You are now leaving the Bright website and entering a third-party website. Bright has no control over the content, products, or services offered, nor the security or privacy of information transmitted to others via their website. We recommend that you review the privacy policy of the site you are entering. Bright does not guarantee or endorse the products, information, or recommendations provided on any third-party website.

Credit Cards have become an integral part of modern financial life, offering convenience and flexibility in managing expenses. However, they also come with the risk of accumulating Debt, which can have a significant impact on your financial well-being, especially when it comes to your Credit Score. Your Credit Score plays a pivotal role in determining your financial health, influencing your ability to secure loans and mortgages, and even impacting the interest rates you're offered.

In this comprehensive article, we will explore the intricate relationship between Credit Card Debt and Credit Scores, shedding light on how your Credit Card usage can either strengthen or harm your creditworthiness.

What Negatively Affects Your Credit Score

When it comes to your Credit Score, Credit Card Debt is a big deal. Here's the scoop: Your credit utilization ratio, which is just a fancy way of saying how much you owe compared to your credit limit, plays a crucial role. It's recommended to keep it below 30% because going over that can ruin your score. Now, let's talk about how late payments can affect credit scores. Missing even one payment can be a real downer, and it can tank your score by around 100 points or more, depending on where you started

On the bright side, having different types of credit and a long credit history can actually boost your score. But here's a tip: avoid making too many credit applications in a short time because each one can slightly lower your score. So, the bottom line, keeping an eye on these factors can help you manage your Credit Card Debt while also keeping your Credit Score in good shape.

Unlock Financial Freedom Today! - Join Bright Money and take control of your finances for a brighter tomorrow.

Understanding Credit Scores

Understanding Credit Scores is essential for financial well-being. These three-digit numbers, typically ranging from 300 to 850, reflect your creditworthiness and play a pivotal role in your financial life. Lenders use them to assess the risk of lending to you. Several factors influence your Credit Score, including payment history, credit utilization, credit history length, types of credit, and recent credit inquiries.

A higher Credit Score generally signifies responsible financial behavior and can lead to better loan terms and lower interest rates. It's crucial to monitor and manage your Credit Score to achieve your financial goals and maintain a healthy financial future.[1]

To delve deeper into this topic, consider visiting our live blog for more insights on how to manage and improve your Credit Score effectively.

Start Saving Smarter - Sign up with Bright Money to access personalized financial insights and savings recommendations.

Credit Card Debt

Credit Card Debt is like borrowing money from your future self. When you use your Credit Card to buy things or cover expenses, you're essentially taking out a loan. The catch is, that if you don't pay off that loan in full by the due date, you'll start accruing interest, and it can be pretty hefty. The more you owe and the longer you carry a balance, the more it can cost you. It's essential to manage your Credit Card Debt wisely to avoid high interest charges and keep your financial future on the right track.[2]

Read more: 10 Traps to Avoid While Building Credit

What Can Impact Your Credit Score?

Factors that impact your credit score include borrowing history, repayment history, credit utilization, type of credit, and new credit inquiry. The impact of these factors is payment history is 35%, amount owned is 30%, length of credit history is 15%, types of credit is 10%, and new credit is 10%.

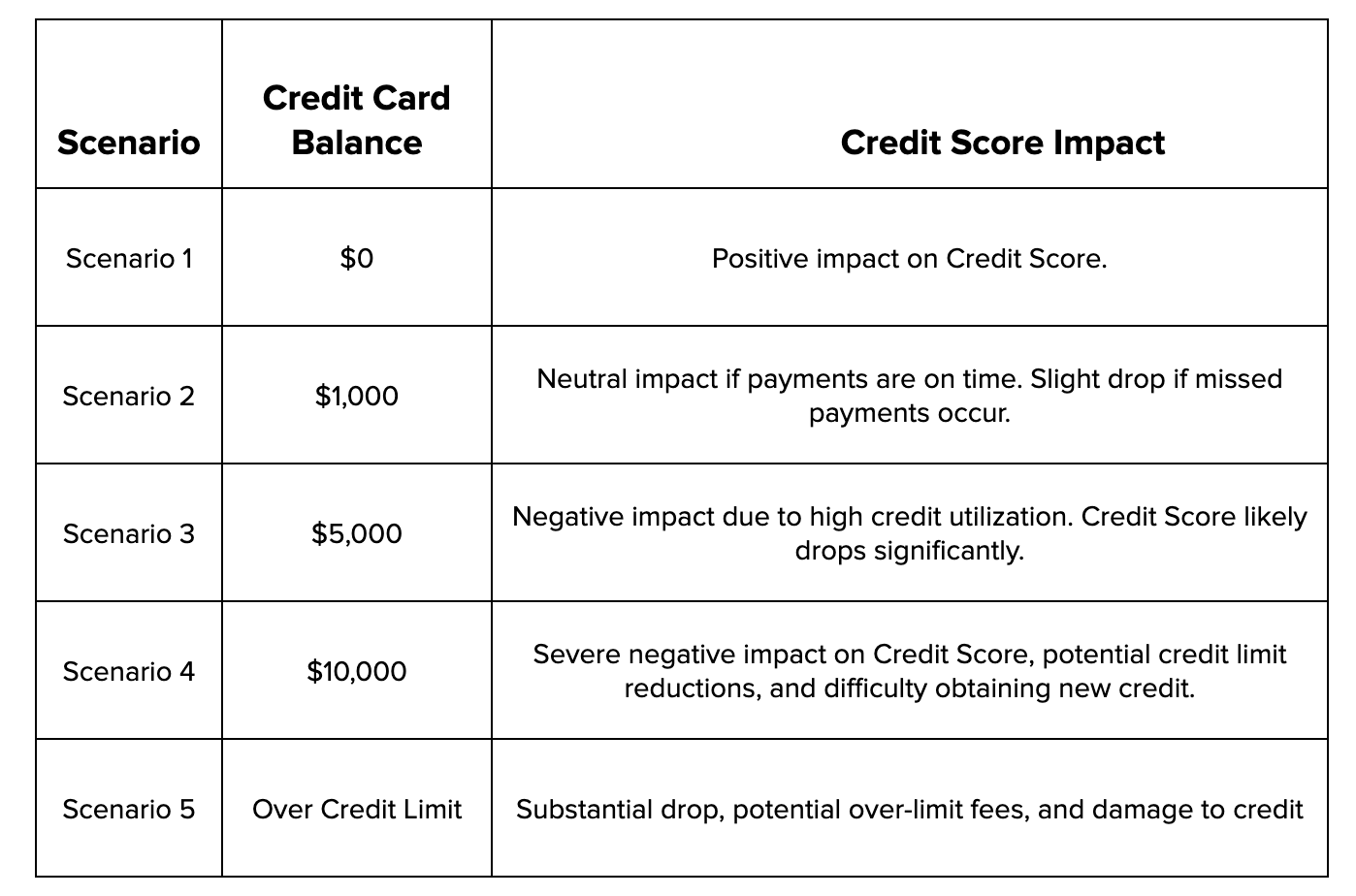

Certainly, let's use an example to illustrate the impact of Credit Card Debt on Credit Scores with different scenarios. Here's a table showcasing how varying Credit Card balances can affect a hypothetical individual's Credit Score:

In these scenarios, maintaining a low Credit Card balance and making on-time payments (Scenario 1) leads to a positive or neutral Credit Score impact. However, carrying a high balance relative to the credit limit (Scenarios 3, 4) or exceeding the credit limit (Scenario 5) can result in significant Credit Score decreases. Consistently missing payments (Scenarios 2, 4) can also negatively affect Credit Scores.

Now, let's delve deeper into the mechanics behind how Credit Card Debt impacts Credit Scores in these different scenarios.

A. Payment History

Your payment history is the most significant factor affecting your Credit Score, making up 35% of the FICO score calculation. Late payments, missed payments, and defaults can severely damage your Credit Score. When it comes to Credit Card Debt, your payment history includes whether you've made timely payments on your Credit Card bills.

Here's how payment history can affect your Credit Score:

- On-Time Payments: Consistently making on-time payments on your Credit Card bills has a positive impact on your Credit Score. It demonstrates responsible financial behavior and reliability

- Late Payments: Late payments can significantly harm your Credit Score. Even a single late payment can lead to a drop in your score, and the more recent and frequent the late payments, the greater the negative impact

- Defaulting: If you default on your Credit Card Debt, it can result in severe consequences, including a significant drop in your Credit Score, collection efforts, and potential legal action by the creditor[3]

B. Credit Utilization Ratio

The credit utilization ratio, which makes up 30% of your FICO score, measures how much of the available credit (made available to you) you're using. A lower credit utilization ratio is generally better for your Credit Score. Here's how Credit Card Debt affects this ratio:

- High Balances: Carrying high Credit Card balances relative to your credit limits can lead to a high credit utilization ratio. This can negatively impact your Credit Score, as it suggests a higher risk of financial strain

- Paying Off Balances: Paying your Credit Card balances can lower your credit utilization ratio, which can have a positive impact on your Credit Score

- Closing Credit Cards: Closing Credit Card accounts can reduce your total available credit, potentially increasing your credit utilization ratio. Hence, it is advisable to keep credit cards open, even if you don't use them regularly[3]

C. Length of Credit History

The length of your credit history accounts for 15% of your FICO score. It considers the age of your credit accounts, including the age of your oldest account, the average age of your accounts, and the age of your newest account. Credit Card accounts play a significant role in your credit history, so it is important to manage them wisely:

- Older Accounts: Older Credit Card accounts with a positive payment history can favorably impact your Credit Score by demonstrating your ability to manage credit over time

- Average Age of Accounts: Opening new Credit Card accounts can temporarily lower the average age of your accounts, potentially affecting your Credit Score. However, this effect diminishes over time

- Closing Accounts: Closing older Credit Card accounts can reduce the length of your credit history, potentially lowering your score. Consider the impact on your credit history before closing accounts[3]

D. Types of Credit

The types of credit you have make up 10% of your FICO score. Lenders like to see a mix of different types of credit accounts, including Credit Cards, installment loans (e.g., car loans), and mortgages. Credit Card accounts fall into the revolving credit category.

- Positive Mix: Having a mix of credit types can positively influence your Credit Score by showing that you can handle different financial responsibilities

- Too Many Credit Cards: While having multiple Credit Cards can be beneficial if managed responsibly, having too many can be seen as a risk factor, potentially affecting your score[3]

Secure Your Financial Future - Don't miss out on Bright Money's expert guidance. Sign up now to secure your financial future.

E. Credit Inquiries

Credit inquiries, which account for 10% of your FICO score, occur when lenders or creditors check your credit report in response to a credit application. There are two types of credit inquiries:

- Hard Inquiries: These inquiries result from credit applications, such as applying for a Credit Card, auto loan, or mortgage. Multiple hard inquiries in a short period can lower your Credit Score

- Soft Inquiries: Soft inquiries occur when you or a company checks your credit report for non-lending purposes, such as background checks or pre-approved credit offers. Soft inquiries do not impact your Credit Score[3]

Read more: What is the Difference Between Credit Score 'Hard Inquiry' vs 'Soft Inquiry'?

Will Paying off Credit Cards Raise Credit Scores?

Yes, paying off credit card debt improves your credit score, which means it reduces credit utilization. For example, closing the account after paying it off decreases the total available credit. Because credit scores take time to update it may reflect in your score.

Does having too many Credit Cards Affect my Credit Score?

Too many cards can impact your credit score, but it depends on how you manage those cards. Opening multiple credit card accounts can increase your credit but decrease your credit utilization ratio. Having multiple credit cards leads to more inquiries and temporarily lowers your score. If you miss any payment on these credit cards, this also negatively impacts your score. Multiple cards may not directly impact credit scores if you manage them properly.

Conclusion

Credit Card Debt can have a profound impact on your Credit Score and overall financial well-being. Understanding how Credit Scores work and the factors that influence them is crucial for making informed financial decisions. By managing Credit Card Debt responsibly, making timely payments, and maintaining a low credit utilization ratio, you will not only be able to protect your Credit Score but also improve it over time.

Remember that recovering from Credit Card Debt and rebuilding your Credit Score may take time and patience. By following the strategies outlined in this article, you can navigate the complexities of Credit Card Debt and emerge with a stronger financial foundation. Ultimately, responsible Credit Card usage and Debt Management are essential skills for achieving long-term financial success.

Experience Stress-Free Finances - Sign up for Bright Money and experience the peace of mind that comes with smart financial management.

References

- https://www.experian.com/blogs/ask-experian/credit-education/score-basics/understanding-credit-scores/

- https://www.experian.com/blogs/ask-experian/credit-education/credit-cards-learn-the-basics-before-you-apply/#:~:text=Credit%20Card%20Basics,-A%20credit%20card&text=Credit%20cards%20are%20considered%20unsecured,the%20debt%20must%20be%20repaid.

- https://www.chase.com/personal/credit-cards/education/credit-score/how-does-credit-card-debt-affect-credit-score#:~:text=The%20amount%20of%20debt%20you,credit%20score%20may%20go%20down.

- https://www.moneyhelper.org.uk/en/everyday-money/types-of-credit/managing-your-credit-card-account

FAQs

1. Can I improve my Credit Score while carrying Credit Card Debt?

Yes, it is possible to improve your Credit Score while carrying Credit Card Debt by focusing on key factors that influence your score. This includes making timely payments, reducing your Credit Card balances (lowering your credit utilization ratio), and avoiding additional debt. Over time, these positive behaviors can help offset the negative impact of existing debt.

2. How quickly can I recover from a Credit Score hit due to debt?

The time it takes to recover from a Credit Score hit due to debt depends on various factors, including the severity of the hit and your financial actions afterward. Generally, late payments can impact your score for up to seven years, while defaulted accounts may remain on your credit report for seven to ten years. However, as you demonstrate responsible credit behavior, your score can gradually improve.

3. Should I close unused Credit Card accounts to improve my score?

Closing unused Credit Card accounts can sometimes have unintended consequences on your Credit Score. It can reduce your total available credit, potentially increasing your credit utilization ratio. Before closing accounts, consider the impact on your credit history and utilization ratio. In some cases, keeping such accounts open yet unused may be a better strategy.

4. Is it better to pay off Credit Card Debt or invest the money?

The decision to pay off Credit Card Debt or invest depends on several factors, including the interest rates on your debt and your investment opportunities. Generally, it is advisable to prioritize paying off high-interest Credit Card Debt, as the interest costs can exceed investment returns. Once your high-interest debt is under control, you can allocate funds to both debt repayment and investing to achieve a balanced financial plan.