You are now leaving the Bright website and entering a third-party website. Bright has no control over the content, products, or services offered, nor the security or privacy of information transmitted to others via their website. We recommend that you review the privacy policy of the site you are entering. Bright does not guarantee or endorse the products, information, or recommendations provided on any third-party website.

Did you know that, according to a report, as of September 2021, the average Credit Card interest rate in the United States was around 15%? Debt may be a major burden on your financial health, leading to stress and preventing you from achieving your financial objectives. Finding efficient ways to pay it off fast is essential whether you have Credit Card Debt, school loans, a mortgage, or any other kind of Debt. Using a lump sum payment is one effective way to speed up your Debt repayment.

But before we get into the topic, it is recommended first to read about 14 Debt Pay-off Tips You Can't Miss in detail by Bright Money!

This in-depth article will explain what a lump sum payment is, how it functions, and the measures you can take to use it to pay off Debt quickly.

Understanding Lump Sum Payments

A lump sum payment is a substantial, one-time payment made toward a specific financial goal, such as paying off Debt. Unlike regular monthly payments, which are typically fixed and scheduled, lump sum payments offer the advantage of a significant infusion of cash that can significantly reduce your Debt balance.

How to pay off Debt Fast using a Lump Sum Payment?

To pay off your Debt quickly using a lump sum payment, allocate a substantial amount of money, such as a tax refund or a work bonus, toward your highest-interest Debt to reduce the principal balance significantly and minimize interest costs.

Example:

Suppose you have two Debts:

Credit Card Debt: You owe $5,000 on a Credit Card with a high-interest rate of 18% APR.

Personal Loan: You have a personal finance loan with a balance of $8,000 and a lower interest rate of 8% APR.

Now, let's say you receive a tax refund of $2,500. To pay off Debt quickly using a lump sum payment, you decide to allocate this lump sum toward your highest-interest Debt, which is the Credit Card Debt.

Before Lump Sum Payment:

Credit Card Debt: $5,000 with an 18% APR.

Personal Loan: $8,000 with an 8% APR.

After Lump Sum Payment:

Credit Card Debt: $2,500 ($5,000 - $2,500) with an 18% APR.

Personal Loan: $8,000 with an 8% APR.

By applying the lump sum payment to your Credit Card Debt, you've significantly reduced the principal balance of that Debt. This not only lowers your overall Debt but also minimizes the interest costs you'll incur over time. With a smaller balance on the Credit Card, you can pay off the remaining Debt more quickly and save money on interest.

Don't Let Debt Hold You Back. Join Bright Money Now and Refinance Your Credit Card Debt for a Brighter Financial Future.

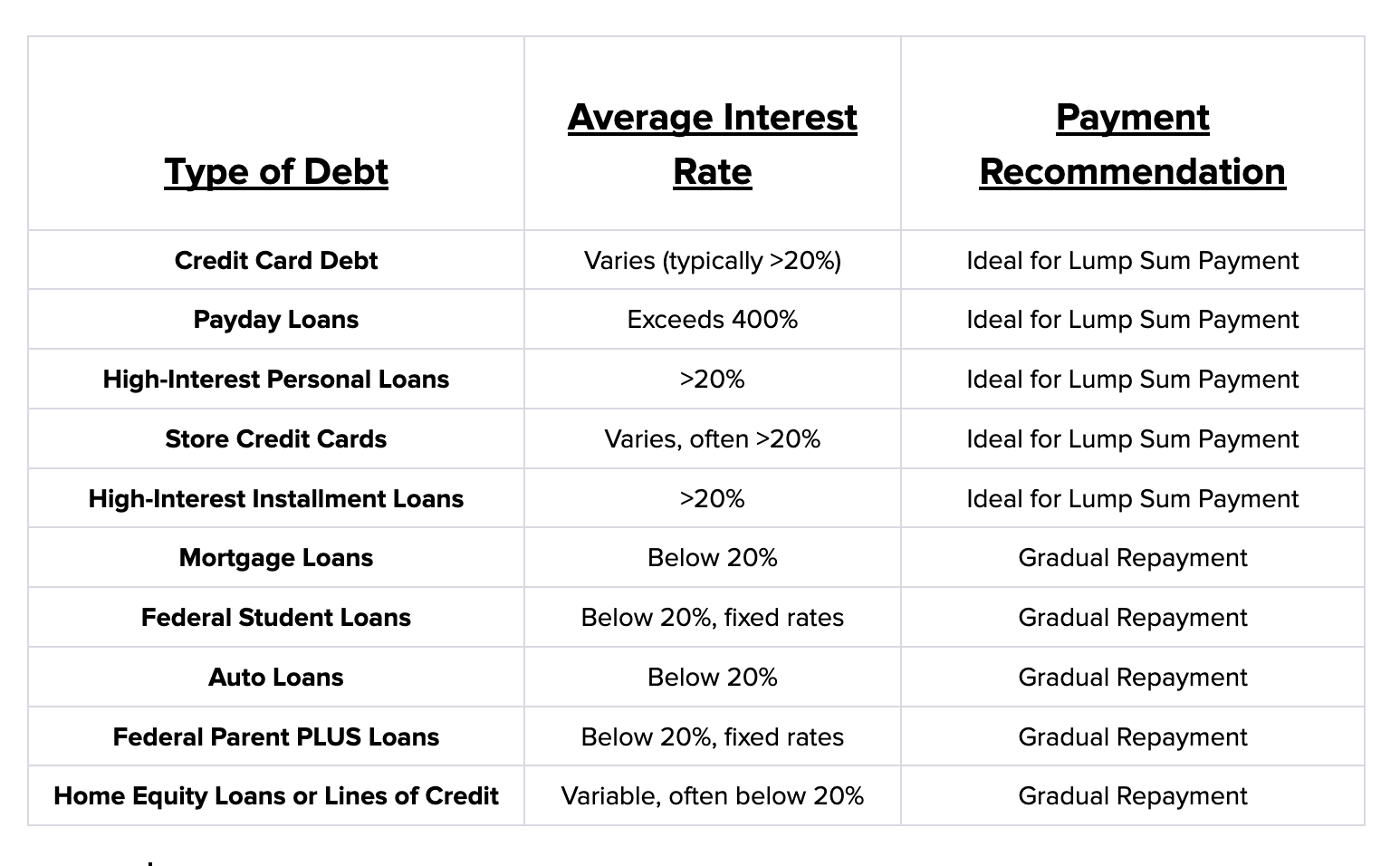

Which Debts should be paid in Lump Sum?

Debts that should be paid off with lump sum payments are typically high-interest Debts with APRs exceeding 15%. These may include:

- Credit Card Debt: Credit Cards often have high interest rates, making them a priority for lump sum payments

- Payday Loans: These short-term loans come with extremely high APRs and should be paid off as soon as possible

- Certain Personal Loans: Some personal loans, particularly those from alternative lenders, can have very high APRs and should be targeted with lump sum payments

- Predatory Loans: Any loans with excessively high-interest rates, such as certain car loans or loans from lenders with predatory practices

Disclaimer: Information on brightmoney.co is for informational purposes; we do not guarantee its accuracy or update frequency. Verify independently and seek professional advice for financial decisions. When considering the use of a lump sum payment to accelerate your Debt repayment, it's crucial to select the right types of Debt to target. Some Debts are more suitable for this strategy due to factors like interest rates, terms, and the potential for significant savings. Here are the types of Debt ideal for lump sum payments:

All High-Interest Debts ideal for Lump Sum (High-Interest > 20% APR):

1. Credit Card Debt

Credit Card Debt is a prime example of high-interest Debt, often carrying APRs well above 20%. These high rates make Credit Card balances particularly costly over time. Here's why lump sum payments are crucial for Credit Card Debt:

- Rapid Interest Accumulation: Credit Cards accumulate interest daily, and when you only make minimum monthly payments, a significant portion goes toward interest, leaving your principal balance relatively untouched. A lump sum payment directly reduces the principal, effectively saving you from future interest on that amount

- Snowball Effect: Reducing or eliminating a Credit Card balance with a lump sum payment can kickstart a Debt reduction "snowball effect." As you pay off one card, you can redirect the money you were paying on that card to tackle other Debts

2. Payday Loans

Payday loans are infamous for their astronomical APRs, often exceeding 400%. They are designed as short-term solutions but can quickly lead to long term financial trouble. Here's why lump sum payments are crucial for payday loans:

- Escape Exorbitant Interest: The interest on payday loans can quickly spiral out of control, making it nearly impossible to pay down Debt through regular payments. A lump sum payment allows you to clear the Debt without incurring astronomical interest charges

- Breaking the Debt Cycle: Payday loans often trap borrowers in a cycle of borrowing to cover previous loans. A lump sum payment breaks this cycle, providing a chance for financial recovery

3. Personal Loans with High APRs

Certain personal loans, particularly those from alternative or online lenders, can have APRs exceeding 20%. These loans often have more flexible qualification criteria but come with higher costs. Here's why lump sum payments are essential for such loans:

- Interest Savings: High APRs on personal loans can result in significant interest costs over time. A lump sum payment reduces the principal and lowers the overall interest paid

- Faster Debt Repayment: Paying off a personal loan with a lump sum accelerates your journey to Debt freedom, freeing up your finances for other goals

4. Store Credit Cards

Store Credit Cards are known for their higher interest rates compared to traditional Credit Cards. If you have outstanding balances on store cards with APRs over 20%, consider lump sum payments for the following reasons:

- Reducing Interest Costs: Paying off store card Debt with a lump sum lowers your interest costs, freeing up your budget for other financial priorities

- Simplify Your Finances: Consolidating and paying off high-interest store card Debt can simplify your financial situation and make it easier to manage your remaining Debts

5. High-Interest Installment Loans

Certain installment loans, like those offered by online lenders or "buy now, pay later" services, can have high APRs. Here's why lump sum payments are advantageous for these loans:

- Interest Reduction: Lump sum payments directly reduce the principal balance, lowering the total interest paid over the life of the loan

- Faster Debt Elimination: By paying off high-interest installment loans more quickly, you regain financial flexibility sooner and can allocate resources to other financial goals

Don't Let Debt Hold You Back. Join Bright Money Now and Refinance Your Credit Card Debt for a Brighter Financial Future.

All Low-Interest Debts should be paid slowly (Low-Interest < 20% APR):

1. Mortgage Loans

- Interest Rates Below 20%: Mortgage loans usually come with relatively low interest rates compared to other types of Debt, often well below 20%. These rates can be in the range of 3% to 5% or even lower

- Reason for Gradual Repayment: Mortgage loans are substantial, long-term commitments, often lasting 15 to 30 years. The low interest rates, coupled with the lengthy loan term, make it more cost-effective to pay them off gradually. Moreover, mortgage interest payments may offer tax deductions in some cases, providing additional financial benefits

2. Federal Student Loans

- Low Fixed Interest Rates: Federal student loans typically feature fixed interest rates that are competitive and lower than 20%. These rates are set by the government and are often more favorable than private student loans

- Flexible Repayment Options: Federal student loans offer various repayment plans, including income-driven repayment, which allows borrowers to align their monthly payments with their income levels. Some borrowers may also qualify for loan forgiveness programs after a certain number of on-time payments

3. Auto Loans

- Competitive Interest Rates: Auto loans generally come with interest rates that are lower than those of Credit Cards or personal loans. Rates can vary, but they are often below 10% or even lower for new cars

- Reasonable Loan Terms: Auto loans typically have shorter terms compared to mortgages, often spanning 3 to 5 years. Given the lower interest rates and shorter loan duration, it makes sense to pay them off gradually while ensuring regular, manageable payments

4. Federal Parent PLUS Loans

- Lower Rates than Private Loans: Federal Parent PLUS loans usually have lower interest rates than many private student loans, often below 10%. These loans are designed to be more affordable for parents funding their children's education

- Flexible Repayment Plans: Parents have access to various federal loan repayment plans, making it easier to manage and budget for loan payments over time

5. Home Equity Loans or Lines of Credit

- Variable but Often Competitive Rates: Home equity loans and lines of credit may have variable interest rates, but they can still be competitive and lower than 20%. Rates can vary based on market conditions

- Utilize Equity for Other Purposes: Many homeowners use these loans to finance home improvements or other major expenses. Gradual repayment allows homeowners to access their home equity while making manageable payments

Why Lump Sum payments are effective?

Lump sum payments are highly effective for paying off Debt quickly for several reasons:

- Interest Reduction: One of the primary benefits of using a lump sum payment is the immediate reduction in interest costs. Since interest accumulates over time, reducing your principal balance means you'll pay less in interest over the life of the loan

- Faster Debt Elimination: A lump sum payment can significantly reduce your Debt balance, allowing you to pay off the remaining amount more quickly. This can help you achieve Debt freedom years ahead of schedule

- Psychological Boost: Making a large lump sum payment can provide a psychological boost, motivating you to continue your Debt repayment journey with renewed determination

- Boosted Credit Score: Reducing your Debt balance can boost your Credit Score, thus making it easier to secure favorable terms on future loans and financial transactions

- Financial Freedom: Once you've paid off your Debt, you'll have more disposable income to allocate toward savings, investments, and other financial goals, ultimately increasing your financial freedom

Don't Let Debt Hold You Back. Join Bright Money Now and Refinance Your Credit Card Debt for a Brighter Financial Future.

Creating a Lump Sum Payment Strategy

Once you've identified potential sources of lump sum payments and assessed your Debt situation, the next critical step is to create a comprehensive strategy for effectively utilizing these funds to pay off Debt faster. A well-thought-out plan can maximize the impact of your lump sum payment and help you achieve your financial goals. Here's a detailed guide on creating a lump sum payment strategy:

1. Prioritize Your Debts

Why it's important: Not all Debts are created equal. To make the most of your lump sum payment, prioritize which Debts to pay off first. Typically, you should focus on high-interest Debts to reduce overall interest expenses.

How to prioritize:

- List your Debts: Make a note of every Debt you have left to pay, including Credit Card balances, personal loans, school loans, mortgages, vehicle loans, and any other commitments

- Determine interest rates: Identify the interest rates associated with each Debt. List them in descending order, with the highest interest rate at the top

- Minimum payments: Note the minimum monthly payments required for each Debt

- Total outstanding balance: Calculate the total outstanding balance for each Debt

- Prioritization: Based on the interest rates and total balances, prioritize which Debts to target first. High-interest Debts should take precedence

Example:

Credit Card A: $5,000 balance, 18% APR

Credit Card B: $3,000 balance, 24% APR

Personal Loan: $7,000 balance, 10% APR

Mortgage: $200,000 balance, 4% APR

In this example, you should prioritize paying off Credit Card B first, as it has the highest interest rate.

2. Review Your Budget

Why it's important: Understanding your current financial situation is crucial for determining how much of your lump sum payment you can allocate towards Debt repayment without jeopardizing your daily living expenses.

How to review your budget:

- Gather financial information: Collect details about your monthly income, expenses, and existing Debt payments

- Create a budget: Develop a comprehensive budget that includes all your income sources and monthly expenses, like rent or mortgage, utilities, groceries, transportation, insurance, and discretionary spending

- Identify discretionary spending: Look for areas where you can cut back on discretionary spending to free up more money for Debt repayment

- Calculate your Debt-to-income ratio: Determine the percentage of your income currently allocated to Debt payments

Example:

Suppose your monthly income is $4,000, and your monthly expenses total $3,000, leaving you with $1,000 in discretionary income. If your minimum Debt payments are $500, your Debt-to-income ratio is 12.5% ($500 ÷ $4,000).

3. Determine the Amount to Allocate

Why it's important: Deciding how much of your lump sum payment to allocate to Debt repayment requires balancing your financial goals, emergency fund needs, and other financial obligations.

How to determine the allocation:

- Assess your financial goals: Consider your short-term and long-term financial goals. Are there other financial priorities, such as building an emergency fund or saving for retirement?

- Emergency fund: Ensure you have an adequate emergency fund to cover unexpected expenses, typically three to six months' worth of living expenses

- Allocate a portion: Determine what percentage of your lump sum payment you're comfortable allocating to Debt repayment while still addressing other financial needs

Example:

Suppose you receive a lump sum payment of $5,000. If your financial goals include both paying off Debt and building an emergency fund, you might decide to allocate $3,000 to Debt repayment and reserve $2,000 for your emergency fund.

4. Execute Your Plan

Why it's important: Execution is the key to success. Once you've created a plan, take action to apply your lump sum payment to your targeted Debts.

How to execute your plan:

- Contact your creditors: Confirm the procedure for sending a lump sum payment by getting in touch with your creditors. They could have precise guidelines or demands

- Make payments: Use your lump sum payment to make additional payments on the prioritized Debts, starting with the highest-interest Debt first

- Document transactions: Keep records of your lump sum payments, including dates, amounts, and confirmation receipts from creditors

- Monitor progress: Regularly check your Debt balances to track your progress. Celebrate milestones as you pay off individual Debts or reach specific reduction targets

5. Adjust Your Budget as Needed

Why it's important: As you execute your lump sum payment plan, you may need to make adjustments in order to your budget to accommodate changes in your financial situation.

How to adjust your budget:

- Reassess expenses: Periodically review your budget to identify areas where you can cut back further to allocate more funds to Debt repayment

- Windfalls or extra income: If you receive additional income, such as bonuses or overtime pay, consider applying these windfalls to Debt repayment to accelerate your progress

- Modify your goals: Reevaluate your financial goals as you make progress. You may decide to allocate more or less of your lump sum payment based on your evolving financial priorities

Example:

If you receive an unexpected bonus of $1,000, you can adjust your budget to allocate this windfall entirely to Debt repayment, further reducing your Debt balances.

Conclusion

According to a study, consumers who paid off their accounts one by one paid down their Debt 15% faster than those who made their Debt payments in equal amounts. Paying off Debt quickly using a lump sum payment is a powerful strategy that can provide financial freedom and peace of mind. By understanding the benefits of lump sum payments, acquiring the necessary funds, creating a Debt payoff plan, and staying disciplined in your approach, you can take significant strides toward becoming Debt-free.

Remember that every financial situation is unique, so it's essential to tailor your Debt repayment strategy to your specific circumstances and goals. With determination and a clear plan, you can take over the control of your finances and achieve a Debt-free future.

Don't Let Debt Hold You Back. Join Bright Money Now and Refinance Your Credit Card Debt for a Brighter Financial Future.

Suggested Readings:

What is a Good Credit Score to Buy a House?

Top 10 Apps to Get Instant Cash!

FAQs

- What is a lump sum payment for Debt?

A lump sum payment for Debt is a one-time, significant payment made toward your outstanding Debts, typically more substantial than your regular monthly payments.

- Why should I consider making a lump sum payment to pay off Debt?

Making a lump sum payment can significantly reduce your Debt balance, lower interest costs, and expedite your journey to becoming Debt-free.

- What types of Debts can I pay off with a lump sum payment?

You can use a lump sum payment to pay off various types of Debts, like Credit Card Debt, student loans, personal loans, auto loans, and even your mortgage.

- How can I acquire a lump sum for Debt repayment?

You can obtain a lump sum by leveraging windfalls, like bonuses or tax refunds, using savings, liquidating assets, pursuing side hustles, borrowing from retirement accounts (with caution), negotiating settlements, or receiving gifts or loans from family or friends.

- Is it better to use a lump sum payment to pay off high-interest Debt or low-interest Debt first?

It's generally more financially beneficial to use a lump sum payment in order to pay off high-interest Debt first. This approach minimizes the total interest paid over time.

- What is the difference between the snowball and avalanche methods of Debt repayment?

The snowball method includes paying off the smallest Debt first, while the avalanche method prioritizes the Debt with the highest interest rate. The snowball method provides quick wins for motivation, while the avalanche method saves more money on interest in the long run.

- Are there any tax implications to consider when using a lump sum payment for Debt repayment?

In most cases, there are no direct tax implications for using a lump sum payment to pay off Debt. However, if you're using retirement account funds, consult a tax advisor to understand potential tax consequences.

- Will making a lump sum payment negatively affect my Credit Score?

Making a lump sum payment should generally boost your Credit Score as it reduces your Debt-to-credit ratio. However, if you negotiate a settlement with a creditor, it might have a temporary negative effect on your credit.

- Can I use multiple lump sum payments to pay off Debt faster?

Yes, you can make multiple lump sum payments over time to accelerate your Debt repayment even further. It's a flexible strategy that allows you to use windfalls or other financial opportunities as they arise.

- What should I do after making a lump sum payment to pay off Debt?

After making a lump sum payment, consider adjusting your budget to allocate the freed-up money towards other financial goals, like investing, building an emergency fund, or saving for retirement.

- Can I use a lump sum payment to negotiate with creditors for Debt settlement?

Yes, you can use a lump sum payment to negotiate with creditors for Debt settlement. Offering a lump sum payment to settle your Debt for less than the full amount owed can be a strategic way to reduce your Debt burden.

- Are there any penalties or fees for making a lump sum payment on my loans or Credit Cards?

Typically, there are no penalties or fees for making a lump sum payment on loans or Credit Cards. However, it's advisable to check your loan or Credit Card terms and conditions to confirm this, as some lenders may have specific policies.

- Should I prioritize an emergency fund or making a lump sum payment on my Debt?

It's generally recommended to prioritize building an emergency fund before making a lump sum payment on Debt. Having an emergency fund provides a financial safety net to cover unexpected expenses and prevents you from potentially taking on more Debt in emergencies.

- Can I use a lump sum payment to pay off a portion of my mortgage or only the entire balance?

You can use a lump sum payment to pay off a portion of your mortgage or the entire balance, depending on your financial goals. Some homeowners make extra payments toward the principal to reduce the overall interest paid over the life of the loan.

- Is there a minimum lump sum payment amount that I should consider when paying off my Debts?

The minimum lump sum payment amount depends on your specific Debt obligations and financial situation. It's essential to assess your budget, prioritize high-interest Debts, and allocate a lump sum that aligns with your financial goals and ability to maintain financial stability.

References:

https://www.nerdwallet.com/article/credit-cards/what-is-the-average-credit-card-interest-rate

https://www.forbes.com/advisor/credit-cards/credit-card-payoff-strategies/