You are now leaving the Bright website and entering a third-party website. Bright has no control over the content, products, or services offered, nor the security or privacy of information transmitted to others via their website. We recommend that you review the privacy policy of the site you are entering. Bright does not guarantee or endorse the products, information, or recommendations provided on any third-party website.

Student loan news can significantly impact the lives of individuals seeking higher education. The burden of student loans can be a significant obstacle, but there is a ray of hope for those who qualify for student loan forgiveness programs. Student loan forgiveness is a process that allows borrowers to have part or all of their student loans discharged, alleviating the financial burden of repayment.

Prior to the pandemic, student loan forgiveness programs were available under various schemes, offering relief to eligible borrowers based on specific criteria. These programs included Public Service Loan Forgiveness (PSLF), Income-Driven Repayment (IDR) forgiveness, and more. However, the pandemic brought about a significant change, with the federal government introducing relief measures to help borrowers cope with the financial hardships of the pandemic.

When the COVID-19 pandemic struck, the federal government acted right away to help those who were still paying off their school loans. The government paused federal student loan payments as part of the CARES Act, which was passed in March 2020, and lowered the interest rate to 0% from March 13, 2020, until September 30, 2021.

Due to this rule, borrowers were exempt from making monthly payments during this time and no interest was charged on their loans. This allowed students and graduates to focus on essential needs during a time of economic uncertainty. As the situation evolved, the federal government kept updating policies and regulations regarding student loan forgiveness and relief options.

Several elements are included in the most recent policy on student loan forgiveness. The Biden-Harris Administration's Student Debt Relief Plan involves loan cancellation of up to $20,000, and students can petition for this relief until December 31, 2023. The proposed debt forgiveness plan, which sought to cancel $10,000 to $20,000 in student loans for the majority of students, is now legally in jeopardy.

In this article, we will provide a comprehensive guide on how to apply for student loan forgiveness, covering various forgiveness options and the steps involved in the application process.

Read more: The benefits of living debt-free

What is Student Loan Forgiveness?

Programs for student loan forgiveness are intended to eliminate all or a portion of a borrower's outstanding school debt. Borrowers who meet certain eligibility requirements, such as working in certain public service positions, teaching in impoverished areas, or making payments under particular income-driven repayment plans, are often eligible for these programs.[1]

Types of Student Loan Forgiveness Programs

Student loan forgiveness programs offer hope to borrowers burdened by educational debt—a situation that’s often quite stressful to handle. These programs aim to alleviate some or all of the financial strain associated with loan repayment, but meeting specific eligibility criteria and requirements is mandatory. Below are some common types of student loan forgiveness programs:[2][3]

1. Public Service Loan Forgiveness (PSLF)

The Public Service Loan Forgiveness program is one of the most popular and comprehensive options. It allows borrowers who work in qualifying public service jobs to have their federal student loans forgiven after making 120 qualifying monthly payments under an eligible repayment plan.

To be eligible for PSLF, you must work for a government organization (federal, state, local, or tribal), a non-profit organization classified as tax-exempt under Section 501(c)(3) of the Internal Revenue Code, or other qualifying not-for-profit organizations.[2]

2. Teacher Loan Forgiveness

Teachers serving in low-income schools may be eligible for Teacher Loan Forgiveness. Under this program, eligible teachers can have up to $17,500 in federal direct or Stafford loans forgiven after completing five consecutive years of full-time teaching at a qualifying school.[2]

3. Income-Driven Repayment Plan Forgiveness

Income-Driven Repayment (IDR) plans offer loan forgiveness after certain qualifying payments (typically 20 or 25 years) based on the borrower's income and family size. The remaining balance is forgiven at the end of the repayment term. It is essential to note that the forgiven amount may be subject to income tax, unlike other federal forgiveness programs. The percentage of forgiveness varies based on the chosen IDR plan and the number of years of payments made.[2]

4. Perkins Loan Cancellation

Federal Perkins Loan recipients may qualify for Perkins Loan Cancellation if they work in specific fields, such as teaching, nursing, law enforcement, or serving in the military. The cancellation amount varies based on the profession and the number of years of service, with a certain percentage of the loan (up to 100%) being forgiven for each year of qualifying service.[3]

5. Closed School Discharge

If your school closes while you are enrolled or shortly after you withdraw, you may be eligible for a Closed School Discharge. This program allows you to have your federal student loans discharged, and you may be eligible for reimbursement of past payments. The Closed School Discharge provides 100% loan forgiveness.[3]

Don't Let Student Debt Hold You Back - Discover Your Path to Financial Freedom with Bright Money. Sign Up Now!

How to Apply for Student Loan Forgiveness?

Student loan forgiveness application involves careful attention to detail and adherence to specific guidelines. To apply for Student Loan Forgiveness (SLF), you can visit the official website of the Department of Education or the Federal Student Aid website. Here are the links where you can find more information on how to apply: [1][2][3]

- Department of Education: https://www.ed.gov/

- Federal Student Aid: https://studentaid.gov/

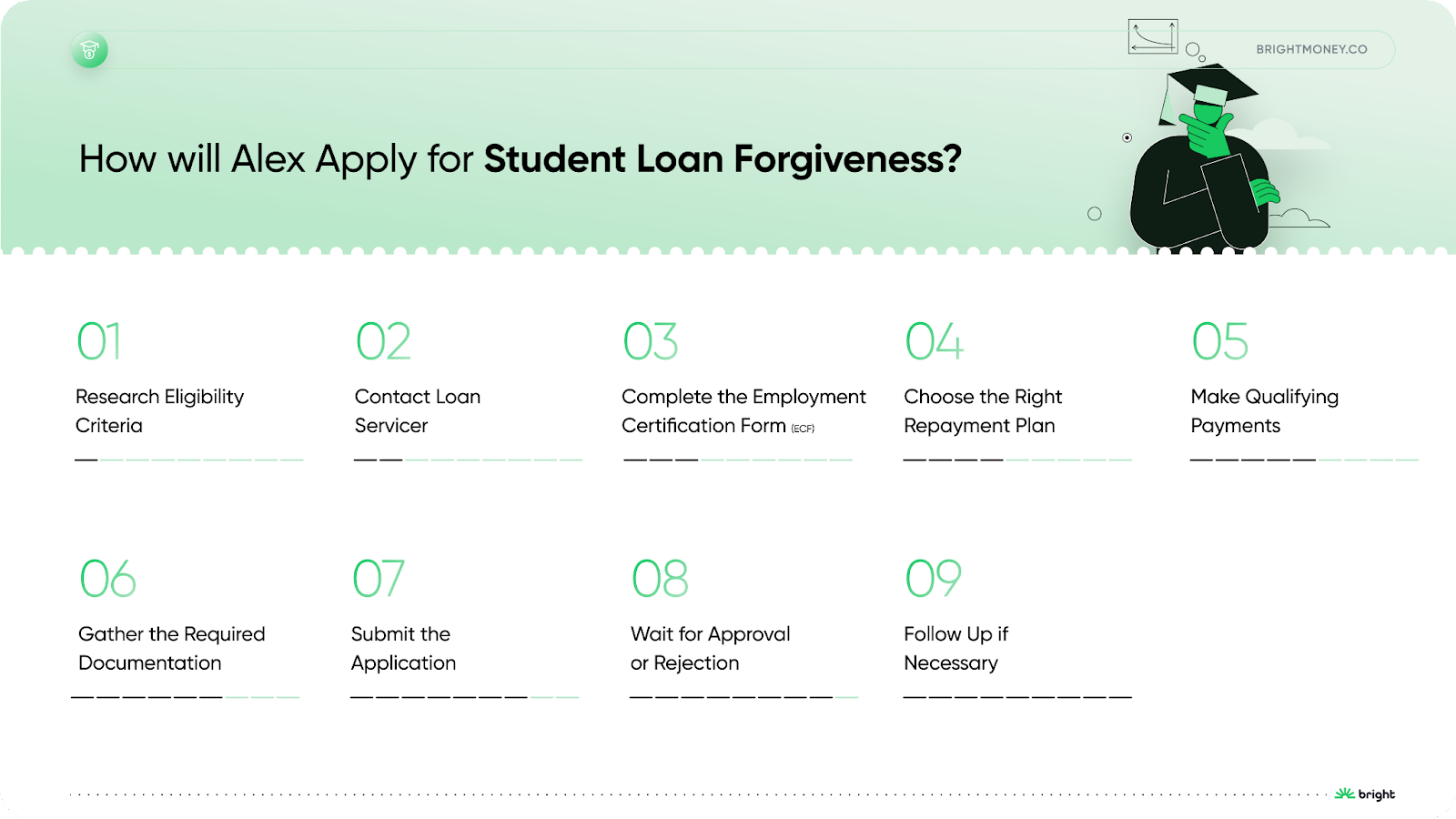

To make the process smoother and more successful, let's take the example of a student named Alex who wants to apply for student loan forgiveness. Here are the steps Alex should follow:

Step 1: Research Eligibility Criteria

Alex should start by researching the eligibility criteria for the student loan forgiveness programs. He should check the requirements for each program to see if he meets the necessary criteria based on his employment, loan type, repayment plan, and loan payment history.

Step 2: Contact Loan Servicer

Alex should contact his loan servicer, the company that manages his student loan account. He can discuss his interest in applying for student loan forgiveness and ask them for essential information about available programs, the application process, and any required documents.

Step 3: Complete the Employment Certification Form (ECF)

If Alex is pursuing Public Service Loan Forgiveness, he must complete the Employment Certification Form (ECF). This form helps track his qualifying payments and verifies his eligibility for the program. Alex should submit this form annually or whenever he changes employers to ensure an accurate recording of his progress toward forgiveness.

Step 4: Choose the Right Repayment Plan

Alex needs to choose the appropriate repayment plan that aligns with his financial situation and future career goals. Most forgiveness programs require enrollment in an income-driven repayment plan, which bases monthly payments on income and family size, making it more manageable.

Step 5: Make Qualifying Payments

To qualify for forgiveness, Alex must make the required number of qualifying payments. For Public Service Loan Forgiveness (PSLF), this means making 120 qualifying payments, while income-driven plans may require 20 or 25 years of on-time payments. Alex should ensure he stays on track and avoids payment delays or forbearance that might reset his progress.

Step 6: Gather the Required Documentation

Depending on the forgiveness program Alex is applying for, he may need to gather various documents, such as tax returns, pay stubs, and proof of employment. It's essential that he has all the necessary paperwork ready to expedite the application process.

Step 7: Submit the Application

Once Alex has met all the requirements and gathered the required documents, he should submit his application for student loan forgiveness. He should carefully follow the instructions provided by his loan service provider and double-check whether all the information shared is accurate and complete.

Step 8: Wait for Approval or Rejection

After submitting the application, Alex should be patient and wait for the response from his loan servicer. The processing time may vary based on the volume of applications and the complexity of his case.

Step 9: Follow Up if Necessary

If Alex's application is approved, he can now enjoy student loan forgiveness. However, if his application is rejected, he shouldn't lose hope. Alex should review the reasons for rejection and, if he believes it was an error, consider appealing the decision or taking corrective action.

By following these steps diligently, Alex can increase his chances of successfully applying for student loan forgiveness and easing the burden of his student loans.

How to Improve Your Chances of Student Loan Forgiveness

Securing student loan forgiveness can be a life-changing opportunity, but it requires careful adherence to program requirements. To enhance your chances of qualifying, follow these essential steps:[2]

1.Thoroughly Understand Eligibility Criteria

Before pursuing any forgiveness program, thoroughly review and understand the eligibility criteria. Each program has specific requirements regarding employment type, loan types, repayment plans, and qualifying payments. By familiarizing yourself with these criteria from the beginning, you can tailor your career choices and loan management to meet the program's standards.

2. Submit the PSLF Form Annually

For Public Service Loan Forgiveness (PSLF) applicants, submitting the PSLF form annually is crucial. This process ensures that your employment remains eligible for forgiveness and allows you to maintain a record of your qualifying service over the years.

3. Maintain Comprehensive Documentation

Keep meticulous records of all essential documents related to your loans and employment. This includes student loan statements, W-2 forms, pay stubs, and any other supporting documentation that may be required for your forgiveness application. Organizing these records will streamline the application process and prevent any delays or complications.

4. Stay Informed and Communicate

Regularly communicate with your loan servicer to track your progress towards loan forgiveness. Staying informed about your current status and the number of qualifying payments made will help you stay on track and address any potential issues proactively.

5. Seek Professional Guidance

If you find navigating the forgiveness process overwhelming, seek assistance from student loan experts or financial advisors. They can provide valuable insights, answer your questions, and guide you through the intricacies of the application process.

Read more: Financial Literacy Gaps

Conclusion

Applying for student loan forgiveness can be a daunting process, but it can be a lifeline for individuals facing overwhelming student loan debt. Understanding the eligibility criteria and following the necessary steps will greatly increase your chances of successfully navigating the application process.

Whether you qualify for Public Service Loan Forgiveness, Teacher Loan Forgiveness, Income-Driven Repayment Plan Forgiveness, Perkins Loan Cancellation, or other programs, it is essential to stay informed and proactive throughout the process with student loan forgiveness updates.

Remember, each student loan forgiveness 2022 program has specific requirements and timelines, so planning properly and making informed decisions about your student loans is crucial for a brighter financial future. The relief of student loan forgiveness can be life-changing, allowing you to focus on your career and personal goals without the weight of debt holding you back.

Take charge of your student loan journey. Let Bright Money guide you toward a debt-free future with loan forgiveness programs. Download App Now!

References:

- https://www.investopedia.com/terms/s/student-loan-forgiveness.asp#toc-how-do-i-get-loans-forgiven

- https://www.forbes.com/advisor/student-loans/apply-for-student-loan-forgiveness/

- https://studentaid.gov/manage-loans/forgiveness-cancellation

FAQs

Q. Are private student loans eligible for forgiveness?

No, private student loans are not eligible for federal forgiveness programs. However, some private lenders may offer their own forgiveness or discharge options under specific circumstances.

Q. Can I apply for multiple student loan forgiveness programs simultaneously?

Yes, you can potentially qualify for multiple forgiveness programs if you meet the eligibility criteria for each. However, the same loan payments cannot be used to qualify for forgiveness under more than one program.

Q. Will my forgiven student loan amount be taxable?

For most federal forgiveness programs, the forgiven amount is not considered taxable. However, with income-driven repayment plan forgiveness, the forgiven amount may be treated as taxable income.

Q. Can I still pursue loan forgiveness if I'm in default on my student loans?

In most cases, you must bring your loans out of default and into good standing before applying for forgiveness. Utilize loan rehabilitation or consolidation to become eligible for forgiveness programs.

Q. Do I need to work full-time to qualify for Public Service Loan Forgiveness?

Yes, to be eligible for Public Service Loan Forgiveness, you must work full-time (30 hours or more per week) for a qualifying employer. Part-time employment does not count toward the required 120 qualifying payments.

*Bright Credit is a line of credit that can be used to pay off your credit cards. Subject to credit approval. Variable APR range from 9% –29.99%, Credit Limit ranges from $500 - $8,000. APR will vary based on prime rates. Final terms may vary depending on credit review. Monthly Minimum Payments are as low as 3% of the outstanding principal balance plus the accrued interest. Also, you can choose to pay more than the minimum due if you want to pay down the loan faster. Credit line originated by Bright or CBW Bank, Member FDIC. Products and services are subject to state residency and regulatory requirements. Bright Credit is currently not available in all states.