You are now leaving the Bright website and entering a third-party website. Bright has no control over the content, products, or services offered, nor the security or privacy of information transmitted to others via their website. We recommend that you review the privacy policy of the site you are entering. Bright does not guarantee or endorse the products, information, or recommendations provided on any third-party website.

Have you ever wondered why some people handle their money so well while others always seem to struggle? It's a common question, and many folks deal with financial stress every day. Even with various incomes, a surprising 61% of Americans live paycheck to paycheck, teetering on the edge of financial trouble.

But here's something hopeful: Among those who don't live paycheck to paycheck, many credit their success to understanding their finances better. They break free from money worries and achieve their goals.

So, what's their secret? Knowing how to deal with interest rates is a big part of smart money decisions. Learning how personal loan interest rates work isn't just about managing debt; it's about taking charge of your financial future.

In this article, we'll dive into the world of personal loan interest rates, demystifying what influences them. We'll give you the knowledge to make smart borrowing choices, whether you're paying off debt, making a big purchase, or just getting financially savvy. This journey will help you make informed decisions and move toward a brighter financial future.

Read more: What is an interest rate and how does it work?

How Are Personal Loan Interest Rates Calculated?

Personal loan interest rates are typically determined by factors such as your credit score, credit history, loan amount, loan term, and the lender's policies. A higher credit score often leads to lower rates, while a longer loan term or riskier credit profile may result in higher rates. Shopping around for lenders can help you find the best rate.

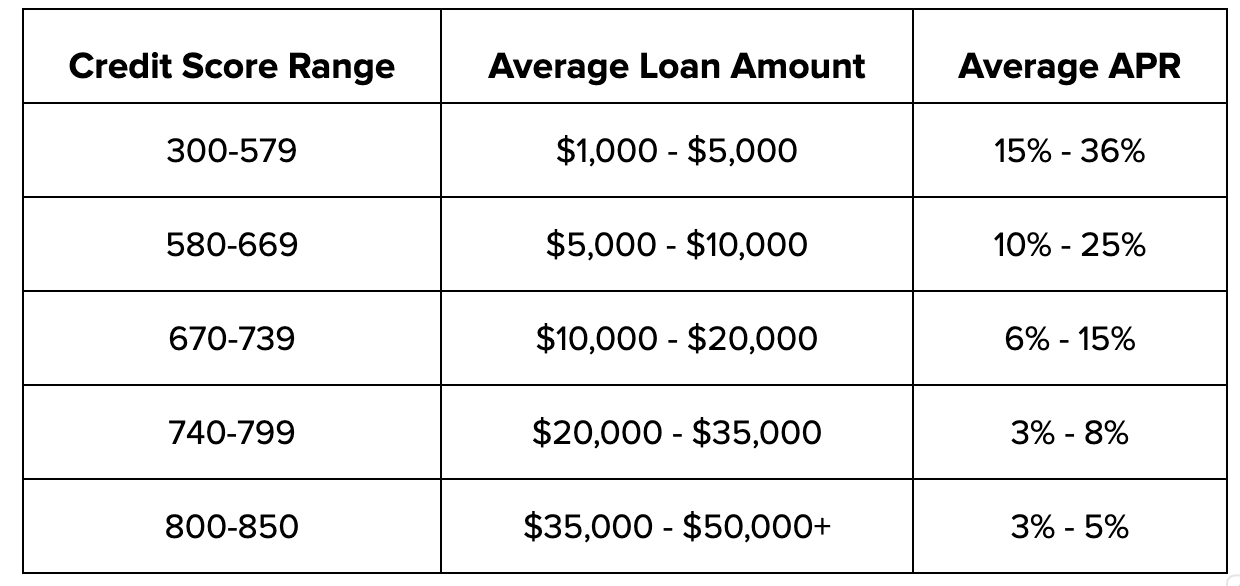

Certainly, here's a table showing how credit score ranges can influence the average loan amount you can get and the average APR (Annual Percentage Rate) you can expect:

Disclaimer: Please note that these are general estimates and can vary depending on various factors, including the lender, your financial history, and the specific loan terms. Credit scores are just one part of the equation when lenders decide on loan amounts and interest rates.

Introduction to Personal Loans

Before diving into the details of interest rate calculation, let's briefly see what personal loans are and why people seek them.

1. What Are Personal Loans?

A personal loan is an unsecured loan offered by banks, credit unions, or online lenders. Unlike secured loans tied to assets like homes or cars, personal loans rely on a borrower's creditworthiness to determine eligibility and interest rates. People use personal loans for diverse purposes, including consolidating high-interest debts, funding home improvements, covering emergencies like medical bills or unexpected repairs, financing major purchases, or supporting educational expenses.

In the realm of personal finance, these loans offer flexibility and financial support without requiring collateral, making them a popular choice for various financial needs. Understanding how interest rates are calculated on personal loans is crucial for making informed borrowing decisions and managing your financial future effectively.[1]

Now that we have a basic understanding of personal loans, let's delve into the heart of the matter: how interest rates on these loans are calculated.

Take Control of Your Finances Today! – Sign up for Bright Money to gain financial clarity and start your journey towards financial success.

Understanding Personal Loan Interest Rates

Interest rates are the cost of borrowing money, and they significantly impact the total amount you will be required to repay over the life of a personal loan. Personal loan interest rates can vary widely from one lender to another and from one borrower to another. To understand how these rates are calculated, we must explore the key factors influencing them.

1. Credit Score

Your credit score is one of the most influential factors in determining your personal loan interest rate. Lenders use your credit score to assess your creditworthiness and your likelihood of repaying the loan on time. Higher credit scores typically result in lower interest rates, while lower scores may lead to higher rates or even loan denials.

Credit scores are generated by credit bureaus, such as Experian, Equifax, and TransUnion, based on your credit history. The most widely used credit scoring model is the FICO score, which ranges from 300 to 850. Here's a general breakdown of how FICO scores can affect your interest rate:

- Excellent Credit (FICO score 720+): Borrowers with excellent credit are likely to qualify for the lowest interest rates available

- Good Credit (FICO score 680-719): Borrowers with good credit can still access competitive interest rates but may not qualify for the absolute lowest rates

- Fair Credit (FICO score 620-679): Interest rates for borrowers with fair credit tend to be higher, and loan approval may be less certain

- Poor Credit (FICO score below 620): Borrowers with poor credit may struggle to secure a personal loan, and if they do, the interest rates are typically significantly higher

2. Loan Amount

The amount you borrow can also influence your personal loan interest rate. In general, larger loan amounts may come with lower interest rates because lenders can earn more interest over the life of the loan. However, the correlation between loan amount and interest rate can vary among lenders.

Start Saving and Investing Wisely – Sign up with Bright Money to receive tailored financial recommendations and maximize your savings and investments.

3. Loan Term

The loan term, or the length of time over which you repay the loan, plays a role in determining your interest rate. Personal loans typically have terms ranging from 12 to 60 months, though some lenders offer shorter or longer terms.

- Shorter Loan Terms: Loans with shorter terms often have lower interest rates because they pose less risk to the lender. However, monthly payments will be higher

- Longer Loan Terms: Loans with longer terms tend to have higher interest rates to compensate for the increased risk to the lender. While monthly payments are lower, you may pay more interest over the life of the loan

4. Annual Percentage Rate (APR)

The Annual Percentage Rate (APR) is a comprehensive measure of the cost of borrowing, as it includes not only the interest rate but also any fees or charges associated with the loan. Lenders are required to disclose the APR, making it easier for borrowers to compare the overall cost of loans from different providers. When comparing personal loans, it is crucial to consider the APR rather than just the interest rate.

5. Lender's Policies

Each lender has its own underwriting guidelines and policies that can affect the interest rate you're offered. Some lenders may specialize in serving borrowers with excellent credit, while others may focus on providing options for individuals with less-than-perfect credit. Looking around and researching the products offered by various lenders can help you find the best loan terms based on your unique financial situation.

6. Economic Conditions

Economic conditions, such as changes in the federal funds rate set by the Federal Reserve, can influence personal loan interest rates. When the Federal Reserve raises interest rates, banks may pass on those increases to borrowers in the form of higher loan rates. Conversely, during periods of economic downturn, interest rates may be lowered to stimulate borrowing and spending.

7. Personal Financial Situation

Lenders may also consider your personal financial situation, including your income, employment status, and Debt-to-income ratio (DTI). A higher income and a lower DTI can make you a more attractive borrower, potentially leading to a lower interest rate.[2]

Unlock a Brighter Financial Future – Join Bright Money now to access personalized financial insights and expert guidance.

How Personal Loan Interest Rates are Calculated?

Now that we've explored the factors that influence personal loan interest rates, let's dive into the mechanics of interest rate calculation. Personal loan interest can be calculated using two common methods: simple interest and compound interest.

1. Simple Interest

Simple interest is calculated on the principal amount borrowed. It remains constant throughout the loan term, as it is based solely on the initial loan balance. The formula for calculating simple interest is as follows:

- Simple Interest = Principal Amount × Interest Rate × Time (in years)

For example, if you borrow $10,000 at an annual interest rate of 7% for three years, the simple interest calculation would look like this:

- Simple Interest = $10,000 × 0.07 × 3 = $2,100

In this case, you would pay $2,100 in interest over the three-year loan term, in addition to repaying the $10,000 principal.

2. Compound Interest

Compound interest is more common in financial products like savings accounts and credit cards, but it is essential to understand how it works. Unlike simple interest, compound interest takes into account the accrued interest on the outstanding balance.

For personal loans, however, simple interest is the standard method used. Nonetheless, some lenders may offer loans with compound interest, so it is crucial to read the loan terms and conditions carefully.

Amortization Schedule

When you take out a personal loan with simple interest, the lender typically provides an amortization schedule. This schedule outlines each monthly payment, including how much goes toward interest and how much goes toward reducing the principal balance.

At the beginning of the loan term, a more significant portion of your monthly payment goes toward interest, with the remainder applied to the principal. As you make payments, the balance shifts, and a greater portion goes toward reducing the principal. Over time, you pay less interest, and your loan balance decreases.[3]

Strategies for Securing a Lower Personal Loan Interest Rate

Now that you understand the factors that influence personal loan interest rates and how they are calculated, let us explore strategies to help you secure a lower interest rate when applying for a personal loan:

1. Improve Your Credit Score

As mentioned earlier, your credit score plays a crucial role in determining your interest rate. To improve your credit score:

- Pay bills on time: Consistently paying your bills on time is one of the most effective ways to boost your credit score

- Reduce credit card balances: High credit card balances relative to your credit limits can negatively impact your score. Aim to keep your credit utilization low

- Avoid opening too many new accounts: Each new credit inquiry can temporarily lower your score, so be cautious when applying for new credit

Experience Stress-Free Money Management – Join Bright Money to simplify your finances and reduce money-related stress.

2. Shop Around

Don't settle for the first loan offer you receive. Instead, shop around and compare loan offers from multiple lenders. Online lenders, traditional banks, credit unions, and peer-to-peer lending platforms all have different loan products and interest rate offerings. By comparing offers, you can find the most favorable terms for your financial situation.

3. Consider a Co-signer

If you have a limited credit history or a lower credit score, you may consider asking a creditworthy friend or family member to co-sign your loan. A co-signer with a strong credit history can help you qualify for a lower interest rate. However, keep in mind that the co-signer is equally responsible for repaying the loan, and any missed payments could harm their credit.

4. Pay Down Existing Debt

Reducing your existing debt can improve your debt-to-income ratio, making you a more attractive borrower. Lenders are more likely to offer lower interest rates to applicants with lower DTIs.

5. Choose a Shorter Loan Term

While longer loan terms may have lower monthly payments, they often come with higher interest rates. If you can afford it, opt for a shorter loan term to secure a lower interest rate and potentially save on interest costs over the life of the loan.

6. Make a Larger Down Payment

If you're using a personal loan to finance a specific purchase, consider making a larger down payment. A larger down payment reduces the loan amount, which can lead to a lower interest rate.

7. Consider Automatic Payments

Some lenders offer interest rate discounts to borrowers who set up automatic loan payments from their checking or savings accounts. These discounts can result in modest interest rate reductions.[4]

Read more: What is better: Personal loans or credit cards?

Conclusion

Personal loans can be valuable financial tools when used wisely, but understanding how interest rates are calculated is essential for making informed borrowing decisions. Interest rates on personal loans are influenced by factors such as your credit score, loan amount, loan term, and the lender's policies.

By taking proactive steps to improve your credit and researching loan offers from multiple lenders, you can increase your chances of securing a lower interest rate and saving money over the life of your loan. Remember that the key to responsible borrowing is to only take out loans that you can comfortably repay and to use them for their intended purpose.

Don't Wait, Secure Your Financial Freedom – Register with Bright Money today and take the first step towards achieving your financial goals.

References:

- https://www.icicibank.com/blogs/personal-loan/what-is-personal-loan-everything-about-personal-loan#:~:text=Personal%20Loan%20is%20an%20unsecured,any%20of%20your%20immediate%20needs.

- https://www.investopedia.com/terms/p/personal-interest.asp

- https://www.adityabirlacapital.com/abc-of-money/personal-loan-interest-rate-calculation#:~:text=Interest%20%3D%20Principal%20x%20Interest%20Rate,60%20months%20or%205%20years.&text=Now%2C%20for%20the%20second%20month,(200000%2D8333.33)%20191666.67.

- https://www.fibe.in/blogs/how-to-negotiate-a-lower-interest-rate-on-loans/

FAQs

- What is the typical range of personal loan interest rates?

Personal loan interest rates can vary widely but typically range from around 5% to 36%. The exact rate you receive depends on factors like your credit score, loan amount, and the lender's policies. Borrowers with excellent credit may secure rates at the lower end of this range, while those with lower credit scores might face higher rates.

- Can I get a personal loan with bad credit?

Yes, it is possible to get a personal loan with bad credit, but it may come with higher interest rates. Some lenders specialize in bad credit loans, but it is essential to be cautious and compare offers, as the terms can be less favorable. Consider improving your credit score before applying to access better rates.

- How does loan term impact interest rates?

The loan term, or the length of time you take to repay the loan, can influence interest rates. Shorter terms often come with lower interest rates, while longer terms may have higher rates. Choosing the right term depends on your budget and financial goals.

- What is the difference between fixed and variable interest rates?

Personal loans may offer either fixed or variable interest rates. Fixed rates remain constant throughout the loan term, providing predictable payments. Variable rates can change over time, often in response to market conditions. Fixed rates are generally more stable, while variable rates can fluctuate.

- Are there prepayment penalties for personal loans?

Some lenders impose prepayment penalties if you repay your personal loan before the agreed-upon term. These penalties are designed to compensate the lender for interest income they would have received. When considering a personal loan, check the terms and ask if there are any prepayment penalties to avoid unexpected fees if you decide to pay off the loan early.