You are now leaving the Bright website and entering a third-party website. Bright has no control over the content, products, or services offered, nor the security or privacy of information transmitted to others via their website. We recommend that you review the privacy policy of the site you are entering. Bright does not guarantee or endorse the products, information, or recommendations provided on any third-party website.

Credit cards can help greatly to improve credit scores. They are an effective credit-building tool. Essentially, when you use a credit card to build credit, you demonstrate your financial responsibility. If you want to understand credit better, we have just the perfect guide for you!

Each on-time payment and sensible spending decision is a positive mark on your credit history, helping to build credit and raise your credit score.

Let’s take a look at what you need to do to build your credit with a credit card.

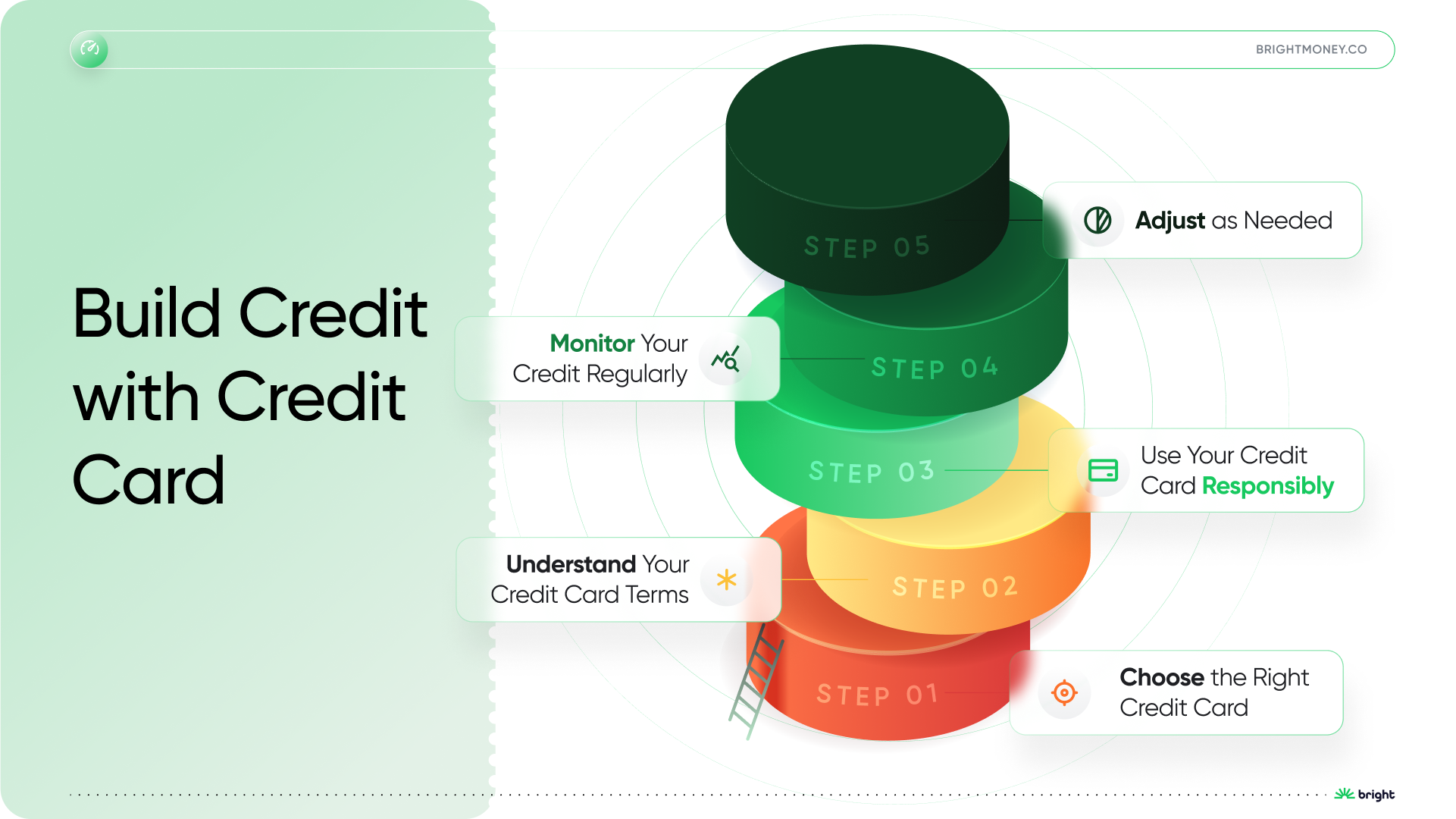

Step-by-Step Guide to Building Credit with a Credit Card

Building credit with a credit card may seem like a daunting task, but it doesn't have to be. By following a step-by-step approach, you can navigate this journey with confidence.

Let's break it down:

Step 1: Choose the Right Credit Card

Your first step is to choose a credit card that suits your situation. Whether it's a secured card, a student card, or a card designed for bad credit, the right card can set the stage for your credit-building journey.

The best card for you is one that matches your spending habits and financial goals. Research different cards, compare their features and benefits, and select the one that aligns with your needs.

Step 2: Understand Your Credit Card Terms

Once you have your card, take the time to understand its terms and conditions. Know your interest rate, credit limit, and any fees associated with the card. Here’s a look into the terms and conditions you need to keep an eye on:

Critical Terms:

Terms that can greatly affect your credit history and credit health can be classified as critical terms. These are:

1. APR (Annual Percentage Rate)

APR stands for "Annual Percentage Rate" and is an important term found on credit card statements. It represents the annualized interest rate charged by the credit card issuer on outstanding balances and certain transactions, expressed as a percentage.

The APR on a credit card statement reflects the cost of borrowing money on that credit card over a year, but it's important to note that credit card balances are typically revolving, and the APR is applied monthly based on the average daily balance. This means that the interest charges are added each month to the outstanding balance, affecting the following month's calculation.

The APR can vary depending on the type of transaction. Common types of APR you may find on a credit card statement include:

- Purchase APR: The interest rate applied to regular purchases made using the credit card.

- Cash Advance APR: The higher interest rate applied to cash advances taken from the credit card. Cash advances usually have no grace period, so interest starts accruing immediately.

- Balance Transfer APR: The interest rate applied to balances transferred from one credit card to another. Balance transfer APRs may be lower or promotional at times, but they usually have a specific time limit.

It's important to pay attention to the APR mentioned on your credit card statement because it affects how much interest you will be charged if you carry a balance from one billing cycle to the next. Responsible credit card usage involves understanding the terms of your credit card, paying your balance in full each month (if possible), and being aware of the APR and how it affects your overall credit card costs.

2. Grace Period

The grace period on a credit card statement refers to the period of time during which you can pay your credit card balance in full without incurring any interest charges. It is the gap between the end of your billing cycle (statement date) and the payment due date for that billing cycle.

During the grace period, which is usually around 21 to 25 days, you have the opportunity to pay off your entire credit card balance from the previous billing cycle without incurring any interest on purchases (assuming you had no outstanding balance from previous months). This means that if you pay your balance in full within the grace period, you essentially get an interest-free loan for that specific billing cycle.

However, it's important to note that not all credit card transactions qualify for a grace period. Cash advances and balance transfers, for example, typically start accruing interest immediately, with no grace period.

To take advantage of the grace period and avoid paying interest, it's essential to understand your credit card's billing cycle and payment due date. Always aim to pay your credit card bill in full and on time to avoid interest charges and maintain a healthy credit history. If you carry a balance, interest will be applied to the remaining amount, and future purchases may also start accruing interest from the transaction date without a grace period until the balance is fully paid off.

3. Minimum Payment

The minimum payment on a credit card statement is the smallest amount of money you are required to pay by the due date to keep your credit card account in good standing. It is a specific portion of your outstanding balance that the credit card issuer mandates you to pay each billing cycle.

The minimum payment amount is calculated based on various factors, including your outstanding balance, interest charges, fees, and any late payment fees from the previous billing cycle. The credit card company typically sets the minimum payment as a small percentage of the total outstanding balance, often around 1% to 3%, or a fixed dollar amount, whichever is higher.

While paying the minimum amount by the due date ensures that you won't be charged a late fee or negatively affect your credit score, it's important to understand that paying only the minimum is not sufficient to avoid interest charges entirely. If you carry a balance on your credit card from month to month, the remaining balance will accrue interest, and interest charges will be added to your next billing cycle.

Ideally, you should strive to pay your credit card balance in full each month to avoid interest charges and maintain good financial health. If you can't pay the full balance, paying more than the minimum will help reduce the overall interest costs and expedite the process of paying off the debt. It's crucial to be aware of the terms and conditions of your credit card, including the minimum payment requirement, to manage your finances responsibly.

4. Credit Limit

The credit limit on a credit card statement is the maximum amount of money that the credit card issuer allows you to borrow or charge on that particular credit card account. It represents the upper boundary of how much you can spend using the card before the issuer may decline further transactions or charge an over-limit fee.

The credit limit is set by the credit card issuer based on various factors, including your creditworthiness, income, credit history, and other financial considerations. It serves as a risk management tool for the issuer, as it helps prevent cardholders from accumulating excessive debt that they may struggle to repay.

For example, if your credit card has a credit limit of $5,000, you can make purchases and transactions up to that amount. Once your charges reach or exceed the credit limit, you will not be able to use the card for additional purchases until you pay down the balance and free up available credit.

It's crucial to manage your credit card spending responsibly and keep track of your usage relative to the credit limit. Keeping your credit utilization ratio (the percentage of your credit limit you are currently using) low is beneficial for your credit score. High credit utilization can negatively impact your creditworthiness, so it's generally advisable to stay below 30% of your credit limit, if possible.

Credit card issuers may periodically review your account and may consider increasing your credit limit based on your payment history, credit score, and financial situation. However, it's essential to use credit cards responsibly and only charge what you can afford to pay back in a timely manner.

5. Due Dates:

The due date on a credit card statement is the specific date by which you must make at least the minimum payment on your credit card balance to avoid late fees, penalties, and a negative impact on your credit score. It is the deadline set by the credit card issuer for you to make a payment for the charges accrued during the billing cycle.

The due date is typically mentioned on the credit card statement, and it falls a certain number of days after the statement date (closing date). This gives you time to review your statement, understand your outstanding balance, and make the necessary payment on time.

It's important to note that paying the minimum amount due by the due date will keep your credit card account in good standing, but it's not the ideal way to manage your credit card debt. If you only pay the minimum, the remaining balance will be subject to interest charges, and it may take a long time to pay off the debt in full. Paying off the full statement balance by the due date is the best way to avoid interest charges and maintain a positive credit history.

It is essential to be aware of your credit card's due date and to make timely payments to keep your credit in good standing and to avoid unnecessary fees and penalties. Missing the due date can lead to late fees, a potential increase in your APR, and negative marks on your credit report. Set up reminders or automatic payments if needed to ensure you never miss a credit card payment.

6. Penalty Fees

A penalty fee on a credit card statement is an additional charge imposed by the credit card issuer when the cardholder fails to adhere to certain terms and conditions outlined in the credit card agreement. These fees are applied as a consequence for specific actions or oversights on the part of the cardholder. Common penalty fees on credit card statements include:

- Late Payment Fee: This fee is charged when the cardholder fails to make the minimum payment or the full payment by the due date mentioned on the credit card statement. It's essential to pay at least the minimum amount on time to avoid this fee

- Over-Limit Fee: If the cardholder exceeds their credit limit by making purchases or incurring charges beyond their available credit, an over-limit fee may be charged. However, many credit card issuers have stopped charging over-limit fees, and they will simply decline transactions that would exceed the credit limit

- Returned Payment Fee: This fee is charged when a payment made by check or electronic means bounces or is returned due to insufficient funds or other reasons

- Foreign Transaction Fee: While not strictly a penalty fee, this fee is charged when a cardholder makes a purchase in a foreign currency or with a merchant located outside the cardholder's home country

- Cash Advance Fee: This fee is applied when a cardholder uses their credit card to obtain cash from an ATM or through cash-like transactions

- Balance Transfer Fee: While not necessarily a penalty, some credit card issuers charge a fee for transferring a balance from one credit card to another.

It's essential to read and understand the terms and conditions of your credit card agreement to be aware of the potential penalty fees that may apply. To avoid penalty fees, pay your credit card bill on time, stay within your credit limit, and be aware of any fees associated with specific transactions or actions. If you have questions about any fees on your credit card statement, you can contact your credit card issuer for clarification.

7. Bill Date

The bill date on a credit card statement is the specific date on which the credit card company generates your monthly statement. It is also known as the statement date or closing date. Each month, the credit card company calculates all the transactions made on your credit card from the previous statement date to the current statement date.

The bill date is essential because it marks the end of your billing cycle, and it's when your credit card statement is generated. After this date, you will no longer be able to add new charges to that specific statement; any transactions made after the bill date will be included in the following month's statement.

For example, if your bill date is the 15th of every month, the credit card company will generate your statement on or around the 15th. The statement will list all the transactions made on your credit card account from the 16th of the previous month to the 15th of the current month.

It's important to pay attention to the bill date because it indicates the deadline for paying the minimum amount due or the entire outstanding balance to avoid any late fees or interest charges. The payment due date is typically a few days after the bill date, giving you time to review your statement and make the necessary payment before the due date.

Secondary Terms:

1. Cash Advances

A high APR can be charged for withdrawing cash from your credit card. Check the terms and conditions regarding cash advances on your credit card and avoid them unless it's an emergency, as they can lead to significant debt.

2. Balance Transfers

A balance transfer refers to the process of shifting existing debt from one credit card to another, often involving the use of a new card. Understand the balance transfer fee and the duration of the promotional APR.

3. Rewards Program

It allows you to earn points, cash back, or miles for using your credit card for purchases. Choose rewards that align with your spending habits, and understand any restrictions.

4. Annual Fee

This is the yearly charge for having a credit card. Evaluate whether the benefits outweigh the cost, especially for low usage.

Understanding these details can help you avoid costly mistakes and make the most of your credit card. Also, be aware of any rewards or benefits your card offers. These can provide additional value, but only if you use them responsibly.

Step 3: Use Your Credit Card Responsibly

Using your credit card responsibly is critical to building credit. This means making payments on time, keeping your balance low, and not maxing out your credit limit. Good credit habits today can lead to a better credit score tomorrow. Try to pay your balance in full each month to avoid interest charges, and if that's not possible, at least make the minimum payment on time. Always keep track of your credit card.

Keeping track of your credit card involves monitoring various essential factors to maintain good financial health and responsible credit card use. The main factors to keep track of are:

- Balance: Regularly check your credit card balance to ensure you don't exceed your credit limit and to manage your overall debt

- Credit Utilization Ratio: This is the percentage of your credit limit that you are currently using. Aim to keep it low, ideally below 30%, as high utilization can negatively impact your credit score

- Due Dates: Always be aware of your payment due dates to avoid late fees and negative effects on your credit score

- Minimum Payment: Understand the minimum amount you need to pay each month to keep your account in good standing, though it's advisable to pay more than the minimum to reduce interest charges

- Interest Rate (APR): Be aware of the APR on your credit card, especially if you carry a balance. High APRs can lead to significant interest costs over time

- Introductory Offers: If you have a card with a promotional offer (e.g., 0% APR), track when the promotional period ends and when regular rates apply

- Rewards and Benefits: Understand the rewards program and benefits offered by your credit card to make the most of it without overspending

- Fees: Be aware of any annual fees, late payment fees, balance transfer fees, or other charges associated with your card

- Fraud Monitoring: Keep an eye on your transactions regularly to detect any unauthorized or fraudulent charges

- Credit Score: Monitor your credit score regularly to track how your credit card usage and other financial activities are impacting your overall creditworthiness.

By staying on top of these factors, you can use your credit card responsibly, build a positive credit history, and avoid potential financial pitfalls.

Step 4: Monitor Your Credit Regularly

Keep an eye on your credit score and credit report. Regular monitoring can help you understand how your credit card usage affects your score and spot any errors on your credit report. Credit partners like Bright Money can help you with this.

Many credit card issuers offer free credit score access, and you can get a free credit report from each of the three major credit bureaus once a year through tools or sites like AnnualCreditReport.com. You will learn more about how credit reports are in the following section.

Step 5: Adjust as Needed

Finally, be ready to adjust your credit card usage based on your credit score and financial goals.

If you notice your score dipping, it might be time to reassess your credit habits. You may need to lower your credit utilization or diversify your credit mix.

Wield your credit card wisely, and monitor your credit regularly - every swipe, every payment, and every decision you make can bring you one step closer to your financial goals.

Bright Money’s App can guide your credit card usage to build better credit every step of the way! Download the app today!

Credit cards are an essential tool to help you build credit. But how do they work? Learn more!