You are now leaving the Bright website and entering a third-party website. Bright has no control over the content, products, or services offered, nor the security or privacy of information transmitted to others via their website. We recommend that you review the privacy policy of the site you are entering. Bright does not guarantee or endorse the products, information, or recommendations provided on any third-party website.

Managing debt is an important task that often determines one's financial health and stability. Among the various strategies available for debt management, two stand out for their effectiveness and widespread use are - Debt consolidation loans and Balance transfer credit cards.

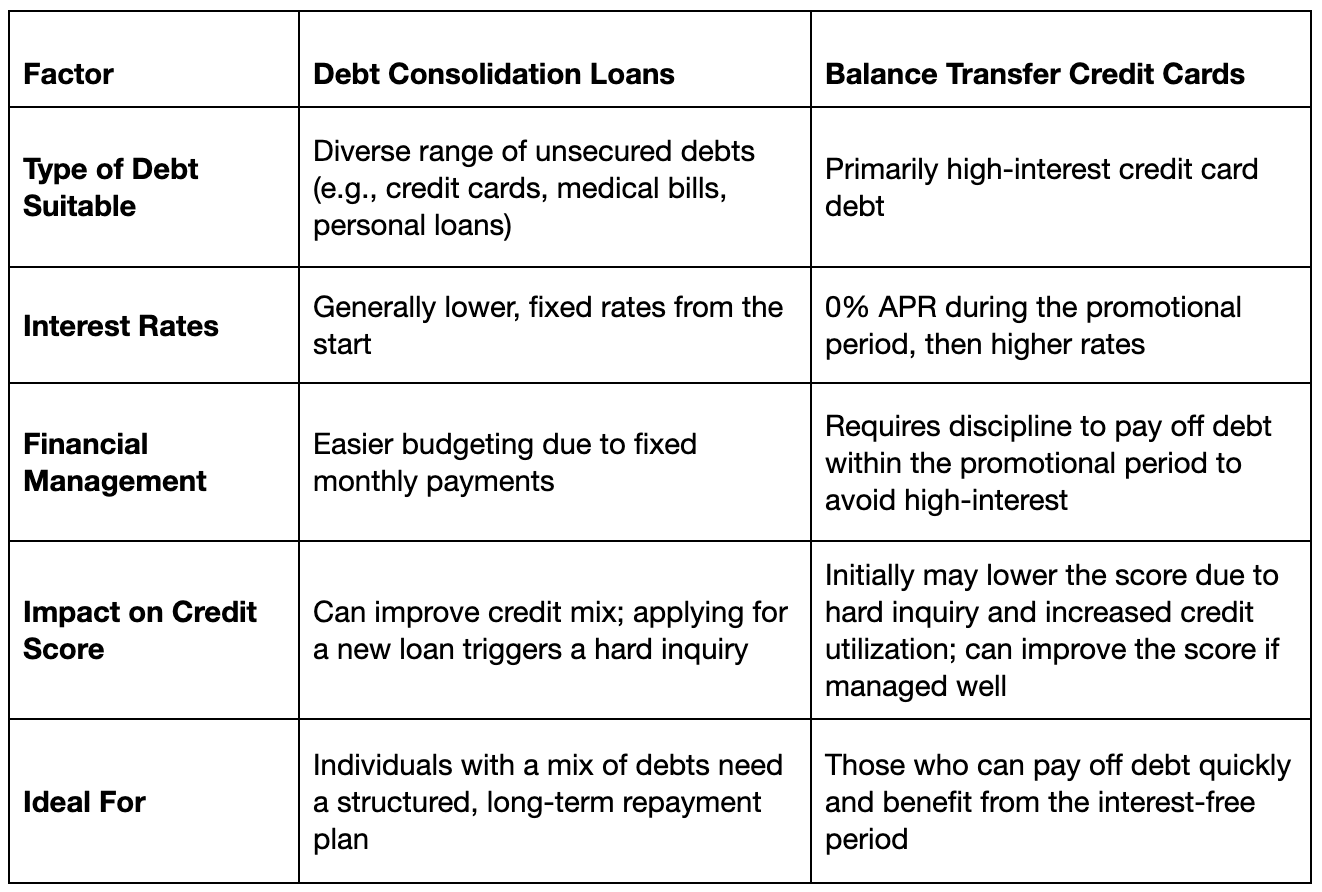

Debt consolidation loan vs. balance transfer credit card

When tackling debt, it is important to choose between a debt consolidation loan and a balance transfer credit card. A debt consolidation loan combines multiple debts into one, often with a lower interest rate, simplifying repayments and potentially reducing the cost over time.

On the other hand, a balance transfer credit card allows you to transfer existing debts to a card with a low introductory interest rate, offering a chance to reduce the debt without accruing high interest.

Understanding Debt Consolidation Loans

Debt consolidation loans are designed to simplify the repayment of multiple debts. Individuals can combine various debts into a single loan by applying for a debt consolidation loan. This approach streamlines the repayment process and can potentially lower the overall interest rate.

Key Features of Debt Consolidation Loans:

- Single Monthly Payment: Instead of managing multiple debts with varying interest rates and due dates, a debt consolidation loan consolidates your debt, requiring just one monthly payment.

- Fixed Interest Rates: These loans typically come with fixed interest rates, meaning the rate remains constant throughout the loan term.

- Varied Repayment Terms: The terms of debt consolidation loans can range from a few years to several, offering flexibility in how quickly the debt can be paid off.

- Impact on Credit Score: Consolidating debt can initially lead to a slight dip in your credit score due to the hard inquiry required during the loan application process. However, successfully managing and paying off the loan can positively affect your credit profile.

Pros and Cons of Debt Consolidation Loans

Pros

- Simplified Debt Management: By consolidating multiple debts into one loan, you reduce the complexity of managing several accounts, making it easier to focus on a single repayment plan.

- Fixed Interest Rates: The stability of a fixed interest rate means your monthly payments remain constant, aiding in reliable budget planning.

- Potential for Lower Overall Interest: If the consolidated interest rate is lower than the average rate of your existing debts, especially high-interest credit card debts, you could save a significant amount on interest over time.

- Improvement in Credit Utilization: Consolidating multiple credit card balances into one loan can lower your credit utilization ratio, positively impacting your credit score.

Cons

- Interest and Fees: While you might secure a lower interest rate than credit cards, the loan will always accrue interest, unlike a 0% APR balance transfer card. Additionally, some loans come with origination fees.

- Risk of Collateral: Some debt consolidation loans, especially those with lower interest rates, may be secured loans requiring collateral like a home or car.

- Potential for Higher Long-Term Cost: If the loan term is extended, you might pay more consolidation every time despite the lower monthly payments.

When To Use Debt Consolidation Loans?

Debt management is a nuanced concept unique to each person's situation. There are times when debt consolidation is the perfect option, and there might be situations where it would be more beneficial to explore other options. So, when should you consider debt consolidation loans?

- Multiple High-Interest Debts: If you have multiple debts with high interest rates, consolidating them into a single loan with a lower interest rate can save you money in the long run.

- Simplify Payments: If you find it challenging to keep track of multiple debt payments, consolidating them into a single monthly payment can make managing your finances easier.

- Improved Credit Score: Debt consolidation can help improve your credit score by reducing your credit utilization ratio and demonstrating responsible debt management.

- Avoid Bankruptcy: Debt consolidation can be an alternative to bankruptcy for individuals struggling with debt, offering a way to repay debts without the severe consequences of bankruptcy.

Top 5 Debt Consolidation Loans

- Avant: Offers debt consolidation loans with APRs ranging from 9.95% to 35.99% and loan amounts up to $35,000 for qualifying borrowers.

- Upgrade: Provides personal loans for debt consolidation with APRs starting at 5.94% and loan amounts up to $50,000 for eligible borrowers.

- Discover: Offers debt consolidation loans with fixed APRs starting at 6.99% and loan amounts up to $35,000 for qualified borrowers.

- Marcus by Goldman Sachs: Provides debt consolidation loans with fixed APRs starting at 6.99% and loan amounts up to $40,000 for eligible borrowers.

- Bright Money: Offers innovative solutions for debt consolidation, including Bright Credit and Bright Builder, tailored to help you manage and consolidate your debts effectively.

Exploring Balance Transfer Credit Cards

Balance transfer (link) credit cards offer an alternative method for managing debt, particularly credit card debt. These cards allow individuals to transfer existing debt from one or more credit cards to a new card, typically featuring a 0% APR promotional period.

Key Features of Balance Transfer Credit Cards:

- Introductory 0% APR: Many balance transfer cards offer an introductory period, usually 12 to 21 months, during which no interest is accrued on the transferred balance.

- Balance Transfer Fees: While these cards can save you money on interest, they often come with a balance transfer fee (link), typically around 3% to 5% of the transferred amount.

- Credit Requirements: A good to excellent credit score is generally required to qualify for a balance transfer card with favorable terms. The credit limit granted also plays a crucial role in determining how much debt you can transfer.

- Post-Promotional Rates: Once the introductory period ends, the interest rate on the remaining balance typically reverts to a higher standard rate. This factor is crucial, as it can affect the cost-effectiveness of transferring your balance.

Pros and Cons of Balance Transfer Credit Cards

If used wisely, these cards can also positively impact your credit score. Paying down balances quickly during the 0% APR period and not accruing additional debt is key to this positive outcome.

Pros

- Simplified Debt Management: By consolidating multiple debts into one loan, you reduce the complexity of managing several accounts, making it easier to focus on a single repayment plan.

- Fixed Interest Rates: The stability of a fixed interest rate means your monthly payments remain constant, aiding in reliable budget planning.

- Potential for Lower Overall Interest: If the consolidated interest rate is lower than the average rate of your existing debts, especially high-interest credit card debts, you could save a significant amount on interest over time.

- Improvement in Credit Utilization: Consolidating multiple credit card balances into one loan can lower your credit utilization ratio, positively impacting your credit score.

Cons

- Interest and Fees: While you might secure a lower interest rate than credit cards, the loan will always accrue interest, unlike a 0% APR balance transfer card. Additionally, some loans come with origination fees.

- Risk of Collateral: Some debt consolidation loans, especially those with lower interest rates, may be secured loans requiring collateral like a home or car.

- Potential for Higher Long-Term Cost: If the loan term is extended, you might pay more in total interest over time despite the lower monthly payments.

When To Use Balance Transfer?

Let's take a look at situations where balance transfers are the ideal option to manage debt.

- High-Interest Debt: If you have high-interest credit card debt, a balance transfer card with a promotional 0% APR period can help you save on interest payments.

- Consolidating Debt: If you have multiple high-interest debts, consolidating them onto a balance transfer card can simplify your payments.

- Improving Credit Score: Transferring balances to a new card can lower your credit utilization ratio, positively impacting your credit score.

Top 5 Balance Transfer Cards To Consider

- Citi® Diamond Preferred® Card: Offers an introductory 0% APR on balance transfers for 21 months, with a 3% balance transfer fee.

- Discover it® Balance Transfer: Provides an introductory 0% APR on balance transfers for 18 months, with a 3% balance transfer fee.

- Chase Freedom Unlimited®: Offers an introductory 0% APR on balance transfers for 15 months, with a 5% balance transfer fee.

- U.S. Bank Visa® Platinum Card: Provides an introductory 0% APR on balance transfers for 20 billing cycles, with a 3% balance transfer fee.

- Wells Fargo Reflect℠ Card: Offers an introductory 0% APR on balance transfers for 18 months, with a 3% balance transfer fee.

Comparative Analysis: Loans Vs. Credit Cards

Conclusion

Choosing between a debt consolidation loan and a balance transfer credit card depends on individual financial circumstances and goals. A debt consolidation loan is typically best suited for those seeking a structured repayment plan and a potentially lower overall interest rate, especially if they have a good credit history.

On the other hand, a balance transfer credit card might be more advantageous for those who can pay off their debt within the introductory low-interest period, thus saving significantly on interest charges. When making this decision, it's important to consider factors such as the total amount of debt, credit score, financial discipline, and long-term financial plans. Ultimately, both strategies, when used responsibly, can be effective tools in managing and reducing debt.

Ready to build your credit with ease? Try Bright Builder today and enjoy the benefits of on-time payments with a 0% APR. No interest fees, no hard credit pull, and a simple way to improve your credit score. Apply now and take the first step towards a brighter financial future!"

Read More:

- What are the Best Debt Consolidation Loans for Bad Credit in 2024?

- How to Liquidate a Credit Card into Cash: What's the Cost?

- Debt Consolidation Loan vs. Balance Transfer Credit Card: Which is Right for You?

FAQs

- Is Debt Consolidation the Same as a Balance Transfer Credit Card?

While both strategies aim to manage multiple debts, they are not the same. Applying for a debt consolidation loan involves taking out a new loan to pay off your existing debt. This can be a good idea if you're dealing with high-interest debts, as consolidation loans often have lower interest rates and more favorable repayment terms. On the other hand, a balance transfer credit card allows you to transfer the balances of your other credit cards to one card, typically with a lower interest rate.

- Is it better to have a credit card balance or a loan for debt consolidation?

Deciding between a balance transfer credit card and a debt consolidation loan depends on your financial situation and credit profile. It might be a better option if you have a good credit history and can qualify for a debt consolidation loan with favorable terms. Consolidation loans often offer lower interest rates than credit cards, saving you money on interest in the long run.

- Is Debt Consolidation the Same as Credit Card Debt?

Debt consolidation is a method for managing credit card debt, among other types of debt. When you consolidate your debt, you combine multiple debts, which may include credit card balances, into a single loan. This consolidated loan often has a lower interest rate than the average rate of your existing debts, especially if they include high-interest credit card debts.

- What is the Difference Between Debt Consolidation and Balance Transfer?

The main difference lies in the approach and the type of product used. Debt consolidation involves taking out a new loan (often a secured loan) to pay off multiple debts. This can be a good idea if you're looking for structured repayment terms and potentially lower interest rates. In contrast, a balance transfer involves moving your existing debt, usually from high-interest credit cards, to a new credit card with a lower interest rate.

- Can I Get a Debt Consolidation Loan with Bad Credit?

Qualifying for a debt consolidation loan with bad credit can be challenging but not impossible. Lenders typically consider your credit history and profile when deciding on your loan application. A lower credit score might mean higher interest rates or less favorable terms, affecting the overall benefit of consolidating your debts.

References

- https://www.forbes.com/advisor/personal-loans/debt-consolidation-loan-vs-balance-transfer/

- https://www.bankrate.com/personal-finance/debt/balance-transfer-credit-card-vs-personal-loan/

- https://www.smfgindiacredit.com/knowledge-center/debt-consolidation-vs-balance-transfer.aspx

Disclaimer: Bright credit is a line of credit that can be used to pay off your credit cards. Subject to credit approval. Variable APR ranges from 9% –24.99%, and credit limits range from $500 - $8,000. Apr will vary based on prime rates. Final terms may vary depending on credit review. Monthly minimum payments are as low as 3% of the outstanding principal balance plus the accrued interest. Also, you can pay more than the minimum due if you want to pay down the loan faster. The credit line originated from Bright or CBW Bank, a member of FDIC. Products and services subject to state residency and regulatory requirements. Bright credit is currently not available in all states.