You are now leaving the Bright website and entering a third-party website. Bright has no control over the content, products, or services offered, nor the security or privacy of information transmitted to others via their website. We recommend that you review the privacy policy of the site you are entering. Bright does not guarantee or endorse the products, information, or recommendations provided on any third-party website.

Want to find out what a perfect credit score is? Read more here!

Maintaining a good credit score necessitates regular monitoring of your credit report, as it provides invaluable insights into your credit health. By consistently reviewing your credit report, you can swiftly detect any errors or signs of fraudulent activity that may be adversely impacting your score. This proactive approach ensures that your credit information remains accurate and enables you to take prompt action to safeguard and bolster your creditworthiness.

Easy Step-by-Step Guide to Help You Access Your Credit Score:

1. Obtain Your Credit Reports

Start by requesting free credit reports from each of the three major credit bureaus: Equifax, Experian, and TransUnion. You are entitled to one free credit report from each bureau every 12 months under federal law. The Fair Credit Reporting Act (FCRA), a federal law, requires this. Visit AnnualCreditReport.com to access your reports online, or you can request them via phone or mail.

2. Review Your Credit Reports

Thoroughly review the information on each credit report for accuracy. Check for any errors, inaccuracies, or fraudulent accounts. If you find any discrepancies, dispute them with the respective credit bureau(s) to have the information corrected.

3. Choose a Credit Monitoring Service

Consider enrolling in a credit monitoring service that offers regular updates on your credit score and alerts you to any significant changes or suspicious activities. Many credit monitoring services are available online and provide valuable insights into your credit health.

4. Sign Up for Credit Score Services

Several financial institutions and credit card issuers offer free credit score monitoring services to their customers. Check with your bank or credit card provider to see if they provide access to your credit score as part of their services.

5. Use Credit Score Apps

There are various mobile apps specifically designed to help you track your credit score easily. Download a reputable credit score app from your device's app store and follow the instructions to sign up and access your credit score.

6. Explore FICO or Vantage Score

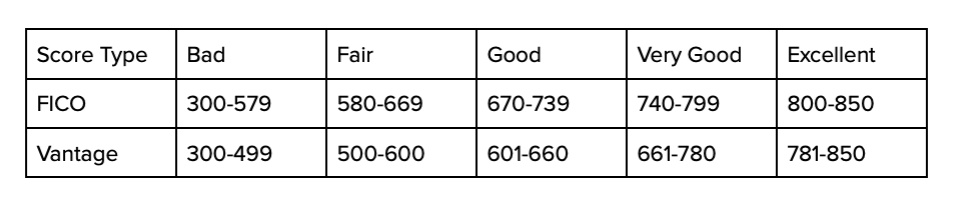

FICO and VantageScore, the two most common credit scoring models, offer consumers the option to purchase their credit scores directly from their websites. Visit myFICO.com for FICO scores and VantageScore.com for VantageScores.

FICO is the dominant credit scoring model used by lenders, while VantageScore is a newer credit scoring model developed collaboratively by Equifax, Experian, and TransUnion, the three major credit bureaus. Despite similarities in their scoring structures, FICO prioritizes late payment history, while VantageScore incorporates trended credit data and has a shorter credit history requirement.

7. Verify Identity

To access your credit score from any source, you'll likely need to verify your identity. Be ready to provide information like your Social Security number, date of birth, and other personal details for verification.

8. Review Your Credit Score

Once you have access to your credit score, review it carefully. Understand the range of scores and what it means for your creditworthiness. A higher score indicates better credit health and increased chances of securing loans and favorable interest rates.

9. Monitor Regularly

Make it a habit to check your credit score regularly, especially if you're actively working on improving your credit. Regular monitoring allows you to track your progress, detect any changes, and respond promptly to potential issues.

10. Take Action

If your credit score is lower than expected or there are areas for improvement, take proactive steps to enhance your credit health. Focus on making on-time payments, reducing credit card balances, and addressing any negative factors affecting your score.

Will My Credit Score Get Impacted While Checking?

When you check your own credit score, it is considered a soft pull or soft inquiry, and it does not impact your credit score. Soft inquiries are only visible to you and do not affect your creditworthiness in any way.

On the other hand, if a lender or creditor checks your credit score as part of a credit application process, it is considered a hard pull or hard inquiry. Hard inquiries can have a small negative impact on your credit score, typically lowering it by a few points. However, the impact is usually temporary and will gradually diminish over time.

It's important to monitor your credit regularly and check your credit report for any errors or discrepancies. By checking your own credit score, you can stay informed about your credit health without worrying about any negative impact on your credit score.

What is the difference between Hard Inquiry and Soft Inquiry?

A hard pull, also known as a hard inquiry, occurs when a lender or creditor checks your credit report as part of the application process for a new loan or credit card. Hard pulls can slightly lower your credit score and are visible to other lenders, as they indicate you are actively seeking new credit.

On the other hand, a soft pull, also known as a soft inquiry, is a credit check that doesn't impact your credit score. Soft pulls occur when you check your own credit report, when a lender pre-approves you for an offer, or when a potential employer checks your credit as part of a background check. Soft pulls are not visible to other lenders and do not affect your creditworthiness.

When discussing credit inquiries, it's important to differentiate between hard inquiries and soft inquiries.

A hard inquiry, often referred to as a hard inquiry, takes place when a lender or creditor examines your credit report during the process of applying for a new credit card or loan. These hard inquiries can have a minor impact on your credit score and are visible to other lenders. They signal that you're actively seeking additional credit, which could potentially affect your creditworthiness.

Conversely, a soft inquiry, also known as a soft inquiry, is a credit check that does not influence your credit score. Soft inquiries occur when you personally review your credit report, when a lender pre-approves you for an offer, or even when a potential employer conducts a background check involving your credit history. Importantly, soft inquiries remain hidden from other lenders and hold no bearing on your creditworthiness.

The difference in impact on your credit score between hard and soft inquiries is significant. A hard inquiry can cause a small dip in your credit score, usually by a few points. This occurs because it suggests that you're actively pursuing new credit lines, potentially raising concerns about your ability to handle additional debt responsibly. On the other hand, soft inquiries have no effect on your credit score whatsoever. They are merely recorded for informational purposes and have no bearing on your creditworthiness or lending decisions.

Let's say you have a credit score of 750 and you decided to apply for a new credit card. The credit card company performs a hard inquiry on your credit report as part of the application process. As a result, your credit score might experience a small drop, perhaps around 5 points. This drop occurs because the new credit inquiry suggests that you are actively seeking additional credit, which could potentially increase your credit risk.

On the other hand, it is important to be aware of your credit score and manage your credit responsibly. You can regularly check your credit report to monitor your financial health. When you access your own credit report to review your accounts and verify your information, it's considered a soft inquiry. This action has absolutely no impact on your credit score. Other lenders do not see this activity, and it doesn't influence your creditworthiness in any way.

By following this step-by-step guide, you can easily check your credit score and stay informed about your credit standing. Taking control of your credit health will empower you to make sound financial decisions and work towards a more secure financial future. Enlist the help of the Bright Money App to guide you through your journey to better credit.

Make full use of your credit card. Here’s how you can use your credit card to build your credit score.