You are now leaving the Bright website and entering a third-party website. Bright has no control over the content, products, or services offered, nor the security or privacy of information transmitted to others via their website. We recommend that you review the privacy policy of the site you are entering. Bright does not guarantee or endorse the products, information, or recommendations provided on any third-party website.

Have you ever found yourself drowning in a sea of debt, struggling to keep your financial head above water? If yes, you're not alone. In the United States, household debt reached a staggering $17.06 trillion in 2023, according to the Federal Reserve. As the weight of various financial obligations bears down on individuals and families, the need for effective debt management tools has never been more critical. That's where the power of credit cards and the art of debt transfer come into play.

Imagine being able to wave a financial magic wand that allows you to move your high-interest debts to a more manageable platform. Picture reducing the crushing burden of interest payments and simplifying your financial life with a single, consolidated monthly payment. It is not a pipe dream—it is the reality of debt transfer to credit cards.

In this era of financial complexity and economic uncertainty, understanding the nuances of debt transfer to credit cards is a vital skill. It is a financial strategy that offers a lifeline to those seeking relief from their debt-related woes. However, before you embark on this journey, you need to know what debts can be transferred, the potential benefits and pitfalls, and the intricate dance of financial choices you must make.

Join us on a comprehensive exploration of this financial landscape as we answer essential questions, provide insights into the types of debts that can be shifted onto credit cards, and offer expert guidance on making the most of this financial tool. Welcome to the world of Debt Transfer to Credit Cards: Your Path to Financial Freedom.

Read more: What is a balance transfer?

Understanding Balance Transfers

Before diving into the details of which debts can be transferred to a credit card, it is important to understand the concept of a balance transfer. A balance transfer involves moving the outstanding balance from one financial account to another, typically from a higher-interest account to one with a lower interest rate. Credit cardholders often use this feature to consolidate and potentially reduce the cost of their debt.

Here's how a balance transfer typically works:

- Selecting a Destination Card: To initiate a balance transfer, you need a credit card that offers this feature. Not all credit cards allow balance transfers, so it is essential to choose a card that specifically promotes this option

- Providing Account Information: You'll need to provide the account information for the debt you wish to transfer, including the account number and the amount you want to move

- Approval and Processing: Once you submit the request, the credit card issuer will review and decide whether to approve the transfer. If approved, they will process the transfer, and the amount will be moved from the original account to your credit card

- New Terms and Conditions: Be aware that when you transfer a balance to a credit card, you are essentially opening a new credit line. This means you will have a new set of terms and conditions, including an interest rate, credit limit, and potential fees

- Repayment: You'll be responsible for paying off the transferred balance according to the terms of the credit card agreement. This often involves making monthly payments that include both principal and interest[1]

Unlock Financial Freedom Today! - Sign up for Bright Money and take control of your finances.

Now that we have a basic understanding of balance transfers, let us explore the types of debts you can transfer to a credit card.

Types of Debts You Can Transfer

Not all debts are eligible for transfer to a credit card, but many common forms of consumer debt can be moved to a credit card account. Here are some of the most typical types of debt that can be transferred:

1. Credit Card Balances

One of the most common uses of balance transfers is to move existing credit card debt to a new credit card. This can be an effective strategy if you have high-interest credit card debt and want to take advantage of a lower interest rate offered by another card.

Example: You have a credit card with a $5,000 balance at a high interest rate of 20%. You apply for a new credit card with a 0% introductory APR on balance transfers for 12 months and transfer the $5,000 balance to the new card to save on interest.[2][6][7][8][9]

2. Personal Loans

If you have an unsecured personal loan with a high interest rate, you can transfer the outstanding balance to a credit card. This can provide significant interest savings if the new credit card offers a lower rate.

Example: You have an unsecured personal loan with a balance of $10,000 at an interest rate of 15%. You open a new credit card with a 10% APR on balance transfers and transfer the personal loan balance to the credit card to lower your interest costs.[2][6][7][8][9]

3. Auto Loans

In some cases, you may be able to transfer the outstanding balance of an auto loan to a credit card. However, this can be more challenging and is less common than other types of transfers, and it typically requires a credit card with a high credit limit.

Example: You have an auto loan with a balance of $15,000 at a 7% interest rate. You find a credit card with a $15,000 credit limit and a promotional 0% APR on balance transfers for 18 months, allowing you to move the auto loan balance to the credit card temporarily.[2][6][7][8][9]

4. Student Loans

Federal and private student loans are generally not eligible for balance transfers to credit cards. However, some financial institutions offer specialized products that allow for student loan refinancing or consolidation using a credit card, although these often come with their own terms and conditions.

Example: Most student loans can't be directly transferred to credit cards. However, you find a financial institution that offers a student loan consolidation program using a credit card. You consolidate your $20,000 in student loans onto a credit card with a lower interest rate.[2][6][7][8][9]

5. Medical Bills

Medical bills can sometimes be transferred to a credit card, especially if they are not covered by insurance and have become a significant financial burden. Using a credit card with a lower interest rate can help you manage these expenses more effectively.

Example: You have $3,000 in medical bills that insurance doesn't cover. You apply for a credit card with a lower interest rate compared to the medical billing company's financing plan and transfer the $3,000 balance to the credit card.[2][6][7][8][9]

6. Store Credit Accounts

Store credit cards often come with high interest rates. You can transfer the balance from a store credit card to a general-purpose credit card with a lower interest rate, potentially saving money on interest charges.

Example: You have a store credit card with a balance of $1,500 and a high-interest rate of 25%. You decide to transfer the balance to a general-purpose credit card with a lower interest rate of 15% to reduce interest costs.[2][6][7][8][9]

7. Tax Debt

While it is possible to pay taxes using a credit card, it is generally not advisable due to the high fees associated with tax payments. However, some individuals may choose to use a credit card to pay taxes and then transfer the balance to a card with a lower interest rate if they cannot pay the full amount immediately.

Example: You owe $5,000 in taxes and are unable to pay the full amount upfront. You use your credit card to make the tax payment but then quickly transfer the $5,000 balance to another credit card with a lower interest rate to avoid excessive interest charges.

It is important to note that the eligibility and terms for balance transfers can vary significantly between credit card issuers and financial institutions. Before proceeding with a balance transfer, carefully review the terms and conditions of the specific credit card you plan to use. Verify the related clauses to ensure your intended debt can be transferred and understand any associated fees or limitations.[2][6][7][8][9]

Join Thousands of Smart Savers! - Join our community of savvy users who are already on the path to financial success. Sign up now!

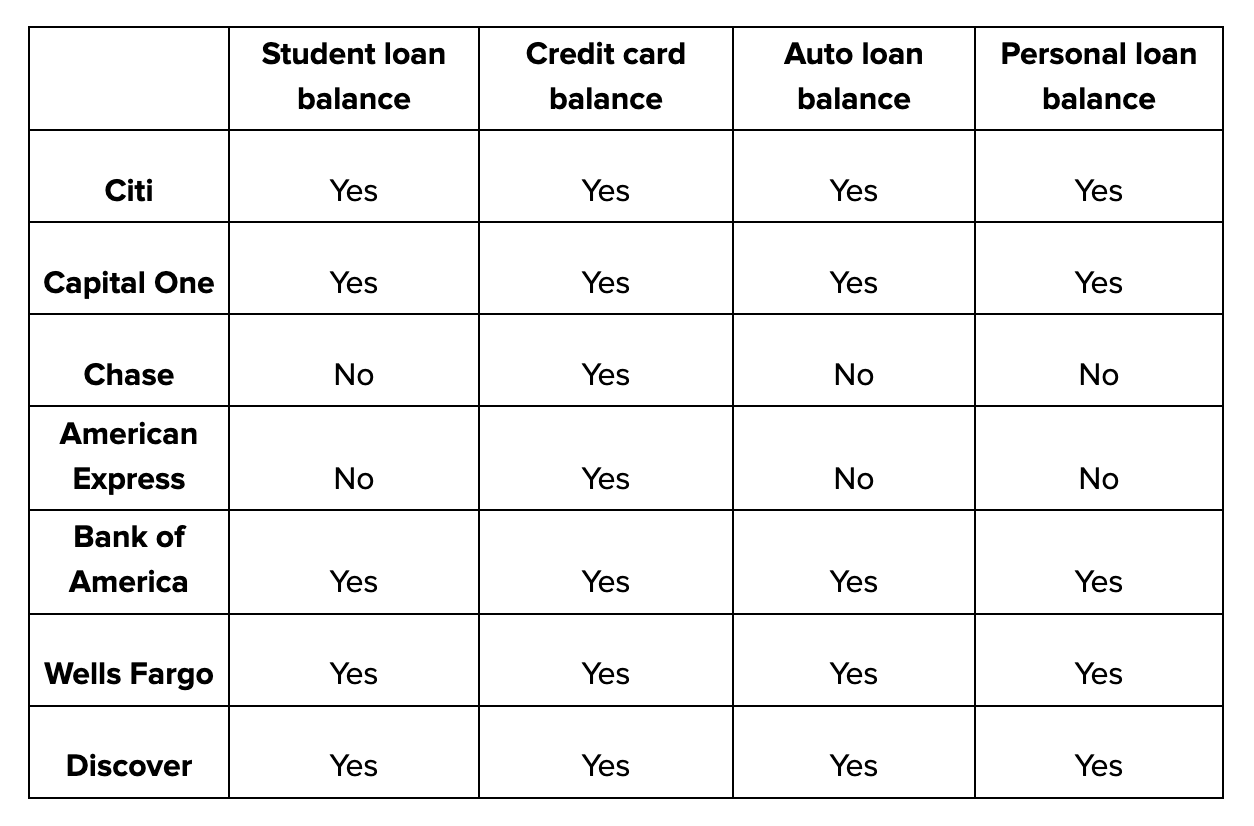

Debts Eligible for Balance Transfer by Different Banks

Although these regulations may change, many issuers permit you to transfer various debts to a balance transfer card as long as they are not from an account with the same issuer. About your options, speak with your issuer.

Now, let's explore the potential risks and considerations associated with transferring debt to a credit card.

Risks and Considerations

While balance transfers can offer significant advantages, certain risks and considerations must be studied before proceeding with this financial strategy:

1. Balance Transfer Fees

Most credit card issuers charge a balance transfer fee, typically ranging from 3% to 5% of the transferred amount. While the potential interest savings may outweigh this fee, it is important to factor it into your overall cost analysis.

2. Introductory APR Expiration

The attractive 0% APR or low introductory rate offered on balance transfers is usually temporary. It is essential to know when this promotional period expires and what the post-promotion interest rate will be. If you haven't paid off the transferred balance by that time, you could end up with higher interest charges.

3. Impact on Credit Score

Opening a new credit card and transferring a balance can temporarily affect your credit score. The credit inquiry associated with a new card application and the reduction in average account age may lead to a slight dip in your score. However, responsible management of the new credit card can have a positive long-term impact on your credit score.

4. Temptation to Accumulate More Debt

After transferring existing debt to a credit card, there may be a temptation to accumulate more debt on the newly available credit line. This can lead to a cycle of increasing debt and financial stress if not managed carefully.

5. Eligibility and Approval

Not everyone will qualify for a credit card with a high enough credit limit to accommodate their desired balance transfer. Your credit history and credit score will play a significant role in determining your eligibility and the terms you receive.[4]

Don't Miss Out on Financial Wellness! - Get access to personalized financial guidance and start building your financial wellness. Sign up now!

How to Transfer Debt to a Credit Card?

If you've weighed the advantages and disadvantages and decided that transferring debt to a credit card is the right financial move for you, here are the steps to follow:

- Select the Right Credit Card: Research and choose a credit card that offers favorable terms for balance transfers. Look for cards with low or 0% introductory APR offers and reasonable balance transfer fees

- Check Eligibility: Review the credit card issuer's eligibility criteria to ensure you meet the requirements. Your credit score, credit history, and income may all play a role in the approval process

- Apply for the Credit Card: Complete the credit card application process, which may involve providing personal information, financial details, and consent for a credit check

- Wait for Approval: Once you submit the application, the credit card issuer will review your information and decide whether to approve it. This can take a few days to a few weeks, depending on the issuer

- Receive Your Credit Card: If approved, you'll receive your new credit card in the mail. Carefully review the terms and conditions and the details of the balance transfer offer

- Initiate the Balance Transfer: Contact the credit card issuer to initiate the balance transfer. You'll need to provide the necessary information for the debt you wish to transfer, including the account number and the amount

- Monitor the Transfer: Keep a close eye on the transfer process to ensure it goes smoothly. Confirm that the debt has been successfully moved to your new credit card account

- Make Timely Payments: Begin making monthly payments on the transferred balance according to the terms of the new credit card agreement. Missing payments or paying late can result in penalties and the loss of promotional APR offers[5]

Tips for Successful Debt Transfers to a Credit Card

To make the most of a balance transfer to a credit card and avoid common pitfalls, consider the following tips:

- Read the Fine Print: Carefully review the terms and conditions of the credit card offer, paying attention to the introductory APR period, balance transfer fees, and post-promotion interest rates

- Create a Repayment Plan: Develop a clear plan to pay off the transferred debt within the promotional period to maximize interest savings. Calculate how much you need to pay each month to achieve this goal

- Avoid New Debt: While paying off transferred debt, refrain from accumulating new debt on the credit card. Focus on reducing your existing balance to achieve your financial goals

- Monitor Your Credit: Keep a close watch on your credit score and credit report to ensure that the balance transfer and payments are accurately reflected. This can help you identify and address any issues promptly

- Consider Professional Advice: If you have substantial debt or complex financial circumstances, it may be beneficial to consult with a financial advisor or credit counselor before proceeding with a balance transfer[5]

Read more: Step-by-step guide for a successful credit card balance transfer

Conclusion

A useful financial option for people trying to manage and reduce their debt load is transferring debt to a credit card. You can benefit from cheaper interest rates, make debt repayment easier, and perhaps even raise your credit score. To achieve a successful and profitable balance transfer, it is crucial to comprehend the many types of debts that can be transferred, carefully weigh the benefits and drawbacks, and adhere to best practices.

Before proceeding with a balance transfer, conduct thorough research, choose the right credit card, and develop a clear repayment plan. By doing so, you can harness the power of balance transfers to achieve your financial goals and work toward a debt-free future.

Your Financial Dreams, One Click Away! - Your dreams are within reach. Sign up for Bright Money and start turning them into reality.

References:

- https://www.investopedia.com/credit-cards/balance-transfer-credit-card/

- https://www.bankrate.com/finance/credit-cards/debts-you-can-transfer-to-a-credit-card/

- https://spiritfinancialcu.org/take-advantage-of-a-balance-transfer-credit-card-offer

- https://www.forbes.com/advisor/credit-cards/the-pros-and-cons-of-balance-transfer-credit-cards/#:~:text=While%20a%20balance%20transfer%20can,credit%20utilization%20rate%20over%20time.

- https://www.nerdwallet.com/article/credit-cards/simple-steps-to-transfer-credit-card-balance

FAQs

FAQ 1: Can I transfer mortgage debt to a credit card?

No, you generally cannot transfer mortgage debt to a credit card. Mortgage loans are typically secured by your home, making them a unique type of debt that cannot be transferred to an unsecured credit card. Instead, mortgage debt is typically refinanced through a mortgage refinance loan, which involves replacing your existing mortgage with a new one, often with different terms and interest rates.

FAQ 2: Are there limits on the amount I can transfer to a credit card?

Yes, credit card issuers typically impose limits on the amount you can transfer. This limit is often a percentage of your credit card's credit limit, such as 80% or 90%. Keep in mind that the balance transfer fee, if applicable, is also factored into this limit. It is crucial to check with your credit card issuer to understand the specific limits that apply to your account.

FAQ 3: Will transferring debt to a credit card hurt my credit score?

Transferring debt to a credit card can have both positive and negative effects on your credit score. Initially, it may cause a slight dip due to the credit inquiry associated with opening a new card and any changes in your credit utilization ratio. However, as you make timely payments and reduce your overall debt, it can contribute to long-term credit score improvement.

FAQ 4: Can I transfer debt between credit cards?

Yes, you can transfer debt from one credit card to another. This is known as a balance transfer between credit cards. It is a common strategy to move debt from a high-interest card to one with a lower interest rate or a promotional 0% APR offer. Balance transfers between credit cards typically incur a balance transfer fee, so you must consider this cost before freezing a plan.

FAQ 5: What happens if I miss a payment on my transferred debt?

Missing a payment on your transferred debt can have negative consequences. It can result in late payment fees, the loss of any promotional APR offers, and a negative impact on your credit score. To avoid this, set up reminders and ensure you make all payments on time, especially during the promotional APR period when interest rates are low or 0%.