You are now leaving the Bright website and entering a third-party website. Bright has no control over the content, products, or services offered, nor the security or privacy of information transmitted to others via their website. We recommend that you review the privacy policy of the site you are entering. Bright does not guarantee or endorse the products, information, or recommendations provided on any third-party website.

When considering strategies for applying for debt consolidation, two prominent options emerge: balance transfer cards and personal loans. Each method offers a distinct approach to handling existing debts.

Should you choose a Balance Transfer Card or a Personal Loan?

Balance transfer cards allow individuals to transfer their debts to a single card, typically offering a low introductory interest rate. On the other hand, personal loans enable the consolidation of various debts into one loan with a fixed interest rate, potentially simplifying repayment schedules and reducing the overall interest paid over time. These options, while beneficial, carry different implications for one's credit profile and financial management. Understanding the specific features, benefits, and potential drawbacks is essential for making an informed decision that aligns with personal financial goals.

Understanding Balance Transfer Cards

A balance transfer (link) card allows you to transfer multiple debts, typically from high-interest credit cards, to a single card. This card often comes with an introductory offer of low or 0% interest, making it an attractive option for reducing interest payments in the short term.

The primary appeal of balance transfer cards lies in their introductory interest rates. These rates are significantly lower than standard credit card rates, sometimes as low as 0%. This period usually spans 12 to 21 months, offering a window where interest does not accumulate on the transferred amount.

While a lower interest rate is appealing, balance transfer cards often include a fee for transferring your existing debt. This fee typically ranges from 3% to 5% of the total transferred amount. When applying for a debt consolidation strategy using a balance transfer card, it's important to factor in these fees to determine if the transfer saves you money on interest in the long run.

Pros:

- Introductory 0% APR: Offers a period (typically 6 to 21 months) of no interest, allowing for faster debt repayment as payments go directly to the principal.

- Debt Consolidation: Enables consolidating multiple credit card debts into one payment, simplifying management.

- Potential for Lower Payments: If managed correctly, it can significantly reduce or eliminate debt during the promotional period.

Cons:

- Balance Transfer Fees: Generally charge 3% to 5% of the transferred amount, increasing overall debt.

- High Post-Promotion Interest Rates: Interest rates can rise significantly after the promotional period.

- Risk of Additional Debt: The temptation to accumulate more debt during the interest-free period.

Exploring Personal Loans

An alternative to balance transfer cards, personal loans offer a way to consolidate your debt into a single, fixed-term loan. Unlike balance transfer cards, personal loans provide a consistent interest rate throughout the repayment term and can be used to cover various types of debts, including secured loans.

Personal loans come with set repayment terms, typically two to five years. The interest rates on these loans vary based on your credit history and the lender but are generally fixed for the duration of the loan. This stability can benefit long-term financial planning, keeping your monthly payments constant.

You should know some pros and cons before applying for a debt consolidation.

Pros and Cons of Personal Loans

Pros

Personal loans come with fixed interest rates, ensuring monthly payments remain constant throughout the loan term. This stability aids in budgeting and financial planning.

- Flexibility in Use: Unlike balance transfer cards, personal loans can consolidate various types of debt, not limited to credit card debt. This includes medical bills, educational loans, and, in some cases, secured debts.

- Potentially Lower Interest Rates: For individuals with good credit profiles, personal loans can offer lower interest rates than standard credit card rates, leading to potential savings over the loan term.

- Improvement in Credit Score: Consolidating multiple debts into a single personal loan can improve your credit score by reducing your credit utilization ratio and diversifying your credit mix.

- No Collateral Required: Most personal loans are unsecured, meaning they don’t require collateral like a home or car. This can benefit borrowers who do not want to risk their assets.

Cons

- Interest and Fees: Personal loans always accrue interest, unlike some balance transfer cards' introductory 0% APR. Additionally, some loans come with origination fees, which can increase the cost of borrowing.

- Higher Payments Compared to Minimum Credit Card Payments: The fixed monthly payments on a personal loan can be higher than the minimum payments on credit cards, which might strain your monthly budget.

- Potential for Higher Interest Rates with Poor Credit: Individuals with lower credit scores may face higher interest rates on personal loans, making them less cost-effective than other debt consolidation options.

- Impact on Credit Score from Loan Inquiry: Applying for a personal loan involves a hard credit inquiry, which can temporarily lower your credit score.

- Penalties for Early Repayment: Some personal loans come with prepayment penalties, meaning you could be charged a fee for paying off the loan early.

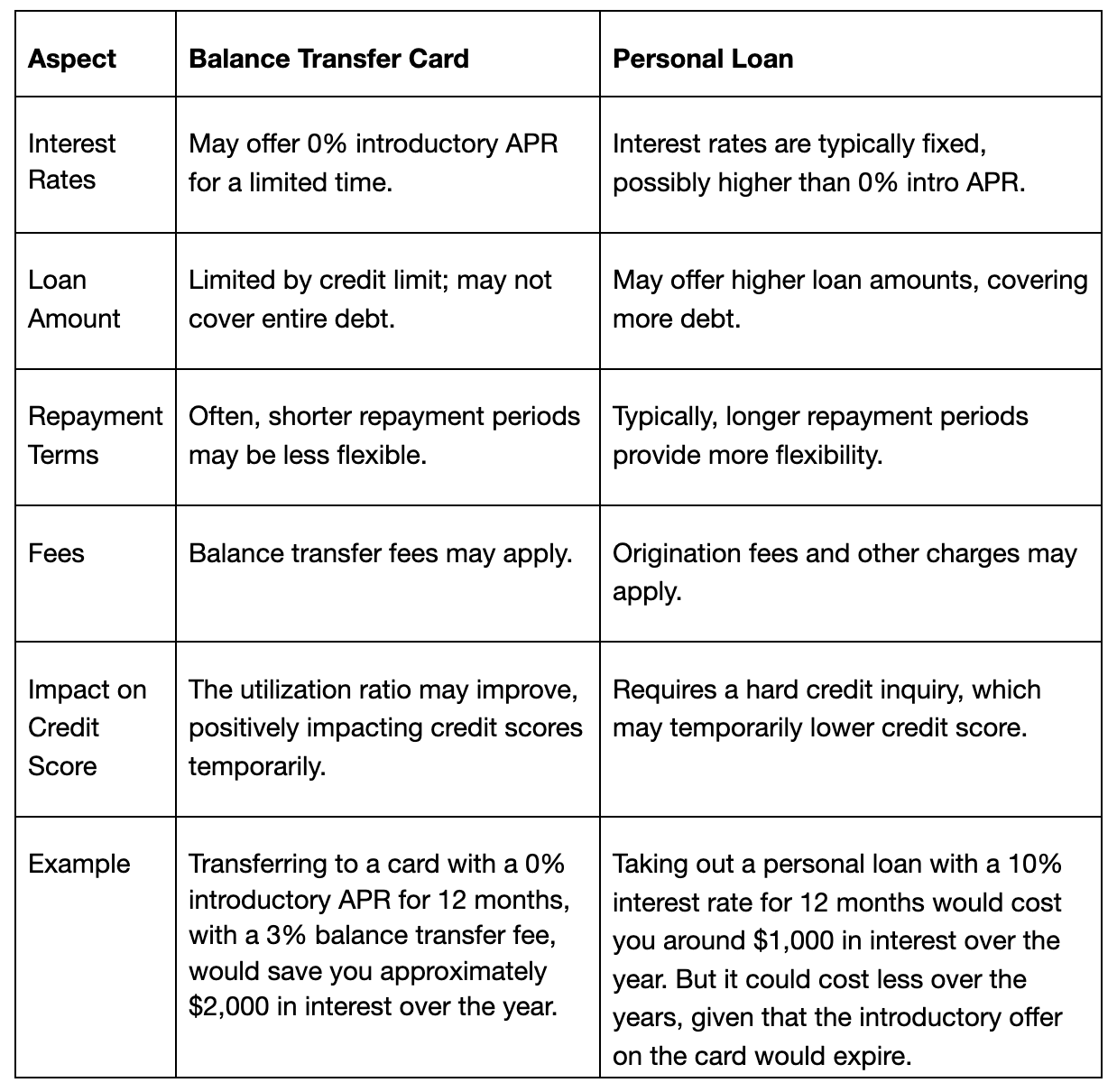

Balance Transfer Cards vs Personal Loan

Let’s look at a comparison table to help you weigh your options.

Additional Considerations

1. Varied Loan Amounts: Personal loans offer a wide range of borrowing options, typically from $1,000 to $50,000 or more, depending on the lender and your creditworthiness.

2. Term Length: Loan terms can vary significantly, from one year to as long as seven years, affecting both the monthly payment amount and the total interest paid.

Impact on Financial Goals

3. Debt Consolidation Efficiency: By consolidating multiple debts into one loan, you can streamline your finances and potentially reduce the total interest paid over time.

Financial Discipline: Fixed repayment terms require consistent monthly payments, encouraging financial discipline and timely debt repayment.

4. Accessibility: Online Lenders and Banks: Personal loans are widely accessible through various financial institutions, including traditional banks, credit unions, and online lenders, each offering different terms and rates.

5. Prequalification Options: Many lenders offer prequalification processes that allow you to check potential rates without impacting your credit score, aiding in comparison shopping.

Personal loans may include an origination fee, a charge for processing the loan. This fee varies by lender and can be a factor in the overall cost of the loan. As with balance transfer cards, taking out a personal loan affects your credit score. Initially, a slight decrease may be due to the hard inquiry on your credit report. However, consistently making on-time payments can positively impact your credit score.

Conclusion

When managing and consolidating debt, both balance transfer cards and personal loans offer viable solutions, each with distinct advantages and considerations. The choice between these two options should be based on your individual financial situation, debt amount, types of debt, credit history, and ability to meet repayment terms.

Therefore, the decision hinges on your financial goals, the nature of your debt, and your personal financial discipline. Balance transfer cards offer a great short-term solution to high-interest debt, especially if you can pay off the balance quickly. On the other hand, personal loans provide a structured path to debt consolidation, often with fixed interest rates, making them suitable for long-term financial planning and diverse debt types.

Start your journey to a debt-free life with Bright Money!

Suggested readings

- How to Liquidate a Credit Card into Cash: What's the Cost?

- What are the Best Debt Consolidation Loans for Bad Credit in 2024?

- How do you secure cash advances with a bad credit score?

FAQ’s

1. Is it better to have a loan balance or a credit card balance?

When considering whether to maintain a loan or a credit card balance, evaluating the interest rates and repayment terms is essential. Personal loans offer lower interest rates than credit cards, making them a more cost-effective option for managing existing debt. This is particularly true for high-interest debts. Additionally, loans usually provide structured repayment plans, which can be more manageable and less volatile on your credit score.

2. What is better, a credit card or personal loan?

Choosing between a credit card and a personal loan depends on your financial situation and goals. Personal loans are generally better for consolidating multiple debts, offering lower interest rates and fixed repayment terms. On the other hand, credit cards, especially balance transfer cards, can be beneficial for paying off your debt faster if you qualify for a promotional 0% interest period.

3. Which is better, a personal loan or debt consolidation?

Deciding between a personal loan and debt consolidation depends on the nature of your debts and your financial strategy. Personal loans can consolidate your debt, offering a single, fixed repayment term and potentially lower interest rates, saving you money on interest over time. This is especially true for those with a good credit history. When applying for debt consolidation, particularly through balance transfer cards, managing high-interest credit card debts can be a good idea.

4. Is a balance transfer of a loan a good idea?

Transferring a loan balance to a balance transfer credit card can be a good idea if it helps reduce the interest rate on your existing debt. This strategy is particularly effective for high-interest credit card debts. By applying for a debt consolidation card with a 0% introductory rate, you can pay off your debt faster and save on interest.

5. Is it better to apply for a debt consolidation loan or manage debts individually?

Applying for a debt consolidation loan can be a strategic move if you have multiple high-interest debts. Consolidation loans typically offer lower interest rates and structured repayment terms, making it easier to manage your finances and potentially saving you money on interest. This can be particularly beneficial for those with a strong credit history. Managing debts individually might be preferable if smaller debts can be paid off quickly or qualify for a balance transfer card with favorable terms.

References

- https://www.investopedia.com/balance-transfer-vs-personal-loan-7501421

- https://www.fool.com/the-ascent/personal-loans/balance-transfer-vs-personal-loan/

- https://www.creditkarma.com/advice/i/balance-transfer-vs-personal-loan

- https://www.lendingtree.com/credit-cards/articles/balance-transfer-vs-personal-loan/

Disclaimer: Bright credit is a line of credit that can be used to pay off your credit cards. Subject to credit approval. Variable APR ranges from 9% to 24.99%, and credit limit ranges from $500 - $8,000. Apr will vary based on prime rates. Final terms may vary depending on credit review. Monthly minimum payments are as low as 3% of the outstanding principal balance plus the accrued interest. Also, you can pay more than the minimum due if you want to repay the loan faster. Credit line originated by bright or CBW Bank, member FDIC. Products and services are subject to state residency and regulatory requirements. Bright credit is currently not available in all states