You are now leaving the Bright website and entering a third-party website. Bright has no control over the content, products, or services offered, nor the security or privacy of information transmitted to others via their website. We recommend that you review the privacy policy of the site you are entering. Bright does not guarantee or endorse the products, information, or recommendations provided on any third-party website.

Did you know that according to a poll, almost 20% of consumers believe that canceling a credit card will have a favorable influence on their credit scores? In the world of personal finance and credit management, the question of whether cancelling a credit card can hurt your credit score is a common concern. The short answer is: it depends.

There are various factors to consider, and the impact on your credit score can vary from person to person. But, before taking such a step, it's crucial to get an idea of the potential impact on your credit score.

Before diving more into the topic we recommend you to read about when you should think of closing a credit card and how to close a credit card by Bright Money!

This article delves into the intricacies of canceling a credit card and how it can affect your creditworthiness.

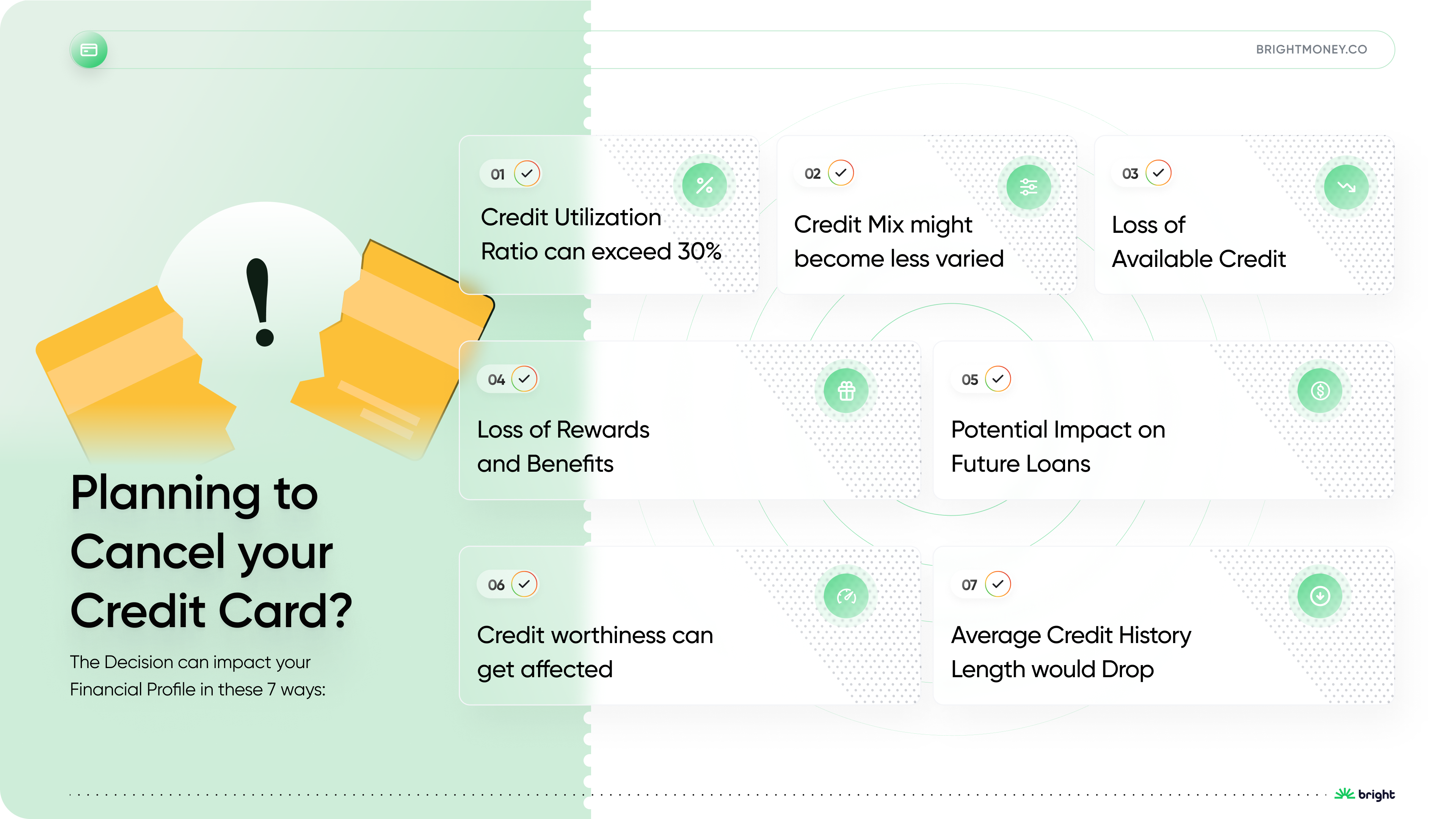

What are the Effects of Canceling a Credit Card?

1. Credit Utilization Ratio

The portion of your available credit that you are now utilizing is known as your credit usage ratio. It's a significant element in figuring out your credit score.

Your credit usage ratio, for instance, would be 40% ($6,000 / $15,000) if you had three credit cards with $5,000 credit limits on each ($15,000 total) and $2,000 balances on each card ($6,000 total).

Your credit usage ratio would rise to 60% ($6,000 / $10,000) if you chose to cancel one card, making your total amount of accessible credit $10,000. Since excessive credit utilization may signal a larger risk to lenders, it might have a negative effect on your credit score.

2. Credit History Length

The length of your credit history plays a crucial role in your credit score calculation. Lenders like to see a longer credit history as it shows your ability to manage credit over time. For instance, let's say you have three credit cards. Card A is five years old, Card B is three years old, and Card C is one year old. If you cancel Card A, your average credit history length drops, potentially affecting your credit score.

3. Credit Mix

Credit bureaus assess your credit mix to determine how well you manage various types of credit. A diverse credit mix, including credit cards, mortgages, and installment loans can impact your credit score positively. FICO states that closing a credit card account can never help your FICO score and can often hurt it. If you cancel a credit card, especially if it's your only credit card account, your credit mix might become less varied.

4. Loss of Rewards and Benefits

Many credit cards offer various rewards and benefits, such as cash back on purchases, travel points, or discounts. For example, a rewards card might offer 3% cashback on groceries and 2% on gas. If you cancel the card, you'll miss out on these rewards, potentially losing money-saving opportunities.

5. Potential Impact on Future Loans

When you apply for a loan, the lenders evaluate your credit history so as to assess your creditworthiness. A long and positive credit history demonstrates financial responsibility. If you cancel a credit card, it could signal to lenders that you're closing accounts, potentially raising questions about your financial stability.

6. Creditworthiness can get Affected

Your creditworthiness determines your ability to qualify for loans and credit at favorable terms. When you cancel a credit card, it may temporarily affect your creditworthiness, especially if the card had a significant credit limit and positive payment history.

7. Loss of Available Credit

Canceling a credit card reduces your total available credit, which can be a concern in emergencies. For example, if you face an unexpected medical expense or car repair, having less available credit might limit your ability to handle such situations.

Manage Debt wisely; refinance your high-interest credit cards with Bright Money!

What are the Alternatives to Canceling a Credit Card?

A study conducted found that consumers with credit scores above 720 experienced an average score drop of 15-45 points after closing a credit card.

Conversely, consumers with lower credit scores (around 600) saw a more substantial score drop, ranging from 45 to 65 points, after closing a credit card account. Before you rush to cancel a credit card, consider these alternatives that can help you maintain a healthy credit score:

1. Credit Card Product Change

Certain credit card issuers provide the option of changing to a different credit card within their product range. This allows you to retain your existing credit line and account history while adapting to your evolving financial needs. If your lifestyle or spending patterns have changed, switching to a more suitable card with better rewards or benefits may be a prudent solution.

2. Temporarily Freeze the Card

If the temptation to use the credit card is becoming a challenge, inquire with your card issuer about the option to freeze the card temporarily. During the freeze period, no new charges can be made, which provides a sense of control over your spending without negatively affecting your credit score or account status.

3. Pay Down the Credit Card Balance

If your motivation to cancel the credit card is due to a high outstanding balance, it's essential to prioritize paying down the debt instead. Reducing the balance improves your credit utilization ratio, which can have a positive impact on your credit score. Moreover, paying off the debt saves you money on interest payments and brings you closer to achieving financial freedom.

4. Consolidate Credit Card Debt

Debt consolidation is a desirable solution for people who manage many credit cards and liabilities. Repayment becomes more reasonable by combining all of your credit card bills into a single, lower-interest loan. You may cut down on interest costs and speed up the process of getting out of debt by consolidating your debts. The Bright Builder can help you out with Debt Consolidation!

5. Credit Card Balance Transfer

If you find yourself burdened by a high-interest credit card balance, exploring the option of a credit card balance transfer can be advantageous. This involves transferring your existing balance to a new card with a promotional low or 0% APR for a specified introductory period. Balance transfers provide temporary relief from high-interest charges, allowing you to focus on repaying the debt without accumulating additional interest.

6. Utilize the Credit Card Responsibly

Rather than canceling the credit card, adopting responsible usage habits can have long-term benefits. Making timely payments, avoiding carrying high balances, and minimizing unnecessary fees demonstrate responsible credit card usage. By doing so, not only do you prevent falling into excessive debt, but you also build and maintain a positive credit history, which can serve you well in future financial endeavors.

7. Negotiating with the Credit Card Issuer

Sometimes, it's worth taking the initiative to reach out to the credit card issuer's customer service department to negotiate better terms. If high-interest rates or annual fees are the primary concerns, explaining your financial situation and demonstrating a strong payment history may lead to improved conditions. Credit card companies often value customer retention and may be willing to offer incentives to retain your business.

8. Paying on time to keep your Credit Card active

Paying your credit card bills on time is essential to keep your card active and maintain a positive credit history. Timely payments demonstrate your financial responsibility, strengthen your creditworthiness, and pave the way for better borrowing opportunities and financial flexibility in the future.

Manage Debt wisely; refinance your high-interest credit cards with Bright Money!

The Bottom Line

Research suggests that 15% of consumers regret closing a credit card account due to the subsequent negative impact on their credit scores. In conclusion, canceling a credit card can have implications on your credit score, and it's essential to weigh the pros and cons before making any decision. While there are situations where canceling a credit card may be necessary, it's essential to consider alternatives that can help preserve your credit score. Remember, maintaining a good credit score is a valuable asset that opens doors to better financial opportunities.

When managing your credit, always strive to make timely payments, keep credit utilization low, and maintain a diverse mix of credit accounts. By following these practices and being mindful of your credit decisions, you can ensure that your credit score remains strong and serves you well in your financial journey.

Remember, understanding your credit is a crucial aspect of your overall financial health. So, whether you're considering canceling a credit card or applying for a new one, make informed decisions to achieve your financial goals.

Manage Debt wisely; refinance your high-interest credit cards with Bright Money!

Recommended Reads:

1. Understanding Secured Loans

References:

1. https://www.bankrate.com/finance/credit-cards/credit-card-cancellation-survey/

- https://www.fico.com/blogs/more-scoring-myths-closing-credit-cards

- https://www.experian.com/blogs/ask-experian/why-did-my-credit-score-drop/

- https://www.bankrate.com/finance/credit-cards/is-closing-a-credit-card-good-or-bad/

Frequently Asked Questions (FAQs)

1. Does canceling a credit card impact my credit score?

A: Yes, canceling a credit card can potentially hurt your credit score. When you close a credit card account, it reduces your available credit, which can increase your credit utilization ratio. A higher utilization ratio may negatively affect your credit score.

2. How does credit utilization ratio affect my credit score?

A: Credit utilization ratio is the percentage of your total available credit that you are currently using. A higher utilization ratio indicates a greater reliance on credit, which can be perceived as a higher credit risk by lenders and credit bureaus, potentially lowering your credit score.

3. Are there instances where canceling a credit card won't impact my credit score?

A: Yes, in some cases, canceling a credit card may have minimal impact on your credit score. If the card you are closing has a very low credit limit and you have other credit cards with substantial credit limits, the effect on your credit utilization ratio might be negligible.

4. Can keeping unused credit cards open to improve my credit score?

A: Keeping unused credit cards open can have a positive impact on your credit score by increasing your overall available credit, which lowers your credit utilization ratio. Additionally, older accounts contribute positively to your credit history's length, which is a factor in determining your credit score.

5. How long does a closed credit card account stay on my credit report?

A: Closed credit card accounts can remain on your credit report for up to ten years. However, the positive payment history associated with the closed account can still contribute positively to your credit score during this time.

6. Will closing a credit card with a balance affect my credit score?

A: Closing a credit card with an outstanding balance can have a more significant impact on your credit score. It may lead to a higher credit utilization ratio, which can negatively affect your credit score. It's generally recommended to pay off the balance before closing the account.

7. Should I cancel a credit card with an annual fee?

A: If you have a credit card with an annual fee that you no longer find valuable, consider downgrading to a no-fee version of the same card or exploring other credit card options with no annual fee. Canceling a card with an annual fee outright may negatively impact your credit score, depending on your individual credit utilization and credit history.

8. Can closing a credit card affect my ability to get new credit?

A: Yes, closing a credit card account can impact your ability to obtain new credit. When you close a credit card, it reduces your available credit, which may affect your creditworthiness in the eyes of lenders. This could potentially lead to higher interest rates or limited credit options when applying for new credit.

9. How can I avoid the negative impact of canceling a credit card?

A: To mitigate the potential negative impact of canceling a credit card, consider paying off any outstanding balances before closing the account. Additionally, explore alternatives to cancelation, such as downgrading the card or negotiating with the credit card issuer for better terms.

10. Should I seek professional advice before canceling a credit card?

A: If you are unsure about the consequences of canceling a credit card or need guidance on managing your credit, seeking advice from a financial advisor or credit counselor is recommended. They can help you make informed decisions based on your unique financial situation and goals.