You are now leaving the Bright website and entering a third-party website. Bright has no control over the content, products, or services offered, nor the security or privacy of information transmitted to others via their website. We recommend that you review the privacy policy of the site you are entering. Bright does not guarantee or endorse the products, information, or recommendations provided on any third-party website.

In the vast and ever-evolving realm of finance, loans play a pivotal role in empowering individuals and businesses to fulfill their aspirations and navigate through life's myriad financial challenges. Among the array of borrowing options, secured loans emerge as a favored choice, hailed for their unique advantages for borrowers and lenders alike.

This article endeavors to unravel the intricacies of a secured loan, shedding light on its essence, mechanics, and profound importance in the dynamic landscape of finance.

From empowering individuals to realize homeownership dreams to fueling entrepreneurial pursuits, understanding secured loans is essential for making informed financial decisions that can shape a brighter, more secure future.

Join us as we delve into the world of secured loans and unlock the potential they hold.

Read more: Good debt vs. Bad debt: What's the difference?

What is a Secured Loan?

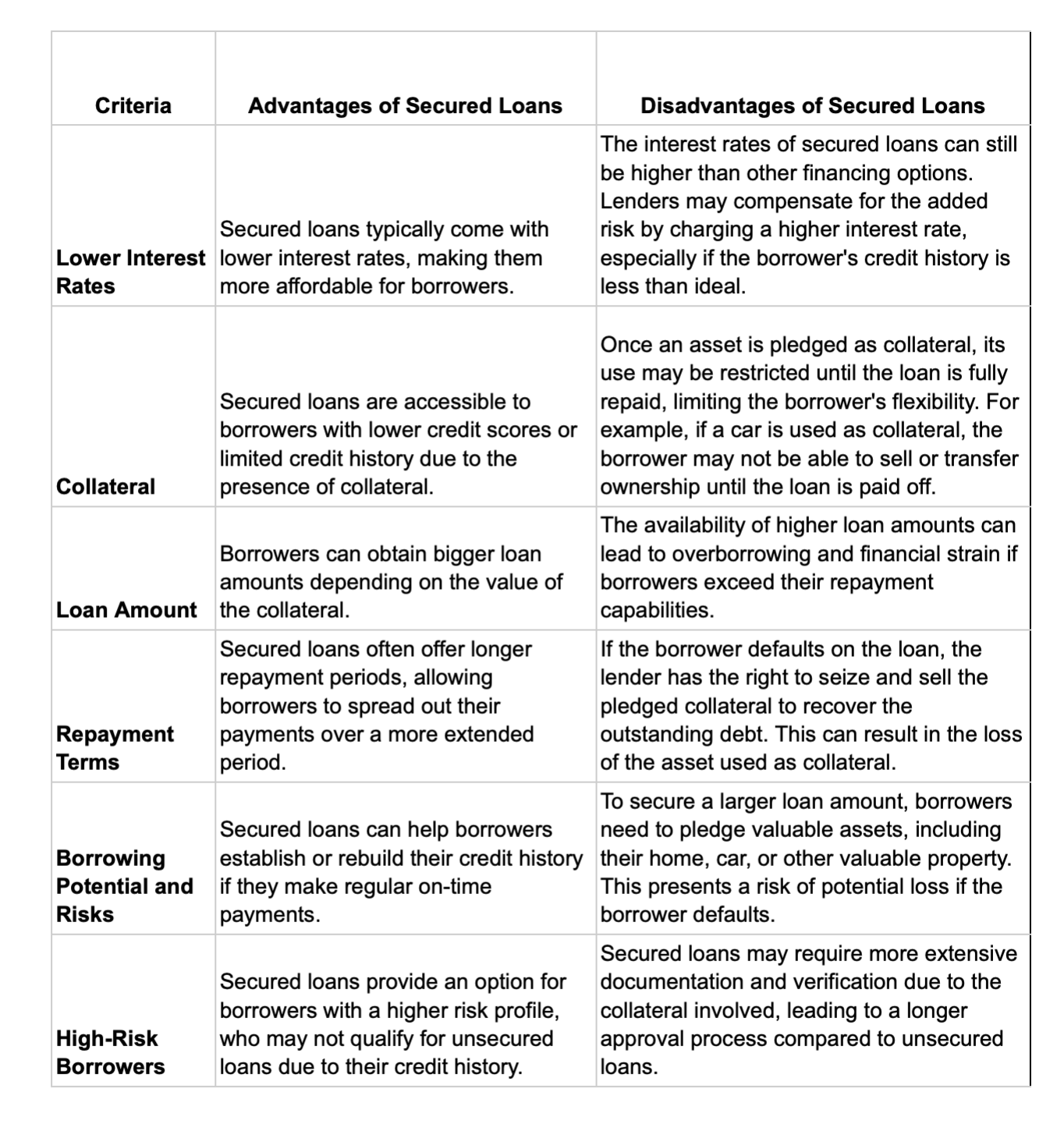

A secured loan is a type of credit that requires collateral to be pledged as security against the borrowed amount. Depending on the lender's policies, collateral can be any valuable asset, such as real estate, vehicles, stocks, or even high-value personal belongings.

The presence of collateral significantly reduces the lender's risk, making secured loans easier to obtain. Also, they often come with lower interest rates compared to unsecured loans.[1]

How Does a Secured Loan Work?

Secured loans provide lenders with an additional layer of security in the form of collateral. When a borrower applies for a secured loan, the lender assesses their creditworthiness along with the value and condition of the collateral offered.

If the lender approves the loan application, the borrower agrees to provide the asset as collateral until the loan is fully repaid. In the event of default, where the borrower fails to repay the loan, the lender has the legal right to seize and sell the collateral to recover the outstanding debt.

One of the key aspects borrowers should consider when opting for a secured loan is the Annual Percentage Rate (APR). The APR is a critical factor as it determines the overall cost of the loan, including the interest rate and any additional fees.

The Annual Percentage Rate (APR) for secured loans can vary depending on several factors, including

- the borrower's creditworthiness

- the type and value of the collateral, and

- the lender's policies

Generally, secured loans come with a wider range of APRs compared to unsecured loans due to the additional security provided by the collateral.

The APR for a secured loan typically falls within a range of 6% to 36%. Borrowers with excellent credit and valuable collateral are more likely to qualify for lower APRs, while those with lower credit scores or less valuable collateral may face higher APRs.

Apart from the APR, certain other fees might be charged while availing of secured loans. These fees can vary from lender to lender and may include:

- application fees

- origination fees

- appraisal fees (to assess the collateral's value), and

- late payment fees

It is essential for borrowers to carefully review the terms and conditions of the loan agreement to understand all the fees associated with a secured loan product.[2]

Unlock your credit potential and access personalized financial solutions that fit your needs. Contact Bright Money today!

Types of Secured Loans

There are various types of secured loans available, each tailored to meet different financial needs:

1. Home Equity Loans

Home Equity Loans are a type of secured loan where homeowners can borrow against the equity they have built up in their property. Equity is the difference between the home's current market value and the amount still owed on the mortgage. These loans often come with fixed interest rates and predictable monthly payments.

The Annual Percentage Rate (APR) for home equity loans typically ranges from 3% to 10% or more, depending on factors like credit score, loan amount, and loan term. To qualify for a home equity loan, borrowers generally need a good to excellent credit score, usually above 660. A higher credit score may result in more favorable loan terms and lower APR.

Example: Sarah owns a home worth $300,000 and still owes $150,000 on her mortgage. She has a credit score of 720. Sarah applies for a home equity loan and is approved with an APR of 5%. She borrows $50,000 using her home's equity, and the loan term is 10 years.

2. Auto Loans

Auto loans enable people to finance the purchase of an automobile since the car is used as collateral. The car itself acts as collateral for the loan, and the lender has the right to repossess the car in the event that the borrower falls behind on payments.

The annual percentage rate (APR) for auto loans can range significantly, from 2% to 10% or more, depending on variables like credit score, loan length, and the age and condition of the vehicle. Borrowers with credit scores over 660 are typically viewed as more creditworthy for vehicle loans, which can result in lower interest rates and better loan terms.

For instance, John wants to buy a new car valued at $25,000. He has a credit score of 700. John applies for an auto loan with a 5-year term and is approved with an APR of 4.5%. He makes a down payment of $5,000 and finances the remaining $20,000 through the auto loan.

3. Secured Personal Loans

Secured personal loans allow borrowers to use valuable assets, such as jewelry, savings accounts, or investments, as collateral to secure the loan. These loans are an option for individuals who may not want to risk their home or car as collateral.

The APR for secured personal loans typically ranges from 3% to 36% or more, depending on factors like credit score, the value of the collateral, and the loan amount. While secured personal loans may be available to borrowers with lower credit scores, having a higher credit score can help secure a lower APR and more favorable loan terms.

For example, Lisa decided to undertake a home renovation project but required additional funds. She opted for a secured personal loan to build her credit and access the necessary money, using her valuable art collection as collateral. In this endeavor, Lisa took the assistance of Bright Money, a trusted platform known for its expertise in credit-building solutions.

By leveraging her art collection and the guidance of Bright Money, Lisa successfully secured the funds she needed while also taking a step towards enhancing her creditworthiness.[3]

4. Credit Builder Loan (CB Loan)

A Credit Builder Loan is a type of loan designed to help individuals build or improve their credit scores. Unlike traditional loans, the funds from a credit builder loan are not disbursed upfront. Instead, the lender holds the loan amount in a separate account while you make regular monthly payments over a fixed period. The funds are disbursed when the amount is paid in full, which also improves the credit history of the lender.

The APR for credit builder loans is generally lower compared to other types of loans, ranging from 4% to 12% or more, depending on the lender and the loan amount. Credit builder loans are accessible to individuals with limited or poor credit history. Since the loan is designed to help build credit, lenders often consider other factors, such as income and financial stability, rather than focusing solely on credit scores.

Let's say Arthur applies for a credit builder loan for $1,000 with a 12-month repayment term. The lender holds the $1,000 in a locked account, and Arthur makes monthly payments of $83.33. After successfully completing the payments, the lender unlocks the $1,000, helping Arthur establish a positive credit history.

5. Home Buying Loan

A Home Buying Loan, also known as a mortgage, is a type of loan specifically designed to help people finance the purchase of a home. Unlike most other loans, a home-buying loan is secured by the property itself, meaning if you fail to repay the loan, the lender can take possession of the home through foreclosure.

Mortgage APRs might differ depending on things like credit score, down payment, loan length, and market conditions. Typically, rates fall between 3% and 6% or more. A credit score of 620 or better is typically required for consumers to get approved for a mortgage with favorable conditions. A lower APR and a smaller down payment may be required in exchange for a higher credit score.

Example: Ben wants to put down $50,000 (20% of the purchase price) on a $250,000 home. His credit rating is 740. After a bank evaluates Ben's creditworthiness, income, and other variables, the bank approves him for a mortgage with an APR of 4.25%. Ben makes monthly payments to the lender until the loan is entirely repaid during the course of the mortgage's 30-year term.

Places to Consider for Secured Loan Applications

Online Lenders: Many online lending platforms offer secured loans, providing borrowers with a convenient and accessible way to apply for financing while comparing various offers available in the market. You can also visit Bright Money to take a secured loan to build credit.

Banks: Traditional banks are a common source for secured loans, and they often offer various loan options secured by assets such as homes, vehicles, or savings accounts.

Credit Unions: Credit unions also provide secured loan options and may offer competitive rates to their members.

Peer-to-Peer Lending Platforms: Peer-to-peer lending connects individual investors with borrowers and can be a viable option for securing a loan with collateral.

Financial Institutions: Some specialized financial institutions may focus solely on secured lending, offering tailored solutions based on specific types of collateral. [4]

Read more: 3 reasons to use personal loans to pay off debt

Conclusion

Secured loans play a vital role in the financial ecosystem, providing a valuable financing option for individuals and businesses alike. Borrowers gain access to more favorable terms by offering collateral, while lenders benefit from reduced risk. It is essential for borrowers to carefully evaluate their financial situation, future earning potential, and ability to repay before opting for a secured loan.

Furthermore, understanding the terms and conditions of the loan agreement and diligently adhering to the repayment schedule can help borrowers avoid potential risks and make the most of this valuable financial tool.

Ready to take control of your finances? Experience the power of Bright Money and achieve financial freedom. Download the app now and start managing your money like never before!

References:

- https://www.investopedia.com/secured-loans-5076025

- https://www.experian.co.uk/consumer/loans/types/secured-loans.html#:~:text=Secured%20loans%20%E2%80%93%20also%20known%20as,of%20getting%20their%20money%20back

- https://navi.com/blog/types-of-loans/

- https://navi.com/blog/types-of-loans/

FAQs

Q. Can I apply for a secured loan if I don't own a home or a car?

Yes, secured loans can be obtained using various valuable assets as collateral, not limited to homes or cars. Lenders may accept assets like jewelry, high-value personal belongings, or even savings accounts as collateral. Always check with the lender to understand the acceptable collateral types and loan terms.

Q. Can I get a secured loan with bad credit?

While bad credit may limit your options, some lenders offer secured loans to individuals with poor credit. Collateral reduces the risk for the lender, increasing your chances of approval. However, be prepared for higher interest rates and stricter terms.

Q. What happens if I default on a secured loan?

If you default on a secured loan, the lender can seize the collateral and sell it to recover the outstanding debt. This could result in the loss of the asset and hurt your credit score.

Q. What types of assets can be used as collateral for a secured loan?

Various assets can be used as collateral, including real estate, vehicles, savings accounts, certificates of deposit, and valuable possessions like jewelry. The value and type of asset accepted will depend on the lender's policies.

Q. Can I repay a secured loan early?

Yes, in many cases, you can repay a secured loan before the agreed-upon term ends. However, check the loan agreement for any prepayment penalties. Early repayment can save you on interest but may involve additional fees.

*Bright Credit is a line of credit that can be used to pay off your credit cards. Subject to credit approval. Variable APR range from 9% –29.99%, Credit Limit ranges from $500 - $8,000. APR will vary based on prime rates. Final terms may vary depending on credit review. Monthly Minimum Payments are as low as 3% of the outstanding principal balance plus the accrued interest. Also, you can choose to pay more than the minimum due if you want to pay down the loan faster. Credit line originated by Bright or CBW Bank, Member FDIC. Products and services are subject to state residency and regulatory requirements. Bright Credit is currently not available in all states.