You are now leaving the Bright website and entering a third-party website. Bright has no control over the content, products, or services offered, nor the security or privacy of information transmitted to others via their website. We recommend that you review the privacy policy of the site you are entering. Bright does not guarantee or endorse the products, information, or recommendations provided on any third-party website.

In the world of personal finance, individuals often find themselves needing to borrow money to meet their financial needs or consolidate existing debts. Two common options for such scenarios are personal loans and balance transfer credit cards. Both of these financial tools serve specific purposes and come with their own sets of advantages and disadvantages.

In this comprehensive guide, we will delve deep into the realm of personal loans and balance transfer credit cards, comparing them in various aspects to help you make an informed decision.

Read more: What is a balance transfer?

Personal Loan vs. Balance Transfer

Personal loans are lump-sum amounts repaid in installments, offering financial flexibility for various needs. In contrast, balance transfers involve temporarily moving credit card debt to a new card with lower interest. Use personal loans for structured financing, like home improvement, and balance transfers for short-term debt reduction. Consider your financial goals and the need for fixed repayment terms or short-term interest relief when deciding between them.

Take the First Step Towards Financial Empowerment – Unlock the Doors to Your Financial Freedom with Bright Money. Sign Up Now to Begin Your Journey!

Understanding Personal Loans

Okay, let's talk about personal loans more relaxedly. So, what's a personal loan? It's like borrowing money from a bank, credit union, or an online lender for whatever you need. Unlike loans for specific things like cars or homes, personal loans are pretty flexible because you don't have to put up any collateral, like your car or house, to get one.

Here's the deal with personal loans: you get a set amount of money all at once, and then you pay it back over time with interest. The interest rate stays the same, and you make fixed monthly payments until the loan is paid off.

People use personal loans for all sorts of stuff, like combining high-interest debts, handling unexpected medical bills, sprucing up their homes, or even going on a well-deserved vacation. The key is to understand the terms, the interest rates, and how you will pay it back before you dive into a personal loan.[1]

Embark on a Journey of Smarter Saving – Let Bright Money Be Your Guide to Financial Prosperity. Get Started Now and Experience the Difference!

Understanding Balance Transfer Credit Cards

Alright, let's break down balance transfer credit cards in a way that's easy to grasp. So, what's the deal with these cards? They're like your secret weapon for tackling high credit card debt.

Here's how they work: You take your existing credit card debt, which might be raising tons of interest, and move it to a new card. The cool part? This new card often starts with a super low or even 0% interest rate for a while. This means you can catch a break from those pesky interest charges and focus on paying off the actual debt.

But there's a catch. This low or 0% interest rate usually only lasts for a specific time, like 12 or 18 months. So, it's like a temporary breather to help you pay down your debt faster. It's a smart move if you've got a plan to pay off that debt during that promo period. Just make sure to check the fine print and understand any fees or terms that might apply. Balance transfer credit cards are a handy tool to get your finances back on track, especially when you're dealing with credit card debt.[2]

Seize the Opportunity for Financial Success – Don't Let This Chance Slip Through Your Fingers. Sign Up Today to Embrace the Promise of Bright Money!

Comparing Personal Loans and Balance Transfer Credit Cards

Now that we clearly understand personal loans and balance transfer credit cards, let's compare these two financial tools in various aspects.

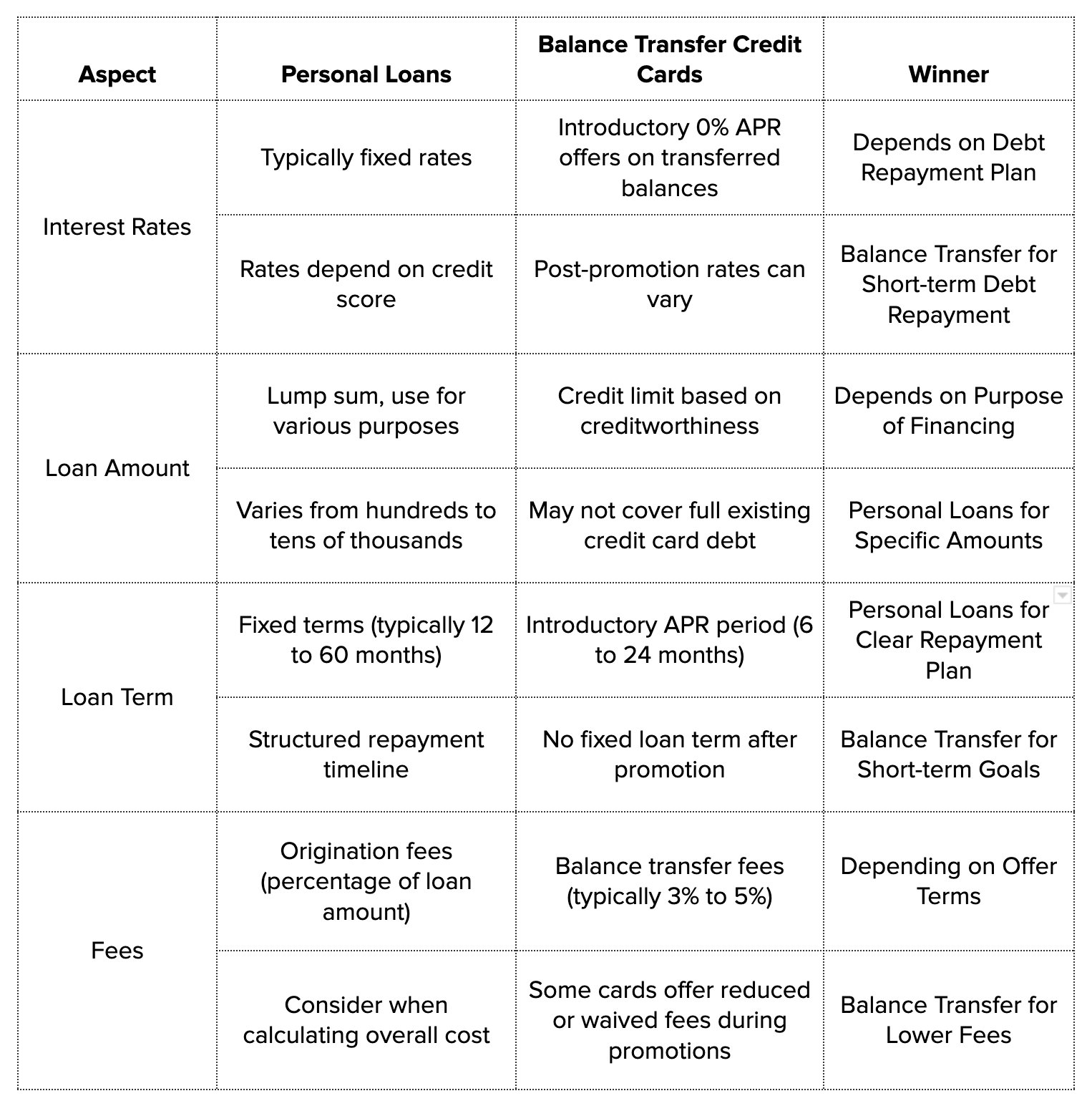

1. Interest Rates

Personal Loans

- Personal loans typically offer fixed interest rates

- The interest rates on personal loans depend on your credit score, with better scores leading to lower rates

- Rates can range from 6% to 36% or higher, depending on your creditworthiness and the lender's policies

Balance Transfer Credit Cards

- Balance transfer credit cards often come with introductory 0% APR offers on transferred balances

- After the promotional period, the interest rates can vary widely, potentially exceeding personal loan rates

Winner: For those who can pay off their debt within the promotional period, balance transfer credit cards offer an advantage with the 0% APR. However, personal loans provide more stability with fixed rates.[3]

2. Loan Amount

Personal Loans

- Personal loans provide a lump sum of money, which you can use for various purposes

- Loan amounts vary based on your creditworthiness and the lender's policies but can range from a few hundred dollars to tens of thousands

Balance Transfer Credit Cards

- The credit limit on a balance transfer card depends on your creditworthiness and the issuing bank

- It may not cover the full amount of your existing credit card debt

Winner: Personal loans are more suitable when you need a specific amount of money for a specific purpose, while balance transfer cards work well for consolidating existing credit card debt.[3]

3. Loan Term

Personal Loans

- Personal loans come with fixed loan terms that are typically 12 to 60 months

- Borrowers have a set timeline for repaying the loan

Balance Transfer Credit Cards

- The introductory 0% APR period on balance transfer cards usually lasts from 6 to 24 months

- After this period, the card's regular APR applies, and there is no fixed loan term

Winner: Personal loans provide a clear and structured repayment plan with fixed terms, whereas balance transfer cards have a limited interest-free period.[3]

4. Fees

Personal Loans

- Some personal loans may have origination fees, which are typically a percentage of the loan amount

- It's important to consider these fees when calculating the overall cost of the loan

Balance Transfer Credit Cards

- Most balance transfer cards charge a balance transfer fee, typically around 3% to 5% of the transferred balance

- Some balance transfer cards may offer reduced or waived fees during promotional periods

Winner: The winner depends on the specific terms offered by lenders and credit card issuers. Balance transfer cards may have lower fees if you can find a card with reduced or waived balance transfer fees.[3]

Certainly, here's a table summarizing the comparison between personal loans and balance transfer credit cards in various aspects:

Your Path to a Brighter Financial Tomorrow Begins Right Here – Take the Initiative and Register with Bright Money Today to Ignite Your Financial Destiny!

5. Credit Requirements

Personal Loans

- Obtaining a personal loan with favorable terms typically requires a good to excellent credit score

- Borrowers with poor credit may have limited options or face higher interest rates

Balance Transfer Credit Cards

- Qualifying for a balance transfer card with a 0% APR offer usually requires a good credit score

- Individuals with lower credit scores may still qualify for balance transfer cards but may receive shorter promotional periods or higher regular APRs

Winner: Individuals with good credit scores have better access to both personal loans and balance transfer cards. However, balance transfer cards may be more lenient with lower credit scores.[3]

6. Impact on Credit Score

Personal Loans

- Successfully repaying a personal loan can positively impact your credit score, as it demonstrates responsible borrowing and on-time payments

Balance Transfer Credit Cards

- Opening a new credit card account can temporarily lower your credit score due to the hard inquiry on your credit report

- Successfully paying down the transferred balance can positively impact your credit score

Winner: Both options have the potential to impact your credit score positively, but personal loans may have a more immediate and consistent effect.[3]

7. Debt Consolidation

Personal Loans

- Personal loans can be used for debt consolidation by paying off multiple debts and combining them into a single loan

Balance Transfer Credit Cards

- Balance transfer cards are specifically designed for consolidating credit card debt into one card with a lower interest rate

Winner: Balance transfer credit cards are tailored for debt consolidation, making them the clear winner for this purpose.[3]

8. Flexibility

Personal Loans

- Personal loans provide flexibility in using the borrowed funds, allowing you to address various financial needs

Balance Transfer Credit Cards

- Balance transfer cards are limited to consolidating and paying off existing credit card debt

Winner: Personal loans offer more versatility in terms of usage, making them suitable for a wider range of financial goals.[3]

Conclusion

We examined the nuances of these two financial instruments in the article "Personal Loan vs. Balance Transfer Credit Card: A Comprehensive Comparison." It's critical to keep in mind that there is no one-size-fits-all solution for managing debt or funding financial objectives. Your specific financial condition, goals, and preferences should guide your decision between a personal loan and a credit card with a balance transfer feature.

Choose a Personal Loan If:

- You need specific money for a defined purpose, such as home improvement or medical expenses

- You prefer fixed interest rates and structured repayments

- You have a good credit score that qualifies you for competitive loan terms.

Choose a Balance Transfer Credit Card If:

- You want to consolidate and pay off existing high-interest credit card debt.

- You can pay off the transferred balance within the promotional 0% APR period.

- You have good credit or are willing to work on improving your credit score.

Read more: Step-by-step guide for a successful credit card balance transfer

Ultimately, the decision should align with your financial goals and ability to manage and repay the debt responsibly. Be sure to compare offers from multiple lenders or credit card issuers to secure the best terms and save on interest or fees. Managing your finances wisely can lead to better financial stability and long-term success.

Join Our Thriving Community of Smart Savers – Become a Part of Our Growing Network and Harness the Power of Bright Money. Sign Up Today and Start Transforming Your Financial Future!

References:

- https://www.forbes.com/advisor/personal-loans/how-do-personal-loans-work/

- https://www.investopedia.com/credit-cards/balance-transfer-credit-card/

- https://www.investopedia.com/balance-transfer-vs-personal-loan-7501421

FAQs

1. What is the typical interest rate for a personal loan?

The interest rate for a personal loan can vary widely depending on factors such as your credit score, the lender's policies, and prevailing market conditions. On average, personal loan interest rates range from 6% to 36%.

2. Can I use a personal loan to repay credit card debt?

You can use a personal loan to consolidate and pay off credit card debt. Many people choose this option to take advantage of potentially lower interest rates and structured repayments.

3. How do I qualify for a balance transfer credit card with a 0% APR offer?

Qualifying for a balance transfer credit card with a 0% APR offer typically requires a good to excellent credit score. Lenders may also consider your income and credit history when making their decision.

4. Are there any downsides to using balance transfer credit cards?

Yes, there are downsides to using balance transfer credit cards. One significant drawback is the limited duration of the introductory 0% APR period. You may face high interest charges if you don't pay off the transferred balance within that time. Additionally, balance transfer fees can add to the overall cost.

5. Can I use a balance transfer credit card for purposes other than consolidating debt?

Balance transfer credit cards are primarily designed for consolidating and paying off existing credit card debt. While you may be able to use the card for other purchases, it's essential to focus on paying down the transferred balance during the promotional period to maximize the benefits of the 0% APR offer.