You are now leaving the Bright website and entering a third-party website. Bright has no control over the content, products, or services offered, nor the security or privacy of information transmitted to others via their website. We recommend that you review the privacy policy of the site you are entering. Bright does not guarantee or endorse the products, information, or recommendations provided on any third-party website.

Ever wondered why so many Americans struggle financially, living paycheck to paycheck? The numbers are staggering – a whopping 78% of U.S. workers find it tough to make their money last. That's a real eye-opener, highlighting the need for better money management.

In this article, we're tackling a big question: When facing a financial challenge, should you go for a personal or payday loan? Your decision can make or break your financial well-being.

Think about this: Nearly 70% of Americans admit they're stressed about money, and 64% worry they don't have enough savings for unexpected expenses. These stats show we need accessible and responsible financial options that won't bury us in debt.

So, let's go on a journey to understand personal loans and payday loans – how they work, who can get them, the interest rates involved, and the consequences of your choice. By the end, you'll have the knowledge to make a smart financial move that sets you on the path to a more secure future. Let's get started!

Read more: What is better: Personal loans or credit cards?

Should You Get a Personal Loan or a Payday Loan?

Choose a personal loan when you have a stable financial situation, need a larger amount, and can handle a longer repayment period. Opt for a payday loan only in extreme emergencies when you need a small amount of cash quickly, but be aware of the high fees and short repayment terms. Always prioritize responsible borrowing and consider your financial circumstances carefully before deciding.

Understanding Personal Loans

Personal loans are versatile financial tools that offer individuals access to a lump sum of money that can be used for a wide range of purposes. Unlike specific loans designed for a particular expense, such as a mortgage for a home or an auto loan for a car, personal loans provide flexibility. Borrowers can use them to consolidate high-interest debt, fund home improvements, cover medical bills, plan a dream vacation, or handle unexpected emergencies.

These loans typically come with fixed interest rates and fixed repayment terms, making it easier for borrowers to budget and plan for their financial obligations. Lenders evaluate an applicant's credit history, income, and other factors to determine eligibility and the interest rate offered. Personal loans are popular for those seeking a predictable and structured way to access funds for various financial needs. However, it's crucial for borrowers to understand the terms, interest rates, and fees associated with these loans to make informed decisions and manage their finances responsibly.[1]

Don't let financial stress hold you back. Join Bright Money now and get personalized financial guidance at your fingertips.

Understanding Payday Loans

Payday loans, often marketed as quick and convenient solutions for immediate cash needs, are short-term, high-cost loans that cater to individuals facing urgent financial constraints. These loans are typically characterized by their small loan amounts and extremely short repayment periods, usually due on the borrower's next payday, hence the name "payday loans." They are relatively easy to access, often requiring minimal documentation and no extensive credit checks. While this accessibility can be appealing for those in desperate situations, payday loans come with exorbitant interest rates and fees, which can trap borrowers in a cycle of debt.

One of the significant concerns surrounding payday loans is the high cost of borrowing. The annual percentage rates (APRs) on these loans can soar into the triple digits, making them one of the most expensive forms of borrowing available. Borrowers who cannot repay the loan in full by their next payday often roll it over, incurring additional fees and interest, leading to a cycle of debt that can be challenging to escape. Due to these risks, payday loans are heavily regulated in many jurisdictions, and it's crucial for borrowers to fully understand the terms and explore alternative financial options before considering a payday loan as a last resort.[2]

Start saving, investing, and living your best financial life with Bright Money. Sign up now and discover a brighter financial future.

Comparing Personal Loans and Payday Loans

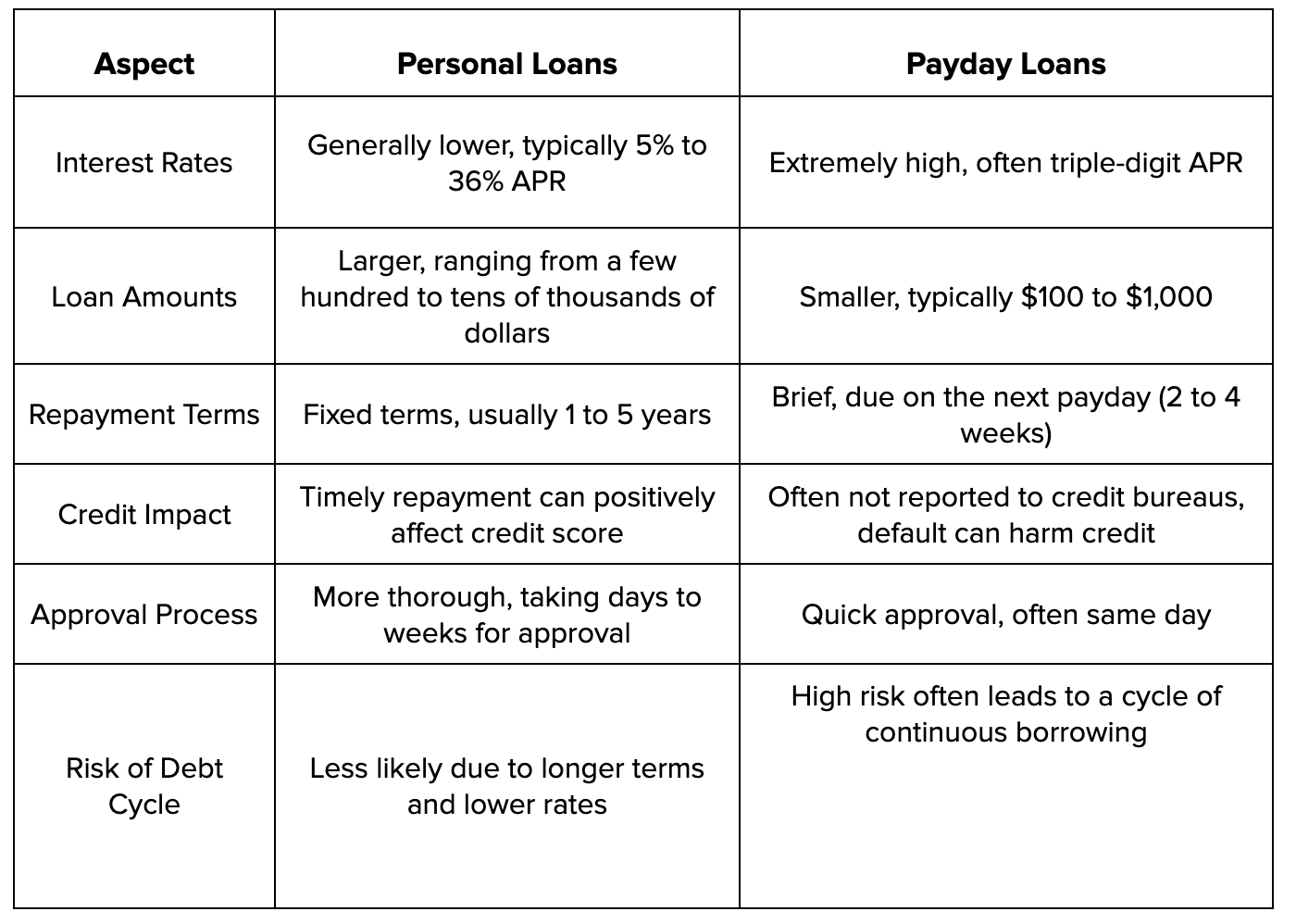

Here's a comparison table summarizing the key differences between personal loans and payday loans:

This table provides a clear overview of how personal loans and payday loans differ in terms of interest rates, loan amounts, repayment terms, credit impact, approval process, and the risk of falling into a debt cycle.[3]

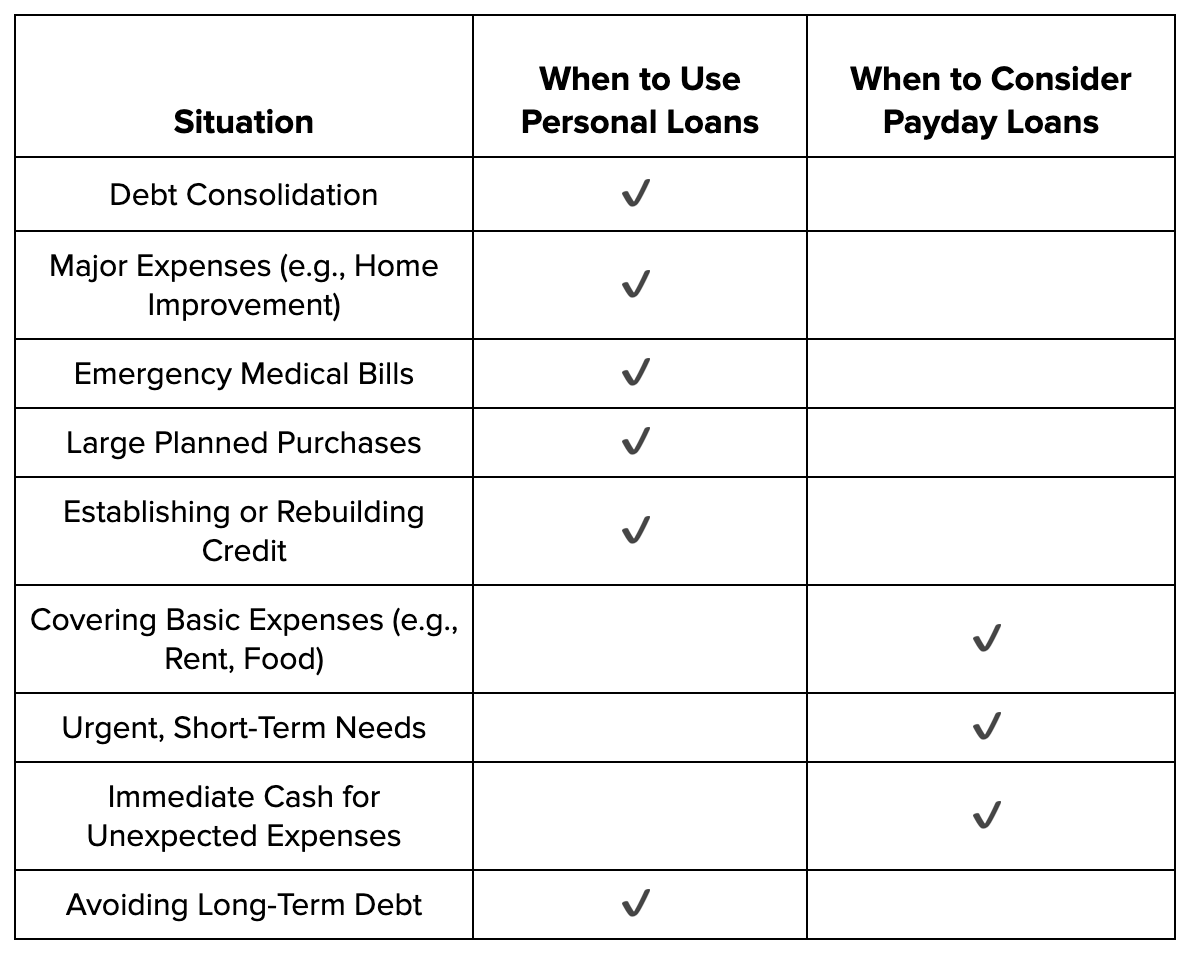

Here's a table summarizing when to use personal loans and when to consider payday loans:

This table helps you understand when it's appropriate to choose a personal loan over a payday loan and vice versa based on different financial situations. Personal loans generally suit larger, planned expenses and long-term financial goals. In contrast, payday loans may be considered for urgent, short-term needs when no other options are available. However, it's essential to exercise caution when considering payday loans due to their high costs and potential for debt cycles.[3]

Why wait to secure your financial future? Sign up for Bright Money and let us help you make smarter money decisions today.

Making an Informed Choice

Now that you have a clear understanding of the differences between personal loans and payday loans, it is important to make an informed choice based on your specific financial situation and needs. Here are some key considerations:

1. When to Choose a Personal Loan?

You may consider a personal loan when:

- You need a larger loan amount for a significant expense, such as home repairs or debt consolidation

- You have a good credit score, which can help you secure a lower interest rate

- You prefer a structured repayment plan with fixed monthly installments

- You want to improve your credit score by making timely payments[3]

2. When to Choose a Payday Loan?

You may consider a payday loan when:

- You are facing an emergency expense that needs immediate attention, such as a medical bill or car repair

- You have no other options for accessing funds, and your credit score is poor

- You are confident in your ability to repay the loan in full on your next payday

- You have explored other alternatives, such as borrowing from friends or family, and found them unsuitable or unavailable

3. Alternatives to Payday and Personal Loans

Before making a final decision, it is essential to explore other alternatives that may be more suitable for your situation:

- Emergency Savings: Building an emergency fund can provide a financial cushion for unexpected expenses, reducing the need for high-interest loans

- Credit Cards: If you have a credit card with available credit, it may be a less costly option than payday loans

- Borrowing from Friends or Family: Consider reaching out to loved ones for temporary financial assistance, if possible

- Community Assistance Programs: Some community organizations and nonprofits offer financial assistance programs for individuals in need

- Refinance Existing Loans: If you have existing loans with high interest rates, refinancing them to secure lower rates can help you save money on interest payments over time

- Credit Builder Loans: These loans are designed to help individuals establish or improve their credit scores. They work by depositing the loan amount into a savings account, and your credit score improves as you make on-time payments. Once the loan term ends, you can access the funds and an improved credit score[3]

Bright Money: Bright Money is a comprehensive financial wellness platform that provides personalized financial advice and strategies to help you manage your finances, pay off debt, and save money. It offers a holistic approach to improving your financial health.

Read more: 3 reasons to use personal loans to pay off debt

Conclusion

In the critical decision between a personal loan and a payday loan, it is paramount to evaluate each option's advantages and disadvantages carefully. With their lower interest rates and structured repayment terms, personal loans offer a more stable and financially responsible choice. On the other hand, payday loans provide swift access to cash, catering to individuals with poor credit, but they come with exorbitant costs and a potential spiral into debt.

Our expert advice is clear: Prioritize responsible borrowing and meticulous financial planning to attain long-term financial stability. Exhaust all other available alternatives before considering payday loans due to their high expenses and the risk of financial instability they entail. If you opt for a personal loan, be diligent in your search for the most favorable terms and interest rates. Your financial well-being hinges on making informed choices that align with your goals while minimizing unnecessary costs and risks.

Join thousands of satisfied users who have transformed their financial lives with Bright Money. Take the first step toward financial freedom – sign up now!

References:

- https://www.forbes.com/advisor/personal-loans/how-do-personal-loans-work/

- https://www.lendingtree.com/personal/understanding-payday-loans/#:~:text=A%20payday%20loan%20is%20a

- https://www.investopedia.com/payday-loans-vs-personal-loans-5214282

FAQs

- Are payday loans ever a good option for emergencies?

Payday loans can provide quick cash for emergencies, but they come with high costs. If you have no other options, and you're certain you can repay the loan on your next payday, they might help. However, they should be a last resort due to their exorbitant interest rates and the risk of falling into a cycle of debt.

- Can I get a personal loan with bad credit?

Yes, some lenders offer personal loans to individuals with bad credit, but the interest rates are typically higher. You may also need a co-signer or collateral to secure the loan. It is essential to compare offers and work on improving your credit score for better loan terms.

- What are the potential consequences of defaulting on a payday loan?

Defaulting on a payday loan can lead to a cascade of problems, including additional fees, collection calls, and damage to your credit score. In extreme cases, lenders may take legal action. It is crucial to communicate with your lender if you're unable to repay and explore alternatives to avoid these consequences.

- How can I break the cycle of payday loan debt?

Breaking the payday loan debt cycle requires careful financial planning. Start by creating a budget, reducing expenses, and exploring alternative sources of income. Seek help from credit counseling agencies or financial advisors who can provide guidance on managing debt and finding a way out of the cycle.

- Are there government regulations in place to protect payday loan borrowers?

Regulations regarding payday loans vary by country and state. Some governments have imposed restrictions on interest rates and loan terms to protect borrowers from predatory lending practices. It is essential to research your local regulations and ensure that the lender you choose complies with them to safeguard your financial interests