You are now leaving the Bright website and entering a third-party website. Bright has no control over the content, products, or services offered, nor the security or privacy of information transmitted to others via their website. We recommend that you review the privacy policy of the site you are entering. Bright does not guarantee or endorse the products, information, or recommendations provided on any third-party website.

Have you ever found yourself in a situation where an unexpected expense left you thinking, "I need cash now"? If so, you're not alone. Life's financial curveballs can catch us off guard, leaving us in need of quick solutions. In fact, a recent survey found that over 60% of Americans face unexpected expenses each year, highlighting the pervasive nature of financial emergencies in our lives.

The truth is that unforeseen circumstances don't discriminate. Whether it is a medical emergency, a car repair, or a sudden home improvement project, these financial challenges can arise when we least expect them. In these moments, having a reliable and effective financial tool at your disposal becomes essential.

Let's be honest: the typical financial environment can be confusing and intimidating. The multitude of options, from loans to credit cards, can leave you feeling confused and uncertain about the best path forward. That's where Bright Money comes in. We're here to help you navigate the often murky waters of personal finance, offering clarity, guidance, and a roadmap to financial wellness.

In today's fast-paced world, it is not enough to merely save money; you need to save smarter. According to a recent study by the National Endowment for Financial Education, over 56% of Americans have less than $1,000 in savings, emphasizing the importance of effective financial planning. Bright Money is your partner on this journey, empowering you to make informed decisions, helping you achieve your financial goals, and enabling you to secure your finances for a better future.

Join us as we dive into the world of financial options, exploring the differences between a Home Equity Line of Credit (HELOC) and a Personal Loan. We'll help you answer that burning question: Which option is the right choice when you need cash now?

Read more: Need Instant Cash? Top 10 Apps to Borrow From!

Need of Cash Now: Should I Choose a HELOC or a Personal Loan?

When you need cash urgently, deciding between a Home Equity Line of Credit (HELOC) and a Personal Loan can be crucial. To determine the right choice, consider your financial circumstances, needs, and the urgency of the situation. HELOCs typically offer lower interest rates but require collateral (your home), while Personal Loans provide unsecured funds but may have higher interest rates.

Understanding Your Financial Needs

Before diving into the specifics of HELOCs and Personal Loans, it is essential to assess your financial needs and goals. Understanding the nature and urgency of your financial requirements will greatly influence your choice.

1. Immediate Cash vs. Long-Term Financial Planning

Consider whether your need for cash is an immediate, short-term requirement or part of a long-term financial plan. If you need money quickly to cover unexpected expenses or bridge a tiny funding gap, a personal loan may be more suitable. Conversely, if you're looking to finance a home improvement project or consolidate high-interest debt, a HELOC might align better with your long-term financial goals.

2. Loan Amount and Term

Determine the amount of money you require and how long you'll need it. Personal loans typically offer a lump sum amount with fixed monthly payments over a predetermined term. On the other hand, HELOCs provide a line of credit that you can draw from as needed, often with a longer repayment period.

3. Collateral and Risk Tolerance

Your comfort level with putting up collateral and assuming financial risk should also factor into your decision. A HELOC is secured by your home, making it a secured loan. If you fail to make payments, you risk losing your home. Personal loans are typically unsecured, which means they do not require collateral. However, they may have higher interest rates to compensate for the increased risk for the lender.

4. Interest Rates and Fees

Compare the interest rates and associated fees for both HELOCs and personal loans. The interest rates on HELOCs are often variable, while personal loans typically have fixed rates. The interest rate structure can significantly impact the overall cost of borrowing.

5. Credit Score and Eligibility

Your credit score and financial history play a significant role in determining your eligibility and the terms you can secure. HELOCs may require a higher credit score and better financial standing due to their secured nature. Personal loans are more accessible to individuals with various credit profiles.[1][4]

Unlock Financial Freedom Today! Sign Up for Bright Money and Take Control of Your Finances.

Now that you've assessed your financial needs, let's delve deeper into the specifics of HELOCs and Personal Loans.

Home Equity Line of Credit (HELOC)

A Home Equity Line of Credit, commonly known as HELOC, is a financial product that allows homeowners to leverage the equity they've built up in their property. It operates as a revolving line of credit, similar to a credit card, where borrowers can access funds as needed up to a predetermined credit limit. The credit limit is typically based on a percentage of the home's appraised value minus any outstanding mortgage balance. HELOCs are secured loans, meaning your home serves as collateral, making them less risky for lenders and often resulting in lower interest rates compared to unsecured loans like credit cards or personal loans.

One of the primary advantages of a HELOC is its flexibility. Borrowers can use the funds for various purposes, such as home improvements, debt consolidation, education expenses, or unexpected financial needs. Unlike a traditional home equity loan, where you receive a lump sum, a HELOC allows you to borrow only what you need when you need it, which can save you money on interest. HELOCs also typically have variable interest rates, meaning your rate and monthly payments can fluctuate based on market conditions. Understanding how HELOCs work and their potential benefits and drawbacks is crucial for homeowners considering this financial tool.[2]

Join Thousands of Smart Savers. Get Started with Bright Money for a Brighter Financial Future!

Personal Loan

A personal loan is a versatile financial product that provides individuals with a lump sum of money, typically unsecured, meaning it doesn't require collateral like your home or car. Borrowers can use personal loans for various purposes, such as consolidating debt, covering medical expenses, funding home renovations, or even taking a dream vacation. One of the key features of personal loans is that they come with fixed interest rates and fixed repayment terms, providing predictability and structure to borrowers.

These loans are typically repaid in monthly instalments over a predetermined period, which can range from two to seven years, depending on the lender and the loan amount. Personal loan eligibility and interest rates are influenced by factors like your credit score, credit history, income, and the lender's policies. With a personal loan, borrowers have the advantage of knowing exactly how much they need to repay each month, making it easier to budget and plan for their financial obligations. Understanding the characteristics of personal loans and how they can be a useful financial tool is essential for individuals seeking to meet various financial goals while managing their finances responsibly.[3]

Don't Miss Out on Financial Wellness. Start Your Bright Money Journey Now. Sign Up Today!

Comparing HELOCs and Personal Loans

To help you make an informed decision, let's compare HELOCs and Personal Loans based on various factors:

1. Interest Rates

- HELOC: Generally, HELOCs offer lower interest rates initially, but they are often variable, meaning they can rise over time. This can make budgeting more challenging as your monthly payments may fluctuate

- Personal Loan: Personal loans typically have higher fixed interest rates, which means you'll know your exact monthly payments from the start. This stability can be helpful for budgeting

Winner: The choice here depends on your preference for stable payments or lower initial rates. If you value predictability, a personal loan might be better.

2. Flexibility

- HELOC: HELOCs provide a revolving line of credit, allowing you to borrow and repay funds as needed during the draw period. This flexibility is ideal for ongoing expenses or projects with changing costs

- Personal Loan: Personal loans offer a lump sum upfront, making them suitable for one-time expenses. However, they lack the ongoing flexibility of a HELOC

Winner: If you need ongoing access to funds for various expenses, a HELOC is more flexible.

3. Collateral

- HELOC: HELOCs are secured by your home, putting your homeownership at risk if you default on payments

- Personal Loan: Personal loans are unsecured, so they don't require collateral. You won't risk losing your home or other assets

Winner: If you're uncomfortable with the idea of using your home as collateral, a personal loan is the safer option.

4. Eligibility and Approval

- HELOC: HELOCs typically require a higher credit score, substantial home equity, and a favorable debt-to-income ratio for approval

- Personal Loan: Personal loans are more accessible to individuals with varying credit profiles. You can often find options for borrowers with fair or even poor credit

Winner: If your credit score isn't strong, a personal loan may be the easier option to qualify for.

5. Loan Amount and Term

- HELOC: HELOCs usually offer higher credit limits, making them suitable for larger expenses. They also come with longer repayment terms

- Personal Loan: Personal loans may have lower maximum loan amounts and shorter terms, which can result in higher monthly payments

Winner: If you need a substantial amount of money for a long-term project, a HELOC may be more suitable. For smaller, short-term needs, a personal loan may suffice.

6. Tax Deductibility

- HELOC: In some cases, the interest paid on a HELOC used for home improvements may be tax-deductible. However, tax laws can change, so consult a tax professional for current information

- Personal Loan: Personal loan interest is generally not tax-deductible

Winner: If you plan to use the funds for home improvements and can benefit from potential tax deductions, a HELOC has an advantage in this aspect.[4]

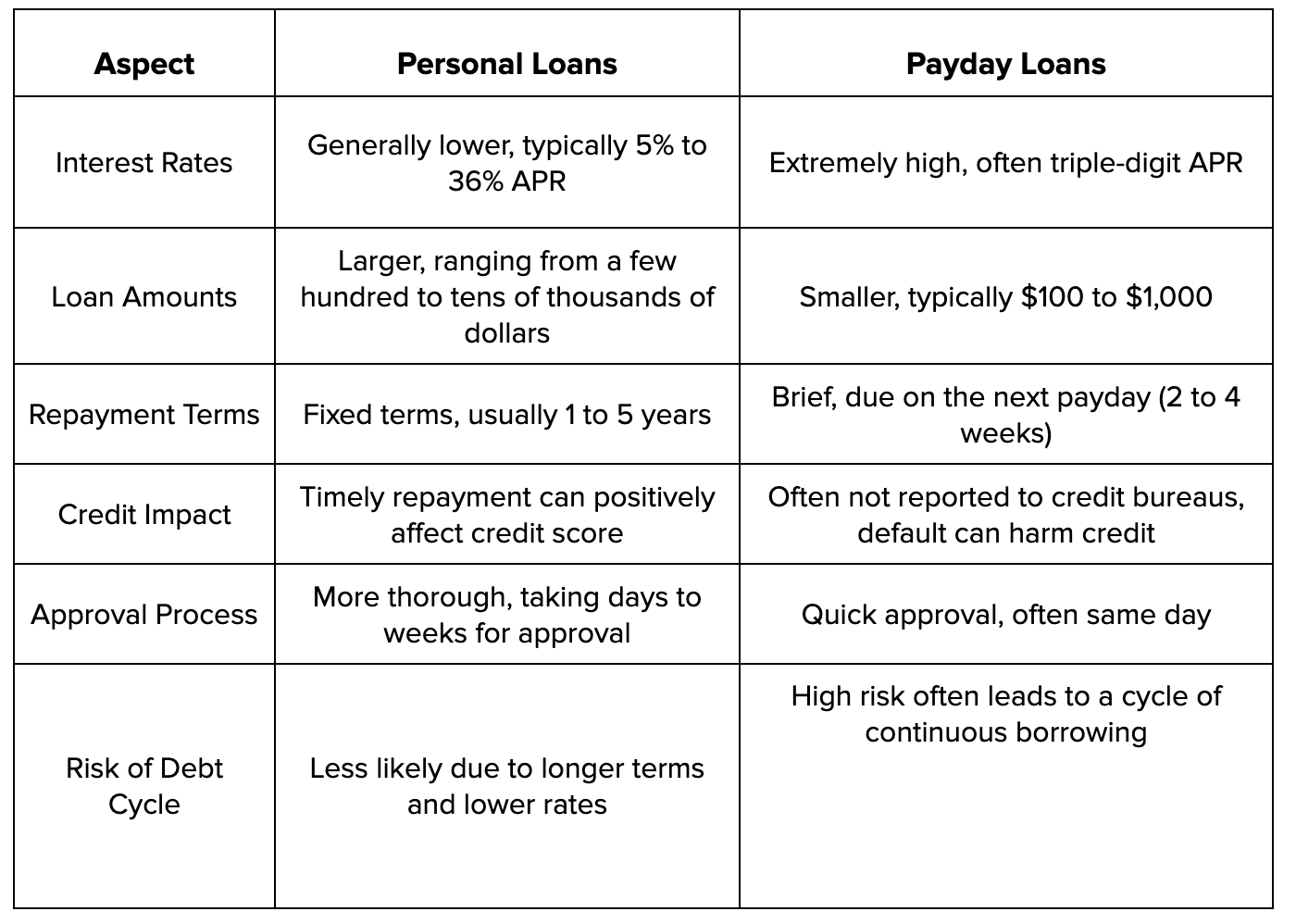

Certainly, here's a comparison table summarizing the key differences between HELOCs and Personal Loans:

This table provides a concise overview of how HELOCs and Personal Loans differ in terms of interest rates, flexibility, collateral requirements, eligibility, loan amounts, and potential tax benefits, helping borrowers make informed decisions based on their specific needs and preferences.

Ready to Save Smarter and Achieve Your Financial Goals? Join Bright Money Today!

Making Your Decision

Ultimately, the choice between a HELOC and a Personal Loan depends on your unique financial situation, needs, and preferences. Here's a step-by-step guide to help you make the right decision:

- Assess Your Needs: Determine the nature, urgency, and amount of your financial need. Consider whether it is a short-term or long-term requirement

- Evaluate Your Risk Tolerance: Decide whether you're comfortable using your home as collateral for a HELOC or prefer an unsecured personal loan

- Check Your Credit Profile: Review your credit score and financial history to understand your eligibility for each option and the terms you may qualify for

- Compare Interest Rates: Consider whether you prefer the lower initial rates of a HELOC or the stability of fixed rates with a personal loan

- Determine Loan Amount and Term: Calculate the exact amount you need and the length of time you'll need to repay it. This will help you decide which loan product aligns with your requirements

- Factor in Flexibility: Consider whether you need ongoing access to funds (HELOC) or a one-time lump sum (Personal Loan)

- Research Lenders: Shop around and compare offers from different lenders. Pay attention to interest rates, fees, and repayment terms

- Seek Professional Advice: If you're unsure which option is best for you, consult with a financial advisor or loan specialist for personalized guidance

- Read the Fine Print: Before committing to any loan, carefully review the loan agreement and understand all terms and conditions

- Make Your Decision: Based on the above considerations and your individual circumstances, choose the financing option that best meets your needs.[1][4]

Read more: Can You Get a Loan With No Credit Check?

Conclusion

When faced with the urgent need for cash, deciding between a HELOC and a personal loan requires careful consideration. Your financial situation, risk tolerance, credit profile, and specific needs will play a pivotal role in determining which option is right for you.

Remember that both HELOCs and personal loans have independent advantages and disadvantages, and there is no one-size-fits-all solution. By evaluating the key factors discussed in this guide and seeking professional advice if needed, you can confidently make an informed decision and navigate your way through unexpected financial challenges while maintaining your financial well-being.

In any case, whether you choose a HELOC or a personal loan, responsible borrowing and timely repayments are essential to ensure your financial stability and protect your assets. So, when the next financial emergency arises, armed with this knowledge, you can confidently say, "I need cash now," knowing you have the information to make the right choice.

It Is Time to Say Goodbye to Financial Stress. Sign Up for Bright Money and Transform Your Finances Today!

References:

- https://www.marketwatch.com/picks/i-need-cash-now-should-i-opt-for-a-heloc-or-personal-loan-42f36bea#:~:text=One%20may%20borrow%20a%20relatively,rates%2C%20fees%20and%20possible%20penalties.

- https://www.investopedia.com/mortgage/heloc/

- https://www.investopedia.com/personal-loan-5076027

- https://www.moneygeek.com/mortgage/heloc-vs-personal-loan/#:~:text=How%20does%20a%20HELOC%20compare,come%20with%20fixed%20interest%20rates.

FAQs

- Can I get a HELOC or personal loan with bad credit?

Yes, it is possible to secure a HELOC or personal loan with less-than-perfect credit, but your options may be limited. For HELOCs, a higher credit score is often required, while personal loans may offer more flexibility for borrowers with lower credit scores. Be prepared to bear potentially higher interest rates and stricter terms if your credit is not strong.

- How long does it take to get approved for a HELOC or personal loan?

The approval process can vary depending on the lender and your financial situation. Typically, personal loans have a quicker approval process, often within a few days. HELOC approvals may take longer, ranging from a few weeks to a couple of months, due to the need for home appraisals and paperwork.

- Can I use a HELOC or personal loan for any purpose?

In general, you can use a personal loan for various purposes, such as medical expenses, debt consolidation, or home improvements. HELOCs are typically used for home-related expenses, like renovations, but can also be used for other financial needs. It is essential to clarify your intended use with the lender.

- What are the closing costs associated with a HELOC?

When opening a HELOC, you may encounter closing costs, which can include appraisal fees, application fees, and attorney fees. These costs vary by lender and location but are similar to the closing costs associated with a mortgage. Be sure to ask your lender for a breakdown of these expenses before proceeding.

- Can I pay off a HELOC or personal loan early without penalties?

Many lenders allow you to pay off a Personal Loan early without prepayment penalties, but it is crucial to confirm this with your lender before taking out the loan. HELOCs often have more flexible repayment terms, and some may not impose penalties for early repayment. Review your loan agreement or discuss this with your lender to understand your specific terms.