.jpg)

You are now leaving the Bright website and entering a third-party website. Bright has no control over the content, products, or services offered, nor the security or privacy of information transmitted to others via their website. We recommend that you review the privacy policy of the site you are entering. Bright does not guarantee or endorse the products, information, or recommendations provided on any third-party website.

Credit cards have rapidly evolved as essential tools for making purchases and issuing payments in today's fast-paced world. They also offer several benefits, such as an improved credit score, rewards, cash back, etc. However, along with this ease comes the need to carefully manage your cash. This includes being able to interpret your credit card statement in its entirety. You can track your expenses, stay on top of your finances, and safeguard yourself from fraud by studying your monthly account statement.

This guide walks you through every aspect of using a credit card and helps you discover credit card statements in a new light, arming you with the knowledge needed to use credit cards wisely.

Read more: How to Build Your Credit With a Credit Card?

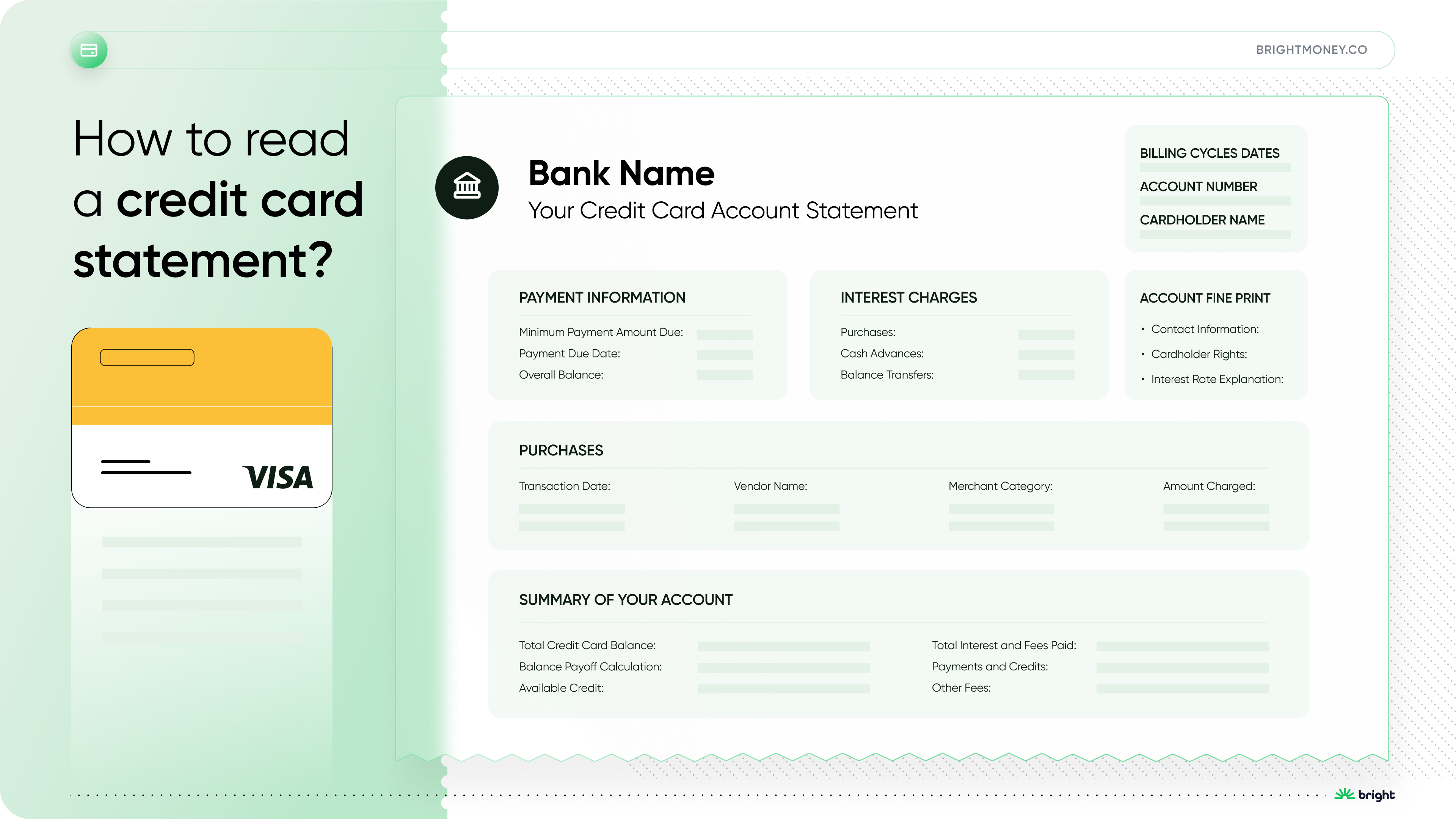

Understanding Statements

A credit card statement is a monthly summary of your credit card activity and is essential for tracking your spending, monitoring transactions, and managing your finances effectively. Let's delve into each section of the statement:

1. Balance Transfer

If you've utilized a balance transfer option, you might find specific details about it in this section. Balance transfers can be a useful tool to consolidate debt from one or more cards onto a single card with a lower interest rate. However, be mindful of introductory rates, transfer fees, and the duration of the promotional period.[4]

2. APR (Annual Percentage Rate)

The APR is a crucial factor in understanding the cost of borrowing on your credit card. It represents the annualized interest rate you'll be charged on any outstanding balance if you carry it from one billing cycle to the next. Knowing your APR helps you assess the impact of interest on your overall debt and make informed decisions about repayment strategies.[5]

3. Due Date

The due date is the deadline for making your monthly payment. It's imperative to make payments on or before this date to avoid late fees and potential damage to your credit score. Setting up reminders or automatic payments can help ensure timely payments.[6]

4. Minimum Payment Due

The minimum payment due is the smallest amount you must pay each month to keep your account in good standing. While paying the minimum is necessary, paying more than the minimum can save you money in interest and help you pay off your balance faster.[6]

5. Purchases

The "Purchases" section offers specific details of each transaction made with your credit card:

- Transaction Date: This date indicates when the purchase was processed, which may differ from the date of the actual transaction

- Vendor Name: The name of the merchant where the purchase was made is mentioned in this column. If you encounter an unfamiliar name, contacting the card issuer can provide more information for verification

- Merchant Category: Each vendor is assigned a Merchant Category Code (MCC) that identifies its business type. Rewards cards often offer higher or better rewards for specific categories based on these codes

- Amount Charged: This is the total amount charged to your credit card for each individual transaction[1]

6. Payment Details

This section focuses on your credit card statement balance, payment options, and interest calculations:

- Total Credit Card Balance: Representing the total amount currently charged to your credit card, paying this amount clears your outstanding balance and resets the credit owed to zero

- Minimum Payment Amount Due: Credit card issuers calculate the minimum payment as a percentage of your balance or a percentage plus interest and fees. Aim to pay more than the minimum to avoid prolonged debt

- Balance Payoff Calculation: Issuers must provide information on how long it will take to pay off your balance if you make only the minimum payments each month. They may also show how paying more will expedite the payoff and save on interest costs

- Available Credit: This section displays the remaining credit available for spending until you reach your credit limit. Keeping your credit utilization rate under 30% is beneficial for your credit score

- Total Interest and Fees Paid: The statement shows the total interest or fees paid throughout the year, providing an overview of the cost of borrowing[1]

7. Account Fine Print

The fine print contains essential legal information and your rights as a cardholder:

- Contact Information: Details on how to reach your credit card issuer by phone, postal mail, or online channels are available

- Cardholder Rights: This section outlines your rights as a cardholder, including acceptable payment methods, credit bureau reporting practices, and the process for resolving account discrepancies

- Interest Rate Explanation: Clear explanations of how your credit card issuer calculates interest on balances subject to finance charges. It also has recommendations for avoiding additional interest by paying your balance in full and on time[1]

8. Interest Charges

The "Interest Charges" section breaks down the various Annual Percentage Rates (APRs) applicable to your credit card:

- Purchases: Most credit cards have variable APRs that fluctuate in line with changes in the Prime Rate. Monitoring these rates helps you anticipate any changes in your interest costs

- Cash Advances: Cash advances typically come with higher APRs than regular purchases, making them an expensive way to borrow money. It is best to explore alternative methods for obtaining cash

- Balance Transfers: This section shows the interest rate on any balances you transferred to the card. If you took advantage of an introductory 0% APR offer for balance transfers, the statement should include the expiration date of this promotion[1]

Understanding Accounts

Your credit card account is a financial tool that requires responsible management to build and maintain good credit. Understanding the various aspects of your account is essential for effective credit management:

1. Account Details

Your credit card statement begins with essential details about your account, which are vital for accurate reporting and identification:

- Personal Information: Your name and mailing address are the cornerstones of your credit card account. Always ensure they are spelled correctly for efficient, error-free communication with the credit card company and accurate credit reporting

- Account Number: The account number, whether displayed in its entirety or masked with the last four digits, serves as your unique identifier. It is essential to safeguard this information to prevent unauthorized access to your account

- Billing Cycle Dates: Understanding the dates of your billing cycle is crucial for tracking transactions and payment due dates. Purchases made after the closing date of the billing cycle will appear in the following month's statement[1]

2. Account Overview

The account summary provides an overview of your credit card activity, including balances and fees:

- Payment Due Date: Credit card issuers are obligated to specify a date on which the payment falls due every month, allowing you a minimum of 21 days after the closing date to make payments

- Payments and Credits: This section records any payments made and credits received during the billing cycle, ensuring transparency in your account transactions

- Overall Balance: The total amount owed on your credit card represents the sum of your outstanding charges and any accrued interest or fees

- Other Fees: In this subsection, you'll find a breakdown of additional charges, such as late fees, foreign transaction fees, and balance transfer fees[1]

3. Rewards

If your credit card offers rewards, the "Rewards" section summarizes your activity during the billing cycle:

- Rewards Balance Prior: This displays the rewards accumulated in previous billing cycles, which may be available for redemption

- Rewards Earned: The rewards earned during the current billing cycle that show your progress toward maximizing rewards are shown here

- Rewards Redeemed: Any rewards you redeemed during the billing cycle, which can range from cashback to travel perks or other redemption options, are shown here

- Amount Available for Redemption: This column shows the total rewards available for redemption, highlighting the value you can gain from your credit card rewards program[1]

Take charge of your finances today! Sign up for Bright Money for better control of your credit card usage and ensure your financial well-being.

Avoiding Common Credit Card Pitfalls

While credit cards offer many benefits, they can also lead to financial trouble if not used responsibly. Here are some common pitfalls to avoid:

- High Credit Card Balances: Carrying a high balance from month to month can lead to mounting interest charges and debt. Aim to pay off your credit card balance in full whenever possible

- Missing Payments: Late payments not only mean you incur late fees, but they also negatively impact your credit score. Set up reminders to ensure you pay your credit card bills on time

- Overspending: Credit cards can make overspending beyond your means easy. Stick to a budget and use credit responsibly

- Ignoring Statements: Failing to review your credit card statement can lead to overlooking errors or fraudulent charges. Regularly review your statements and contact your issuer if you spot any problems

- Opening Too Many Credit Accounts: Opening multiple credit cards in a short period can negatively affect your credit score. Only apply for new credit when necessary[2]

Read more: Top 10 common credit card mistakes and ways to avoid them.

Utilizing Online Account Management Tools

Credit management platforms like Bright Money, provide online account access and mobile apps that offer a range of helpful tools for managing your credit card account. Through these platforms, you can:

- View Real-Time Transactions: Keep track of your purchases, payments, and credit balances in real time (as transactions occur). This allows you to monitor your spending more effectively

- Set Up Payment Reminders: Avoid missing payment due dates by setting up payment reminders through email or text alerts. You may also consider setting up standing instructions to pay off your credit card bills on time

- Access E-Statements: Opt for electronic statements to receive your credit card statement via email, reducing paper clutter and ensuring secure delivery

- Monitor Your Credit Score: Many issuers now offer free credit score monitoring, enabling you to track changes in your creditworthiness over time

- Dispute Transactions: If you spot any unauthorized or erroneous charges, you can initiate a dispute through the online platform

You can keep track of your credit card usage, send payments on schedule, and take proactive measures to better your financial situation by using Bright Money’s application. To get the most out of these capabilities and improve your credit card experience, keep in mind to frequently go into your account and explore all of the options.[3]

Conclusion

Your credit card statement holds the key to managing your finances effectively, safeguarding your creditworthiness, and making the most of the credit card benefits received in the form of rewards, cashback, interest-free credit, etc. By learning to interpret each section of your statement, you can stay informed about your spending, make timely payments, and detect any unauthorized activity promptly.

Regularly reviewing your credit card statement empowers you to take control of your financial journey since you always know what is a statement balance on a credit card, setting you on the path to financial success and security.

While the layout may vary among credit card issuers, the fundamental information remains consistent across all statements. Embrace this knowledge, and embark on a journey toward financial awareness and responsible credit card usage with these tips and pointers.

Ready to make the most of your credit card benefits? Join Bright Money now and unlock personalized insights for responsible credit card management.

References:

- https://www.forbes.com/advisor/credit-cards/how-to-read-your-credit-card-statement/

- https://www.cnbc.com/select/common-credit-card-mistakes/

- https://www.freshbooks.com/hub/accounting/account-management-software

- https://www.investopedia.com/credit-cards/balance-transfer-credit-card/#:~:text=Key%20Takeaways-,Credit%20card%20balance%20transfers%20are%20typically%20used%20by%20consumers%20who,months%2C%20though%20some%20are%20longer

- https://www.consumerfinance.gov/ask-cfpb/what-is-a-credit-card-interest-rate-what-does-apr-mean-en-44/#:~:text=A%20credit%20card's%20interest%20rate,month%20by%20the%20due%20date

- https://www.paisabazaar.com/credit-card/credit-card-billing-cycle/#:~:text=Your%20credit%20card%20due%20date,26th%20of%20the%20same%20month

FAQs

Q. What should I do if I notice an error on my credit card statement?

If you spot an error on your credit card statement, it's essential to take immediate action. First, contact your credit card issuer's customer service to report the discrepancy and request clarification. They will guide you through the dispute process and may issue a temporary credit card while investigating the matter. Additionally, it's advisable to follow up in writing, sending a letter to the credit card issuer detailing the error and your concerns.

Q. Is it necessary to keep physical copies of my credit card statements if I receive e-statements?

While keeping physical copies of your credit card statements can be helpful for record-keeping purposes, it's not a strict requirement if you receive e-statements. E-statements are typically accessible through your online account, allowing you to review past statements as needed. However, for important transactions or tax-related purposes, you may consider downloading and saving electronic copies in a secure location.

Q. Can I negotiate credit card fees and interest rates with my issuer?

Yes, you can negotiate credit card fees and interest rates with your issuer. If you have a good payment history and a strong credit score, you may have better leverage in negotiating lower interest rates or having certain fees waived. It's best to call your credit card issuer's customer service and discuss your situation. While they may not always agree to your request, it doesn't hurt to inquire about and advocate for better terms.

Q. What happens if I miss the payment due date on my credit card statement?

Missing the payment due date on your credit card statement can have several consequences. Most credit card issuers will charge a late payment fee, which can vary depending on your credit card terms. Additionally, your credit card issuer may report the late payment to credit bureaus, leading to a negative impact on your credit score. Consistent late payments can severely affect your creditworthiness and make it challenging to obtain favorable credit terms in the future.

Q. Should I always pay off my credit card balance in full every month?

Paying off your credit card balance in full every month is a recommended practice for responsible credit card usage. By doing so, you avoid accumulating interest charges and maintain better control over your finances. However, there might be situations where paying the full balance isn't possible. In such cases, aim to pay more than the minimum to reduce interest costs and work towards paying off the balance as quickly as you can.