You are now leaving the Bright website and entering a third-party website. Bright has no control over the content, products, or services offered, nor the security or privacy of information transmitted to others via their website. We recommend that you review the privacy policy of the site you are entering. Bright does not guarantee or endorse the products, information, or recommendations provided on any third-party website.

Imagine you're on a quest to make smart financial decisions in a world full of options. You have a specific money goal in mind, like paying off debt, fixing up your home, or handling unexpected medical bills. But how do you pick the right tool for the job?

Well, it's kind of like choosing between two handy gadgets: a personal loan and a line of credit. They both help you out financially, but they work a bit differently. Let's break it down in a way that's easy to understand.

Think of personal loans as getting a lump sum of money from a friendly lender. You know exactly how much you're getting and how long it'll take to pay it back. It's like borrowing your buddy's lawnmower for a weekend – clear terms and a fixed arrangement.

Now, picture a line of credit as a financial safety net. It's like having a friend who lets you borrow money whenever you need it, up to a certain limit. You can take a little here and there, and you only pay interest on what you use. It's flexible, like borrowing your neighbor's tools whenever a home project pops up.

In our journey, we'll explore these two money helpers in detail. We'll see when personal loans shine and when Line of Credit steal the spotlight. By the end, you'll have the knowledge to make a wise financial choice, just like picking the right tool for any job. So, let's dive into the world of personal finance and discover which option works best for you.

Read more: Personal loan vs. Credit Card: What's better?

Personal Loans or Lines of Credit: Which is the Better Financial Option for You?

Personal loans provide a fixed sum of money upfront, repaid in installments, often ideal for specific, one-time expenses. Lines of credit offer a flexible borrowing arrangement, where you can access funds up to a predetermined limit as needed, with interest on the amount used.

Personal loans offer predictability, while lines of credit offer convenience. Your choice depends on your financial goals and preferences: the certainty of a personal loan or the flexibility of a line of credit. Understanding these distinctions empowers you to make the right financial decision tailored to your unique circumstances.

Understanding Personal Loans

Online lenders, credit unions, and banks all provide personal loans as a financial service. They are often unsecured, which implies that no property, such as a house or car, is needed as security for the loan. Personal loans give borrowers access to a lump sum of cash that they can use for a range of things, such as debt relief, home renovations, medical costs, and more. Here are some essential details about personal loans:

- Fixed Loan Amount: Personal loans provide borrowers with a predetermined amount of money, which is agreed upon at the time of loan approval. This amount is typically dispersed in one lump sum

- Fixed Interest Rate: Personal loans often come with a fixed interest rate, which means that the interest rate remains constant throughout the life of the loan. This makes it easier for borrowers to budget because they know exactly how much they must repay each month

- Fixed Repayment Term: Personal loans have a fixed repayment term, which is usually between 1 and 5 years. Borrowers make equal monthly payments until the loan is paid off in full

- Credit Check: Lenders typically require a credit check when applying for a personal loan. A good credit score can help secure a lower interest rate and better loan terms

- Purpose: Personal loans can be used for a wide range of purposes, from funding a vacation to covering unexpected medical expenses[1]

Join Bright Money Today and Take Control of Your Finances!

The Benefits of Personal Loans

Now that we have a basic understanding of personal loans let's explore some of the benefits they offer to borrowers:

- Predictable Payments: Personal loans come with fixed monthly payments, making it easier for borrowers to budget and plan their finances. This predictability can be particularly advantageous when consolidating high-interest debt

- No Collateral Required: Since personal loans are typically unsecured, borrowers don't need to put up assets like their home or car as collateral. This means that the lender cannot seize their property in the event of default

- Various Loan Amounts: Personal loans come in various loan amounts, so borrowers can choose an amount that suits their specific needs, whether it's a small loan for a minor expense or a larger loan for a major project

- Competitive Interest Rates: With a good credit score, borrowers can qualify for competitive interest rates on personal loans, making them an affordable option for borrowing

- Quick Approval: Many lenders offer fast approval and funding for personal loans, allowing borrowers to access funds relatively quickly, often within a few days[2]

Understanding Lines of Credit

A line of credit (LOC) is another form of borrowing that differs from a personal loan in several ways. Instead of providing a lump sum of money upfront, a line of credit offers borrowers a revolving credit limit, similar to a credit card. Borrowers can draw funds from this credit line as needed, up to the maximum limit, and interest is only charged on the amount borrowed. Here are some key characteristics of lines of credit:

- Revolving Credit: A line of credit is a revolving form of credit, meaning that as you repay the borrowed amount, the credit becomes available again, much like a credit card

- Variable Interest Rate: Lines of credit often come with variable interest rates, which means that the interest rate can change over time based on market conditions

- Flexible Repayment: Unlike personal loans with fixed monthly payments, lines of credit offer more flexibility in how you repay the borrowed funds. You can make minimum payments or pay off the balance in full, depending on your financial situation

- Access to Cash: Lines of credit provide access to cash when needed, making them suitable for covering ongoing expenses or managing financial emergencies

- Credit Check: Lenders typically require a credit check when applying for a line of credit. A strong credit history can help secure better terms and a higher credit limit[3]

Unlock Financial Freedom - Sign Up for Bright Money Now!

The Benefits of Lines of Credit

Now that we've covered the basics of lines of credit let's explore some of the advantages they offer to borrowers:

- Flexibility: Lines of credit are highly flexible, allowing borrowers to use funds as needed and only pay interest on the amount borrowed. This flexibility makes them ideal for unpredictable expenses or projects with varying costs

- Ongoing Access: With a line of credit, you have continuous access to funds as long as you stay within your credit limit. This can be useful for managing cash flow in a business or handling unexpected financial setbacks

- Variable Interest Rates: While variable interest rates can be a disadvantage in rising rate environments, they can also work in your favor when interest rates are low, potentially resulting in lower borrowing costs

- Lower Initial Costs: Since you only pay interest on the amount you borrow, the initial costs of opening a line of credit can be lower than those associated with a personal loan

- Credit Building: Responsible use of a line of credit can help build or improve your credit score over time, which can be beneficial for future borrowing[4]

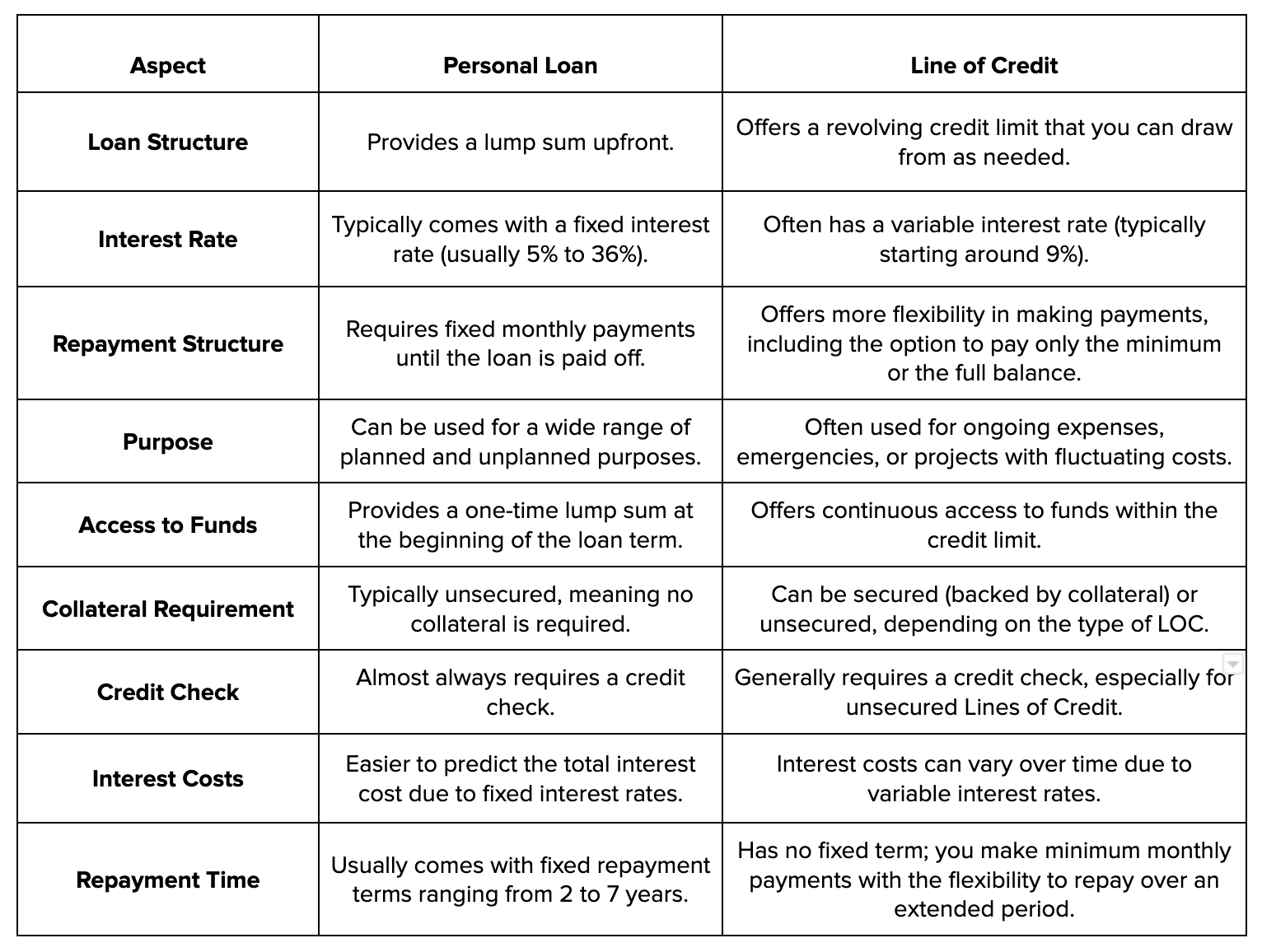

Differences Between Personal Loans and Lines of Credit

Now that we have a clear understanding of both personal loans and lines of credit, let's compare them side by side to highlight their key differences:

a) Loan Structure

- Personal Loan: Provides a lump sum of money upfront

- Line of Credit: Offers a revolving credit limit that you can draw from as needed

b) Interest Rate

Personal loan interest rates typically range from 5% to 36%, depending on your creditworthiness. Lines of credit often have variable rates, typically starting around 9% but can vary widely based on your financial profile.

- Personal Loan: Typically comes with a fixed interest rate

- Line of Credit: Often has a variable interest rate that can change over time

c) Repayment Structure

Personal loans usually offer fixed repayment terms ranging from 2 to 7 years. Lines of credit have no fixed term; you make minimum monthly payments with the flexibility to repay over an extended period or as quickly as you prefer.

- Personal Loan: Requires fixed monthly payments until the loan is paid off

- Line of Credit: Offers more flexibility in making payments, including the option to pay only the minimum or the full balance

d) Purpose

- Personal Loan: Can be used for a wide range of planned and unplanned purposes.

- Line of Credit: Often used for ongoing expenses, emergencies, or projects with fluctuating costs.

e) Access to Funds

- Personal Loan: Provides a one-time lump sum at the beginning of the loan term

- Line of Credit: Offers continuous access to funds within the credit limit

f) Collateral Requirement

- Personal Loan: Typically unsecured, meaning no collateral is required

- Line of Credit: This can be secured (backed by collateral) or unsecured, depending on the type of LOC

g) Credit Check

- Personal Loan: Almost always requires a credit check

- Line of Credit: Generally requires a credit check, especially for unsecured lines of credit

h) Interest Costs

- Personal Loan: It is easier to predict the total interest cost due to fixed interest rates

- Line of Credit: Interest costs can vary over time due to variable interest rates[5]

Certainly, here's a table summarizing the differences between personal loans and lines of credit:

Don't Miss Out on Smarter Money Management - Get Started with Bright Money!

When to Choose a Personal Loan?

Now that we've highlighted the differences between personal loans and lines of credit let's discuss when it makes sense to choose a personal loan:

- Fixed Expense: If you have a specific, one-time expense in mind, such as purchasing a car or financing a home improvement project, a personal loan with a fixed amount and interest rate may be more suitable

- Predictable Budgeting: Personal loans offer fixed monthly payments, making it easier to budget and plan for the repayment of your loan

- Debt Consolidation: If you have high-interest debts that you want to consolidate into a single, lower-interest loan, a personal loan can be an effective tool for debt consolidation

- Short-Term Financing: Personal loans typically have shorter loan terms, which can make them suitable for borrowers looking to repay the debt relatively quickly

- Good Credit: A personal loan may offer cost-effective borrowing if you have a strong credit history and can qualify for a competitive interest rate[6]

When to Choose a Line of Credit?

Now, let's explore situations where choosing a line of credit is more advantageous:

- Ongoing Expenses: Lines of credit are ideal for managing ongoing expenses, such as running a small business or dealing with unpredictable medical bills

- Emergency Fund: A line of credit can serve as a financial safety net for unexpected emergencies, providing quick access to funds without the need to apply for a new loan

- Fluctuating Costs: If you're working on a project with fluctuating costs, like a home renovation, a line of credit can provide flexibility in funding as needed

- Variable Interest Rates: In a low-interest-rate environment, a line of credit with a variable interest rate may offer lower borrowing costs than a fixed-rate personal loan

- Building Credit: Responsible use of a line of credit can help improve your credit score over time, which can be beneficial for future borrowing[7]

Join Thousands of Satisfied Users - Sign Up with Bright Money Today!

How to Apply for a Personal Loan or a Line of Credit?

Whether you decide to apply for a personal loan or a line of credit, the application process generally involves the following steps:

- Check Your Credit: Review your credit report and credit score to get an idea of your creditworthiness. A higher credit score can improve your chances of approval and better terms

- Choose a Lender: Research different lenders, including banks, credit unions, and online lenders, to find one that offers competitive rates and terms

- Gather Required Documents: Lenders typically require documentation such as proof of income, identification, and bank statements. Be prepared to provide these documents when applying

- Fill Out the Application: Complete the lender's application form, providing accurate and up-to-date information about yourself and your financial situation

- Await Approval: The lender will review your application and credit history to determine whether to approve your request for a personal loan or line of credit

- Review the Terms: If approved, carefully review the terms and conditions of the loan or line of credit, including the interest rate, repayment schedule, and any fees

- Accept the Offer: If you're satisfied with the terms, accept the lender's offer by signing the loan agreement or line of credit agreement

- Receive Funds: Once you've accepted the offer, the lender will disburse the funds to your bank account or, in the case of a line of credit, make the credit available for your use[8]

Read more: Personal Loans: Everything You Need to Know.

Conclusion

Personal loans and lines of credit are valuable financial tools that can help individuals meet their various financial needs. While personal loans offer a lump sum with fixed terms and predictable payments, lines of credit provide flexibility and ongoing access to funds. Your choice between the two depends on your specific financial situation, goals, and preferences.

Before applying for either option, it's essential to carefully evaluate your needs and compare the terms offered by different lenders. Also, maintaining responsible borrowing habits and managing your debt wisely will help you make the most of a personal loan or a line of credit while maintaining your financial well-being.

Ultimately, the key to successful borrowing is understanding the nuances of personal loans and lines of credit and selecting the one that aligns best with your financial goals and lifestyle. By making informed decisions and managing your debt responsibly, you can use these financial tools to your advantage and confidently achieve your financial objectives.

Experience Stress-Free Finances - Register for Bright Money Now!

References:

- https://www.forbes.com/advisor/personal-loans/how-do-personal-loans-work/

- https://www.bajajfinserv.in/what-are-personal-loan-benefits

- https://www.investopedia.com/terms/l/lineofcredit.asp

- https://www.cibc.com/en/personal-banking/smart-advice/borrowing-and-credit/line-of-credit-advantages.html#:~:text=Here%20are%20some%20benefits%20to,pay%20back%20a%20large%20purchase

- https://www.bajajfinserv.in/difference-between-personal-loan-and-line-of-credit

- https://www.investopedia.com/articles/personal-finance/111715/when-are-personal-loans-good-idea.asp#:~:text=Some%20reasons%20for%20choosing%20a,your%20least%20expensive%20borrowing%20option.

- https://www.investopedia.com/articles/personal-finance/072913/basics-lines-credit.asp#:~:text=However%2C%20if%20you%20don't,up%20to%20that%20limit%20again

- https://www.investopedia.com/articles/personal-finance/010516/how-apply-personal-loan.asp

FAQs

1. What Are the Common Uses of Personal Loans?

Personal loans are versatile and can be used for various purposes, such as consolidating high-interest debt, financing home improvements, covering medical expenses, funding a wedding, or even taking a dream vacation. The flexibility of personal loans makes them a popular choice for borrowers with diverse financial goals.

2. How Can I Qualify for a Competitive Interest Rate on a Personal Loan?

To secure a competitive interest rate on a personal loan, it's crucial to maintain a good credit score, demonstrate a stable income, and have a low debt-to-income ratio. Lenders typically offer better rates to borrowers with strong creditworthiness.

3. What Is the Difference Between a Secured and Unsecured Line of Credit?

A secured line of credit requires collateral, such as a home or car, to secure the credit limit. In contrast, an unsecured line of credit does not require collateral but may have higher interest rates and stricter credit requirements. Choosing between the two depends on your risk tolerance and available assets.

4. Can I Access My Line of Credit via a Credit Card or Cheques?

Many lines of credit offer convenient access options, such as credit cards or cheques linked to the credit line. These tools allow you to use your line of credit for everyday expenses or specific purchases, making it more versatile.

5. How Does a Line of Credit Affect My Credit Score?

Properly managed lines of credit can positively impact your credit score by demonstrating responsible borrowing behavior. Paying on time and maintaining a low credit utilization rate can boost your creditworthiness. However, late payments or maxing out your credit limit can have a negative effect on your credit score.