You are now leaving the Bright website and entering a third-party website. Bright has no control over the content, products, or services offered, nor the security or privacy of information transmitted to others via their website. We recommend that you review the privacy policy of the site you are entering. Bright does not guarantee or endorse the products, information, or recommendations provided on any third-party website.

Credit Scores play a pivotal role in our financial lives. These three-digit numbers can determine whether you're approved for a loan, the interest rate you'll pay on that loan, and even your eligibility for certain job opportunities or rental properties. Given the significant impact Credit Scores have on our financial well-being, it's only natural to want to understand how they work and what factors influence them.

One common misconception about Credit Scores is the belief that carrying more Debt can lead to a higher Credit Score. This idea seems counterintuitive at first glance, as it is often advised to keep debt levels low to maintain good credit. However, it's essential to debunk this myth and clarify how Debt and Credit Scores are intertwined.

In this comprehensive article, we will explore the relationship between carrying Debt and your Credit Score. We will delve into the factors that affect your Credit Score, the role of Debt in credit scoring models, and how to use credit responsibly to improve and maintain a healthy Credit Score.

Read more: Debunking Common Credit Myths: What Really Affects Your Credit Score?

Will my Credit Score be higher if I carry more Debt?

Carrying more Debt typically doesn't result in a higher Credit Score. While responsible Debt management, like making on-time payments, can positively affect your score, excessive Debt or high credit utilization ratios can have a negative impact. A good Credit Score relies on various factors, not just the amount of Debt carried.

"Start Your Journey to Financial Freedom Today!" - Join Bright Money and take the first step towards managing your finances effortlessly. Sign up now to experience a brighter financial future.

Understanding Credit Scores

Before delving into the topic of carrying Debt and its impact on your Credit Score, let's start by understanding what a Credit Score is and why it's so crucial.

Think of a Credit Score as your financial report card. It's a number, usually between 300 and 850 in the US, that shows how trustworthy you are with borrowed money. The higher the score, the better. It is based on your credit history, like whether you pay bills on time, how much credit you're using compared to what you have, how long you've had credit, and the types of credit you have.

Why does it matter? Well, when you want to borrow money for things like a car or a house, lenders check your score to decide if they'll lend to you and at what interest rate. Higher scores mean better loan terms, while lower scores might mean paying more. So, keeping a good score is essential for financial flexibility.[1]

"Unlock a World of Financial Possibilities - Sign Up Now!" - Don't miss out on the opportunity to gain control over your money. Sign up for Bright Money and discover the endless possibilities that await you.

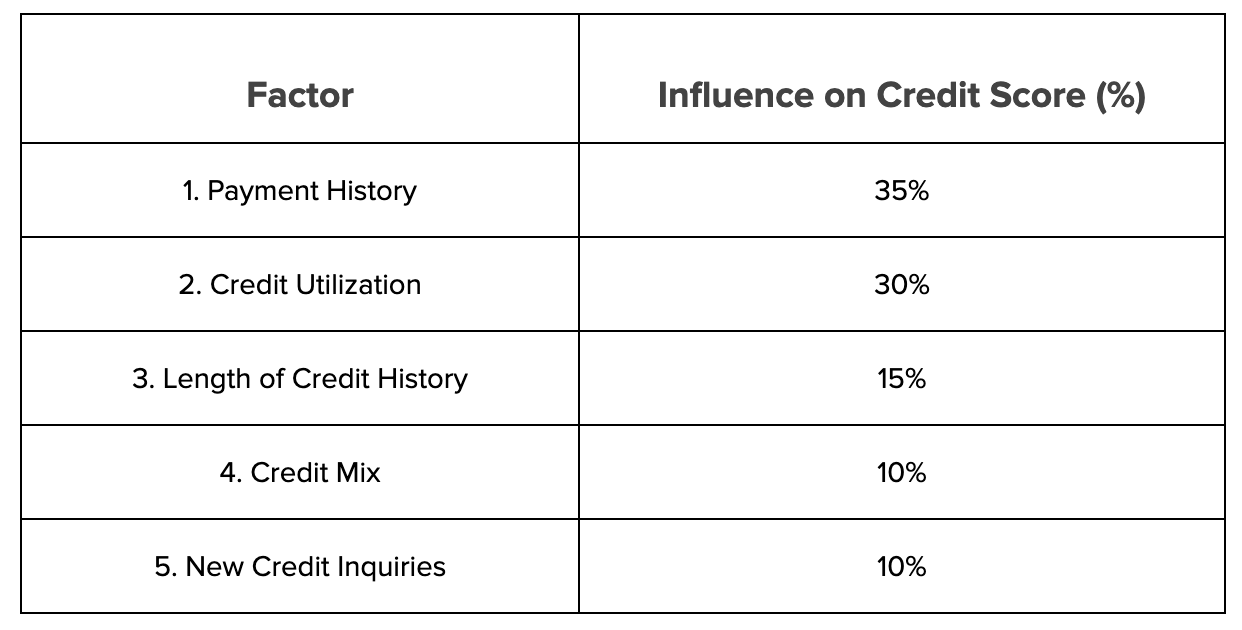

Certainly, here's a table summarizing the factors that influence your Credit Score:

Remember that these percentages are approximate and can vary depending on the specific credit scoring model used. Nevertheless, understanding these factors and how they impact your Credit Score is crucial for maintaining good credit and making sound financial decisions.

Now that we have a clear understanding of the factors that influence Credit Scores, let's explore the relationship between carrying Debt and Credit Ccores.

"Don't Wait - Secure Your Financial Future with Bright Money!" - Your financial well-being matters. Sign up for Bright Money now and take control of your finances with confidence.

Will my Credit Score be higher if I carry more Debt?

No, carrying more Debt will not necessarily lead to a higher Credit Score. In fact, it is a common misconception that having a substantial amount of Debt can improve your credit rating. Your Credit Score is influenced by various factors, and while responsible credit usage can positively impact it, excessive Debt can have detrimental effects.

Let's delve into the relationship between Debt and Credit Scores, explaining why responsible management of credit is crucial, and how carrying too much Debt can actually harm your creditworthiness.

How to maintain Debt to keep your Score higher?

To maintain a higher Credit Score through Debt management, consider this example:

Begin by strategically taking on a reasonable amount of Debt, like a manageable Credit Card or a small personal loan. Avoid excessive borrowing.

Next, consistently make on-time payments for your Debts. Punctuality in payments showcases your creditworthiness. For instance, paying your Credit card bill in full and on time each month is a positive practice.

Ensure that your creditors report your payment history to credit bureaus. This reporting is vital as it contributes to the calculation of your Credit Score. If your payments aren't reported, your responsible financial behavior won't be reflected accurately.

Over time, as you adhere to these steps, you'll observe a positive impact on your Credit Score. This upward trend will improve your financial prospects, granting you access to better credit options and lower interest rates. In summary, strategic Debt management, timely payments, and credit reporting are key elements in maintaining a high Credit Score.[2]

"Start Saving More, Worrying Less - Sign Up with Bright Money!" - Say goodbye to financial stress and hello to financial security. Join Bright Money today and start saving more while worrying less.

Improving and Maintaining a Healthy Credit Score

Now that we've clarified the relationship between carrying Debt and Credit Scores, let's explore how you can improve and maintain a healthy Credit Score.

1. Pay Your Bills on Time

As previously mentioned, your payment history is the most influential factor in your Credit Score. Consistently making on-time payments on your credit cards, loans, and other Debts is essential for maintaining and improving your Credit Score. Set up reminders or automatic payments to help ensure you never miss a due date.

2. Reduce Credit Card Balances

High credit card balances relative to your credit limits can harm your Credit Score. Aim to keep your credit card utilization ratio below 30%. If you have Credit Card Debt, create a plan to pay it as quickly as possible. Reducing your credit card balances can have a positive impact on your Credit Score.

3. Avoid Closing Old Credit Accounts

The length of your credit history is another significant factor in your Credit Score. Closing old credit accounts can shorten your credit history and potentially lower your score. Even if you no longer use a Credit Card, consider keeping the account open to maintain your credit history's length.

4. Limit New Credit Inquiries

As discussed earlier, too many hard inquiries within a short period can lower your Credit Score. Be selective when applying for new credit and only do so when necessary. Additionally, you can inquire with potential lenders about their credit inquiry policies to determine whether a soft inquiry is possible.

5. Monitor Your Credit Report

Regularly checking your credit report allows you to spot errors or inaccuracies that may be dragging down your Credit Score. You are entitled to a free annual credit report from each of the three major credit bureaus (Equifax, Experian, and TransUnion). Review your report at least once a year and dispute any inaccuracies you find.

6. Build a Positive Credit History

If you're new to credit or have a limited credit history, building a positive credit history is essential. You can start by applying for a secured Credit Card, becoming an authorized user on someone else's Credit Card, or taking out a credit-builder loan. These strategies can help you establish a positive credit history and boost your Credit Score over time.

7. Seek Professional Guidance if Needed

If you're facing significant credit challenges, it may be helpful to seek guidance from a certified credit counselor or financial advisor. They can provide personalized advice and strategies to improve your credit and manage your Debts effectively.[3]

Read more: 10 Traps to Avoid While Building Credit

Conclusion

Carrying more Debt does not inherently lead to a higher Credit Score. While certain aspects of Debt, such as making on-time payments and responsibly managing credit utilization, can positively influence your Credit Score, simply accumulating Debt without proper management can have adverse effects.

Understanding the factors that influence your Credit Score and practicing responsible Debt management is essential for maintaining and improving your creditworthiness. By consistently making on-time payments, keeping Credit Card balances in check, and being mindful of your credit inquiries, you can work toward achieving and maintaining a healthy Credit Score.

Remember that your Credit Score is a reflection of your financial responsibility, and it can have a significant impact on your financial opportunities and well-being. By staying informed and making informed financial decisions, you can ensure that your Credit Score works in your favor, helping you achieve your financial goals and secure a brighter financial future.

"Ready to Supercharge Your Savings? Join Bright Money!" - Begin your savings journey with Bright Money. Sign up today to access powerful tools and expert guidance that will help you save smarter and achieve your financial goals faster.

References:

- https://www.experian.com/blogs/ask-experian/credit-education/score-basics/understanding-credit-scores/

- https://www.cnbc.com/select/how-your-amount-of-debt-affects-your-credit-score/#:~:text=Consumers%20don't%20get%20rewarded,most%20important%2C%20Fay%20reminds%20us.

- https://www.hdfcbank.com/personal/resources/learning-centre/pay/how-to-maintain-a-good-credit-score

FAQs

1. Can carrying no debt negatively impact my Credit Score?

While it's essential to manage debt responsibly, having no debt doesn't inherently harm your Credit Score. In fact, some individuals choose to live debt-free, which is a responsible financial choice. Your Credit Score is primarily influenced by your credit history, payment behavior, and other factors mentioned in the article. If you've never taken on debt or have recently paid off all your debts, you may have a limited credit history, which can affect your Credit Score. However, this doesn't necessarily equate to a lower score. You can maintain a healthy credit score by making on-time payments, having diverse credit types, and managing your credit inquiries, even if you don't have outstanding debt.

2. How often should I check my Credit Score and report?

You should regularly monitor your Credit Score and report to detect errors or signs of identity theft. Many experts recommend checking your credit report at least once a year from each of the three major credit bureaus (Equifax, Experian, and TransUnion). You can obtain a free annual report from AnnualCreditReport.com. Additionally, some Credit Card issuers and financial institutions offer free Credit Score monitoring, allowing you to keep a closer eye on your credit health.

3. Can paying off a large debt boost my Credit Score significantly?

Paying off a substantial debt can have a positive impact on your Credit Score, especially if the debt has a high credit utilization ratio. However, the exact score increase can vary depending on your overall credit history and individual circumstances. Keep in mind that other factors, such as your payment history and the age of your accounts, also play significant roles in your Credit Score. While paying off debt is beneficial, it's essential to focus on overall responsible credit management to maintain a healthy score.

4. How long does it take to improve a poor Credit Score?

The time it takes to improve a poor Credit Score depends on several factors, including the severity of the negative information, your actions to improve your credit, and the specific credit scoring model used. Generally, you can start seeing improvement within a few months to a year if you consistently practice responsible credit habits, such as making on-time payments and reducing Credit Card balances. However, significant improvements may take several years, as negative information can stay on your credit report for seven to ten years. Patience and a commitment to positive credit behavior are key to rebuilding your credit.

5. Does checking my own Credit Score hurt my credit?

No, checking your own Credit Score does not harm your credit in any way. When you check your Credit Score or request a copy of your credit report, it results in a soft inquiry, which differs from the hard inquiries made by lenders when you apply for credit. Soft inquiries have no impact on your Credit Score, so feel free to monitor your credit as often as you'd like without worrying about negative consequences.