're determined to avoid accumulating new debts, a consolidation loan can help you stay disciplined

Example: You consolidate your debts and commit to responsible spending habits, not using your credit cards for unnecessary purchases.[3]

Consider Balance Transfer Credit Cards If:

- You Have High-Interest Credit Card Debt: Suppose the majority of your debt is on high-interest credit cards. A balance transfer card with a 0% introductory APR can save you a significant amount in interest

Example: You have $8,000 in credit card debt with a 20% interest rate. By transferring it to a balance transfer card with a 0% APR for 12 months, you can save $1,600 in interest during that period.

- You Can Pay Off the Debt Quickly: If you have a solid plan to pay off the entire balance within the introductory period, a balance transfer card can maximize your savings

Example: You have a clear strategy to pay off your $5,000 balance within the 15-month introductory period, allowing you to do so without incurring interest charges.

- You Don't Want Another Loan: You're averse to taking on more debt in the form of a consolidation loan. A balance transfer card utilizes your existing credit accounts

Example: You prefer not to take on additional loans and opt for a balance transfer card to manage your credit card debt.

- You're Confident in Your Credit Management Skills: To make the most of a balance transfer card, you must manage it responsibly by avoiding new charges and making on-time payments

Example: You're disciplined about not using the balance transfer card for new purchases and focus solely on paying down your existing debt.

- You Want to Earn Rewards: Some balance transfer cards offer rewards, allowing you to benefit from your spending even while paying off debt

Example: Your balance transfer card offers cashback rewards, so as you pay down your debt, you also earn cashback on eligible purchases.[3]

Evaluate Both Options If:

- Complex Situation: Let's say you have a mix of debts, including credit cards, a personal loan, and some medical bills. A complex situation like this might benefit from a debt consolidation loan. It can lump all these debts into a single, manageable loan with a fixed interest rate and structured payments, simplifying your financial life

- Uncertain Eligibility: Imagine you're not sure whether you qualify for either a debt consolidation loan or a balance transfer credit card. You decide to explore both options. You find that you qualify for a balance transfer card with a 0% introductory APR for 18 months, making it an attractive choice to consolidate your credit card debt

- Value Flexibility: Let's say you prioritize flexibility in your debt consolidation approach. You decide to explore both options. After comparing offers, you find a debt consolidation loan with a lower interest rate and a longer repayment term. This allows you to lower your monthly payments, providing financial flexibility

- Professional Advice: You're uncertain about the best route to take, so you consult a financial advisor. They analyze your financial situation and recommend a debt consolidation loan because it offers a lower interest rate than balance transfer cards and is suitable for your specific needs, providing you with professional guidance tailored to your situation.[3]

Your journey to financial wellness begins here and now with Bright Money. Sign up today and gain access to the tools, insights, and support you need to make informed financial decisions and secure your financial future.

Applying for Debt Consolidation Loans and Balance Transfer Credit Cards

Once you've decided which option aligns with your financial needs and goals, the next step is to apply for either a debt consolidation loan or a balance transfer credit card.

For Debt Consolidation Loans, Bright Money is a valuable platform to consider. Bright Money offers personalized insights and recommendations to help you make informed decisions about debt consolidation. They analyze your financial situation and provide guidance on the best debt consolidation options tailored to your needs.

Whether you're looking for lower interest rates, simplified payments, or a strategy to manage your debts more effectively, Bright Money can be a trusted partner in your debt consolidation journey.

When it comes to Balance Transfer Credit Cards, popular options include Chase Slate and Citi Simplicity. These cards often feature competitive introductory 0% APR periods on balance transfers, allowing you to save on interest charges as you work to pay down your debt. Remember to compare the terms, fees, and rewards offered by different credit card issuers to find the one that best suits your balance transfer needs.

Read more: Step-by-step guide for a successful credit card balance transfer

Conclusion

Dealing with debt can be overwhelming, but it is crucial to take proactive steps to manage and eventually eliminate it. Debt consolidation loans and balance transfer credit cards are two popular methods for simplifying your debt and potentially saving on interest costs. The choice between these options depends on your unique financial situation, goals, and preferences.

Before making a decision, carefully assess the advantages and disadvantages of each method. Consider factors such as your credit score, the types of debt you have, your ability to make timely payments, and your commitment to responsible financial behavior. Additionally, be aware of the potential pitfalls associated with each option and take steps to avoid them.

Remember that there is no one-size-fits-all solution when it comes to managing debt. Your choice between a debt consolidation loan and a balance transfer credit card should align with your specific circumstances and help you move toward a debt-free future. Whichever option you choose, stay committed to your debt repayment plan and seek professional guidance if needed. With dedication and the right financial strategy, you can regain control of your finances and work toward a debt-free life.

Empower yourself to take charge of your finances like never before. And the best part? It won't cost you a dime. Sign up for Bright Money for free today and start your journey toward financial mastery.

References:

- https://www.investopedia.com/terms/d/debtconsolidation.asp

- https://www.bajajfinserv.in/insights/what-is-balance-transfer-and-how-does-it-works

- https://www.forbes.com/advisor/personal-loans/debt-consolidation-loan-vs-balance-transfer/

FAQs

- What is the minimum credit score required to qualify for a balance transfer credit card?

The minimum credit score required for a balance transfer credit card varies among issuers but typically falls within the “good” to “excellent” credit range. A FICO score of 700 or higher is often a good benchmark to have a chance at approval.

- How does debt consolidation affect my credit score?

Debt consolidation can have both positive and negative effects on your credit score. On one hand, it can improve your score by reducing your credit utilization ratio and showing a history of responsible repayment. However, opening a new credit account (such as a consolidation loan or balance transfer card) may temporarily lower your score, and any missed payments can have adverse effects.

- Is it possible to consolidate student loans with a debt consolidation loan or balance transfer credit card?

Student loans generally cannot be directly consolidated with balance transfer credit cards. However, you can consider consolidating federal student loans through a Direct Consolidation Loan program or private student loans through a private consolidation loan. Debt consolidation loans can also be used to consolidate various types of debt, including student loans, depending on the lender's policies.

- Can I use a balance transfer credit card to transfer balances between cards from different issuers?

In most cases, you can transfer balances from credit cards issued by different financial institutions onto a balance transfer credit card. However, check the specific terms and conditions of the card, as some issuers may have restrictions or fees for such transfers.

- Are there any tax implications for using a debt consolidation loan or balance transfer credit card to manage debt?

Generally, there are no direct tax implications for using these methods to manage debt. Interest on a debt consolidation loan may not be tax-deductible, unlike some mortgage or student loan interest. However, consult with a tax professional to understand how your specific financial situation may be affected.