You are now leaving the Bright website and entering a third-party website. Bright has no control over the content, products, or services offered, nor the security or privacy of information transmitted to others via their website. We recommend that you review the privacy policy of the site you are entering. Bright does not guarantee or endorse the products, information, or recommendations provided on any third-party website.

Do you ever feel like you're trapped in a never-ending cycle of credit card debt? Does the weight of high interest rates and mounting balances keep you awake at night? You're not alone. In fact, a staggering 47% of American households carry credit card debt, with the average balance per household reaching $5,315, according to the Federal Reserve's most recent data.

High interest rates, minimum monthly payments, and the seemingly insurmountable challenge of escaping the clutches of credit card debt can take a severe toll on your financial well-being. But fear not; a strategic and potentially life-changing solution is at your disposal.

Imagine a scenario where you could not only break free from the suffocating grip of credit card debt but also do so with lower interest rates, predictable monthly payments, and a clear path to financial freedom. It is not a fantasy; it is the power of using a personal loan to pay off your credit card debt.

In this thorough tutorial, we'll take a trip through the world of personal finance and examine the advantages and disadvantages of using a personal loan to pay off credit card debt. We'll arm you with the information and resources you need to decide for yourself whether this financial strategy is the best fit for your particular set of circumstances.

Join us as we delve into the art of financial liberation, where wise choices can lead to a brighter, debt-free future.

Read more: 3 reasons to use personal loans to pay off debt

Understanding Credit Card Debt

Before delving into the specifics of using a personal loan to pay off credit card debt, it is crucial to grasp the nature of credit card debt itself. Credit card debt is unsecured debt, meaning it is not backed by collateral like a mortgage or auto loan. As a result, credit card companies charge higher interest rates compared to secured loans, making it one of the most expensive forms of borrowing.

1. The High Costs of Credit Card Debt

The primary reason credit card debt is so burdensome is the high Annual Percentage Rate (APR). Credit card APRs can easily exceed 20% or even 30%, depending on the cardholder's creditworthiness. This high interest accrues monthly on the outstanding balance, substantially increasing the overall cost of the debt.

2. Minimum Payments and Debt Snowballing

Credit card companies typically require cardholders to make minimum monthly payments, usually calculated as a percentage of the outstanding balance or a fixed amount, whichever is greater. While this might seem like a manageable approach, it can lead to a dangerous cycle of debt.

Paying only the minimum amount due can result in the debt snowball effect. As the interest continues to accumulate, it becomes increasingly challenging to pay off the principal balance, and the debt grows larger over time.

3. Impact on Credit Score

Carrying a high credit card balance relative to your credit limit, known as a high credit utilization rate, can negatively impact your credit score. A lower credit score can affect your ability to secure favorable loan terms, rent an apartment, or obtain competitive insurance rates.[1]

Start Your Journey to Financial Freedom Today! - Click here to sign up for Bright Money and take control of your finances.

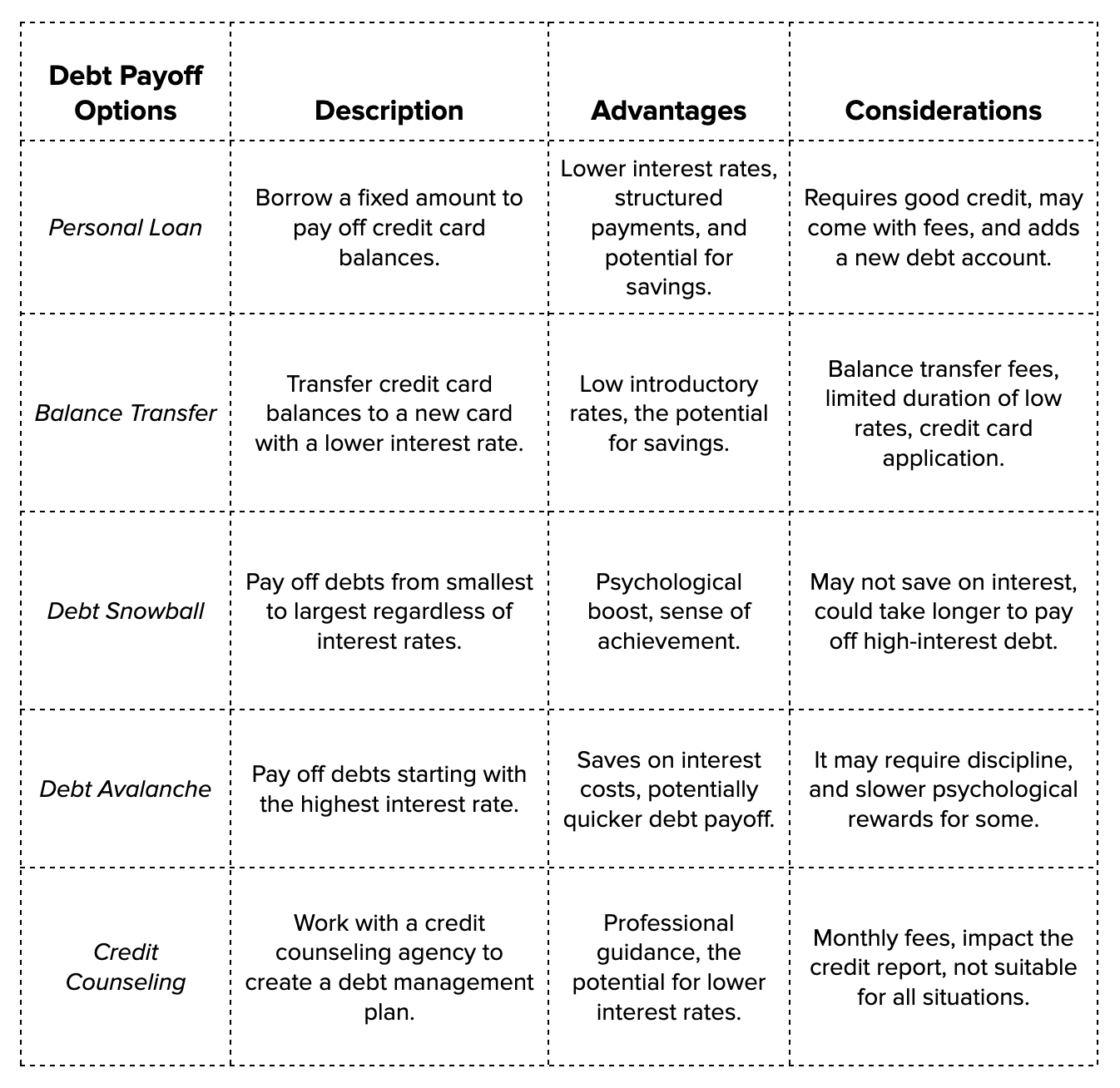

Options to pay Credit Card Debt

When it comes to paying off credit card debt, individuals have several options to consider. Let's compare these options in a table to highlight their key features:

Debt Consolidation with Personal Loan

Debt consolidation is a popular strategy for managing credit card debt. It involves taking out a personal loan to pay off multiple credit card balances, essentially consolidating them into a single loan account. This approach can be highly effective for several reasons:

- Lower Interest Rates: Personal loans typically offer lower interest rates compared to credit cards, which can result in reduced overall interest costs

- Structured Payments: Personal loans come with fixed monthly payments and a set repayment term, making it easier to budget and plan for debt elimination

- Potential for Savings: By securing a personal loan with a lower interest rate, you can potentially save money over time while paying off your debt

However, debt consolidation with a personal loan requires good credit to qualify for favorable interest rates. It's important to be aware of any fees associated with the loan and ensure that you don't continue to accumulate new credit card debt after consolidating.

If you're considering debt consolidation with a personal loan, take the first step toward financial freedom with Bright Money. Optimize your debt repayment strategy, build credit the smart way, and AI budget management. Get started today!

Personal Loans as a Solution

Personal loans offer an alternative means of borrowing money to pay off credit card debt. Unlike credit cards, personal loans typically have lower interest rates, fixed monthly payments, and structured repayment terms. Here's why they can be a viable solution:

1. Lower Interest Rates

One of the most significant advantages of using a personal loan to pay off credit card debt is the potential for lower interest rates. Personal loans are often available with fixed interest rates, which are considerably lower than the variable rates associated with credit cards.

2. Fixed Monthly Payments

Personal loans come with fixed monthly payments, allowing borrowers to create a budget and plan for debt repayment with confidence. This predictability can help individuals regain control of their finances.

3. Structured Repayment Terms

Personal loans typically have structured repayment terms, which means borrowers know exactly when they will be debt-free. This can provide a sense of accomplishment and motivation to stay on track with repayment.

4. Consolidation of Multiple Debts

If you have multiple credit card balances, a personal loan can simplify your finances by consolidating these debts into a single, manageable payment. This streamlining can reduce the risk of missing payments or incurring additional fees.[2]

Unlock a Brighter Future! - Join Bright Money now to access personalized financial guidance and improve your financial well-being.

Steps to Using a Personal Loan for Credit Card Debt

Now that we understand the advantages of using a personal loan to pay off credit card debt, let us explore the steps involved in this process.

- Assess Your Financial Situation: Start by evaluating your current financial status. Calculate your total credit card debt, noting the APR and minimum monthly payments for each card. Check your credit score to gauge your eligibility for a competitive consolidation loan

- Research Lenders: Explore reputable lenders that offer debt payoff or consolidation loans. Consider factors like interest rates, loan terms, fees, and customer feedback. Popular lenders like LendingClub and SoFi often provide competitive options

- Apply for a Loan: Begin the loan application process with your chosen lender. Provide personal and financial information and consent to a credit check. Be ready to submit documentation like pay stubs, bank statements, and proof of identity

- Compare Loan Offers: Once you receive loan offers from different lenders, carefully compare them. Focus on interest rates, loan terms, monthly payments, and any associated fees. Select the offer that aligns best with your financial goals

- Use the Loan to Pay Off Debt: Upon securing your consolidation loan, use the funds to pay off your credit card debt in full. By doing this, you close your credit card accounts, preventing further charges and additional debt accumulation

- Create a Repayment Plan: Develop a structured repayment plan for your consolidation loan. Incorporate the monthly loan payments into your budget, ensuring they are manageable. Timely payments are crucial to avoid late fees and protect your credit score

- Monitor Your Progress: Keep a close eye on your debt reduction progress as you pay down your consolidation loan. Celebrate milestones, such as paying off a specific percentage of the loan, to stay motivated and committed to becoming debt-free

By following these steps and utilizing a consolidation loan, you can efficiently manage your credit card debt and work toward financial stability.[3]

Don't Wait – Secure Your Financial Peace! - Sign up with Bright Money and pave the way for a stress-free financial future.

Advantages of Using a Personal Loan for Credit Card Debt

Using a personal loan to consolidate and pay off credit card debt can offer several significant advantages for borrowers seeking financial relief and a more manageable path to debt repayment.

One of the primary advantages is the potential for significantly lower interest rates. Credit cards often come with high annual percentage rates (APRs), leading to exorbitant interest charges, especially when carrying a balance from month to month. In contrast, personal loans typically offer lower interest rates, particularly if you have a good credit score. This can result in substantial savings on interest payments, making your debt more affordable over time.

Another advantage is the structure of personal loans, which come with a fixed repayment schedule. With credit cards, it's easy to fall into the minimum payment trap, where you make only the minimum required payment each month, and a significant portion goes toward interest, prolonging the debt. Personal loans, however, have fixed monthly payments and set loan terms, helping you create a clear and structured plan for debt elimination. This predictability can make it easier to budget and stay on track with your payments.

Additionally, using a personal loan for credit card debt consolidation can simplify your financial life. Instead of juggling multiple credit card bills with varying due dates and interest rates, you'll have just one loan payment to manage each month. This streamlined approach can reduce the risk of missed payments and late fees, helping you regain control over your finances.[4]

Join Thousands of Satisfied Users! - Experience the transformative power of Bright Money – sign up now!

Risks and Considerations

Consolidating credit card debt with a personal loan can offer advantages, but it's essential to consider the potential risks and factors before proceeding.

One significant risk is the temptation to accumulate more credit card debt once your cards are paid off. Without addressing the root causes of your debt accumulation, you might find yourself in a cycle of borrowing that could worsen your financial situation. To mitigate this risk, it's crucial to create a budget and financial plan that helps you manage your spending and avoid falling back into debt.

Additionally, personal loans come with specific terms and conditions, including interest rates and fees. If you don't secure a personal loan with a lower interest rate than your credit cards, you might not experience significant financial benefits. It's essential to compare the interest rates and terms offered by different lenders carefully.

Lastly, some personal loans may come with origination fees or prepayment penalties. Be sure to read the loan agreement carefully to understand any additional costs associated with the loan.[5]

Tips for Maximizing the Effectiveness

Consolidating credit card debt with a personal loan can be a smart financial move, but it requires careful planning and discipline. Start by choosing the right loan with favorable terms, such as a lower interest rate than your credit cards. Compare offers from various lenders to find the most cost-effective option.

Once you have the loan, create a clear repayment plan that fits your budget. Calculate your monthly expenses and ensure that you can comfortably make loan payments without straining your finances. Stick to this plan to avoid accumulating more debt.

While repaying the personal loan, refrain from making new charges on your credit cards. Using your cards for additional purchases can undermine your efforts to reduce debt. Focus on paying down the existing balances and avoid taking on more financial obligations.

Make it a priority to make timely payments on your personal loan. Consistent, on-time payments not only keep you on track but also positively impact your credit score. Late or missed payments can harm your credit history, making it harder to secure favorable financial terms in the future.[6]

Read more: The best day to pay your credit cards

Conclusion

If you have high-interest credit card balances, using a debt consolidation or credit card refinance to pay off credit card debt can be a wise financial move. Lower interest rates, regular monthly payments, structured payback schedules, and the possibility of debt consolidation are some of the benefits. However, you must carefully assess the dangers and the potential effects on your credit score.

Take measures to raise your credit score, look around for the best loan deals, make a budget, and refrain from taking on additional credit card debt to get the most out of this strategy. Using a personal loan to pay off credit card debt can be a key step toward reaching financial freedom and peace of mind with cautious preparation and sound money management.

Ready to Thrive Financially? Let's Begin! - Start your Bright Money journey today and make smarter financial decisions.

References:

- https://www.investopedia.com/terms/c/credit-card-debt.asp#:~:text=Credit%20card%20debt%20is%20a,and%20tracked%20by%20credit%20bureaus.

- https://www.forbes.com/advisor/personal-loans/personal-loan-to-pay-off-credit-card/

- https://www.cnbc.com/select/using-a-personal-loan-to-pay-off-credit-card-debt/

- https://poonawallafincorp.com/blogs/benefit-of-using-personal-loan-to-pay-credit-card-debt.php

- https://www.bankrate.com/finance/credit-cards/take-out-personal-loan-to-pay-credit-card-bill/

- https://m.economictimes.com/wealth/borrow/seven-smart-ways-to-reduce-loan-burden-without-stressing-your-wallet/articleshow/45502314.cms

FAQs

Q. What are the qualifications for obtaining a personal loan to pay off credit card debt?

To qualify for a personal loan to pay off credit card debt, you typically need a good credit score, which is generally considered to be 660 or higher. Lenders also consider factors like your income, employment history, and debt-to-income ratio. A stable source of income is essential to demonstrate your ability to repay the loan. Keep in mind that qualification requirements may vary among lenders, so it is a good idea to shop around and compare offers.

Q. How does using a personal loan affect my credit score?

Initially, taking out a personal loan may result in a small dip in your credit score due to the hard credit inquiry made by the lender. However, as you use the loan to pay off credit card debt and make consistent, on-time payments, your credit score can improve over time. Reducing your credit card balances and closing some accounts can also positively impact your credit utilization rate, which is another factor that influences your credit score.

Q. Are there alternatives to using a personal loan to pay off credit card debt?

Yes, several alternatives exist, including balance transfer credit cards, debt consolidation programs, and negotiating directly with creditors for lower interest rates or repayment plans. Each option has its pros and cons, so evaluating which option aligns the best with your financial goals is important.

Q. What should I do after paying off credit card debt with a personal loan?

After successfully paying off your credit card debt with a personal loan, avoid accumulating new credit card balances. Maintain responsible credit card usage by paying your full balance each month and only using credit for necessary expenses. Continue to budget effectively and consider saving or investing the money you were previously allocated to credit card payments.

Q. Can I pay off the personal loan early without penalties?

The ability to pay off a personal loan early without penalties depends on the terms of the loan agreement. Some lenders allow early repayment without additional charges, while others may impose prepayment penalties. Before signing the loan agreement, understand clauses regarding early repayment to finalize your repayment strategy.