You are now leaving the Bright website and entering a third-party website. Bright has no control over the content, products, or services offered, nor the security or privacy of information transmitted to others via their website. We recommend that you review the privacy policy of the site you are entering. Bright does not guarantee or endorse the products, information, or recommendations provided on any third-party website.

Loans and other forms of credit lines have become an indispensable part of financial planning. Such planning is crucial for debt financing and fulfilling your aspirations and monetary needs. Financial institutions give individuals loans for different purposes, such as pursuing higher education, buying a house, launching a business, buying a car, etc. It is estimated that about 29 percent of undergraduate students and 66 percent of graduate students borrow federal loans to support their educational expenses.

However, banks don't approve loans to just everyone. As a borrower, you need to prove your creditworthiness to the banks. Creditworthiness means your ability to pay back the loans on time. There are several metrics that banks use to measure a borrower's creditworthiness. Some of the commonly used metrics to assess creditworthiness are debt-to-income ratio, credit score, etc.

This blog post will cover the debt-to-income ratio calculation, the importance of the debt-to-income ratio, and some key strategies to help you maintain an adequate debt-to-income ratio.

Read more: What's a good credit score?

What is the Debt to Income Ratio?

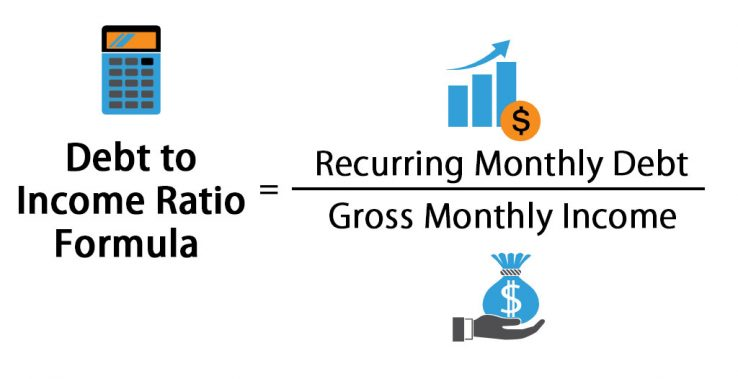

Debt to Income ratio is an essential metric that indicates your overall financial health. According to Investopedia, the Debt to Income ratio can be defined as the percentage of your gross monthly earnings utilized to meet your total monthly debt payments. For instance, if your debt-to-income ratio is 20%, then 20% of your gross monthly salary is used to repay existing loans. This metric is commonly used by financial institutions to assess the risks associated with loan repayment capabilities. [1]

A high debt-to-income ratio indicates that a high proportion of your salary goes into debt repayments, making it difficult for you to get additional loans. A low debt-to-income ratio signifies adequate earnings relative to debt repayments and makes it easier to get loans. Next, let's learn how to calculate your debt-to-income ratio.

How to Calculate the Debt to Income Ratio?

Here is what you need to do to calculate the debt-to-income ratio:

Step 1: First, you need to calculate your total monthly bills and payments. This should include all monthly recurring expenses such as house rent or mortgage payments, student loan payments, monthly alimony payments, child support payments, credit card debt, and any other types of debts incurred. It is important to note that debt to income ratio calculation does not include daily expenses such as gas, groceries, utilities, etc. [5]

Step 2: The next step is to divide the total monthly debt payments by your gross monthly earnings.[5]

(Note: Gross monthly income means your total earnings before taxes or any other deductions)

Step 3: The resulting number is your debt-to-income ratio. You can convert it into the percentage format by multiplying it by 100.[5]

Debt to Income Ratio = Total Monthly Debt Payments / Gross Monthly Income [3]

For instance, suppose Mr. X is trying to calculate his debt-to-income ratio. Here are the details of Mr. X's monthly income and bills.

- Gross monthly salary: $7,000

- Earning by renting out property: $5,000

- Credit card debt: $1,000

- Home mortgage payments: $1,500

- Auto loan payments: $500

Mr. X’s total monthly debt payment = ( $1,000 +$1,500 + $500 ) = $3,000

Mr. X’s gross monthly earnings = ( $7,000 + $5,000 ) = $12,000

Hence, Mr. X's debt-to-income ratio can be calculated as below:

Debt to Income ratio = ( $3,000 / $12,000 ) = 0.25

Therefore, Mr. X will report a 25% debt-to-income ratio.

There are many online debt-to-income ratio calculators that you can use to calculate your debt-to-income ratio. All you need to do is feed in the data required by the online tool.

Improve your credit easily with Bright Money. Sign up now!

Importance of Debt to Income Ratio

We have already established that banks use the Debt to Income Ratio as one of the metrics to assess the risks associated with the borrower's ability to pay back the loans. But the advantages of this metric go far beyond just that. Here are some pointers that signify the importance of debt to income ratio:

- Assessment of financial health: The debt-to-income ratio can tell you about your financial well-being in general. It can help you to quantify the proportion of your income spent on debt repayment. A lower debt-to-income ratio is indicative of a healthier financial situation as compared to a higher debt-to-income ratio.

- Personal financial planning: This metric can act as a powerful tool in financial planning. It allows you to make data-driven decisions based on your existing financial situation and align them with your financial goals and aspirations.

- Debt management: This metric plays an important role in the debt management process. With the help of this metric, you can forecast the impact of borrowing additional loans or reorganizing existing debt. Furthermore, you can also make informed choices about refinance options, debt repayment structure, etc.

- Risk assessment in personal finance: You can also use the debt-to-income ratio to evaluate your exposure to financial risk. A high debt-to-income ratio suggests that a large portion of your income is used for debt repayments. This situation makes you more vulnerable to a financial downturn, especially in case of unexpected expenses.

What Constitutes an Excellent Debt to Income Ratio?

Now, we know that a low debt-to-income ratio makes a borrower's profile more attractive to financial institutions. But is there an exact number that makes you eligible to apply for loans? Unfortunately, no.

Each financial institution has its debt-to-income ratio threshold for loan eligibility. But here is a general idea for you to understand what is an excellent debt-to-income ratio:

- Equal to or lower than 35%: Your debt-to-income ratio is looking good. You will have adequate earnings left over after paying your loan installments. You are in a good financial condition to apply for additional loans if required. [4]

- Between 35% and 50%: Your debt-to-income ratio has some scope for improvement. This range signifies that you are managing your debt well but should improve your debt-to-income ratio. If your debt-to-income ratio falls in this range, banks may ask you to submit additional documents for loan approval.[4]

- Equal to or higher than 50%: At this range, more than half of your salary is spent on loan payments. You will have a limited number of borrowing options with such a high debt-to-income ratio.[4]

Tips to Keep Your Debt to Income Ratio in Check

If your debt-to-income ratio is at a higher level and you are looking to improve your debt to income ratio, here are some key strategies that you can put to use:

- Look into other sources of income: Additional sources of monthly earnings can have a positive impact on your debt-to-income ratio. You can try to get a second job, work extra hours, seek a pay raise, or improve your skills to pursue a higher-paying job.[2]

- Increase your payment of loan installments: Though this step might increase your debt-to-income ratio temporarily (given your earning remains constant), it will reduce your total debt in the long run and thus lower your debt-to-income ratio.[2]

- Be reasonable with spending your money: Try to cancel or postpone some of the expensive purchases. This will enable you to save more and pay a larger sum towards loan payments.[2]

- Debt consolidation: You can also opt to take a debt consolidation loan. This step is carried out to restructure multiple small debts into one single payment. This will simplify your debt payment structure and lower your debt-to-income ratio in the long term.[2]

Read more: Who has the best debt consolidation loans?

Conclusion

A good debt-to-income ratio is an important milestone in achieving financial freedom. A lower debt-to-income ratio means more money is available after paying back loan payments and is favorable for debt financing. Strive to increase your earnings or lower your existing debt to lower your debt-to-income ratio and move closer to a debt-free life.

Bright Money is revolutionizing the way individuals pay back debt and build credit. We leverage cutting-edge technology to curate personalized AI-driven repayment plans and help individuals to achieve a debt-free life. Bright Money makes use of bank-level security with 256-bit encryption for data security. Say goodbye to low credit scores and embrace a future of financial well-being with BrightMoney.

Delete Debt and Build Savings with Bright Money. Get App.

References

- https://www.investopedia.com/terms/d/dti.asp#toc-how-to-lower-a-debt-to-income-ratio

- https://www.investopedia.com/ask/answers/081214/whats-considered-be-good-debttoincome-dti-ratio.asp#toc-how-to-lower-your-debt-to-income-dti-ratio

- https://www.wellsfargo.com/goals-credit/smarter-credit/credit-101/debt-to-income-ratio/

- https://www.wellsfargo.com/goals-credit/smarter-credit/credit-101/debt-to-income-ratio/understanding-dti/

- https://www.idfcfirstbank.com/finfirst-blogs/personal-loan/what-is-debt-to-income-ratio-and-how-to-calculate-it

- https://www.paisabazaar.com/home-loan/debt-to-income-ratio/

- https://www.bajajfinserv.in/insights/what-is-the-debt-to-income-ratio-and-how-to-get-it-right

- https://www.creditmantri.com/article-what-is-debt-to-income-ratio-and-how-does-it-impact-your-home-loan-eligibility/

- https://www.self.inc/blog/8-startling-signs-you-have-too-much-debt