You are now leaving the Bright website and entering a third-party website. Bright has no control over the content, products, or services offered, nor the security or privacy of information transmitted to others via their website. We recommend that you review the privacy policy of the site you are entering. Bright does not guarantee or endorse the products, information, or recommendations provided on any third-party website.

Congratulations! You are already demonstrating wisdom beyond your years by considering the importance of building credit at the age of 18. While many may overlook the significance of establishing credit early on, you understand that this is a crucial step towards achieving financial independence and securing a bright future. Your proactive approach to learning how to build credit at such a young age sets you on a path of empowerment and opens doors to a world of opportunities.

A good credit score is crucial for achieving financial independence and securing favorable loan terms and interest rates. However, as an 18-year-old, you likely have minimal or no credit history, making it challenging to qualify for loans or rental agreements without a cosigner. To overcome this hurdle and establish a solid credit foundation, learning how to build credit at 18 is essential.

In this comprehensive guide, we will provide you with practical tips to help you on your journey to build credit fast.

Read more: 8 reasons why your credit score is important

Why Build Credit at 18?

Building credit at 18 is crucial because it establishes a strong financial foundation for the future. Early credit history enables access to better interest rates and higher credit limits, essential for purchasing a car, renting an apartment, or obtaining loans later in life. Responsible credit management at a young age also cultivates good financial habits, fostering responsible spending and saving practices that will benefit individuals throughout their lives.

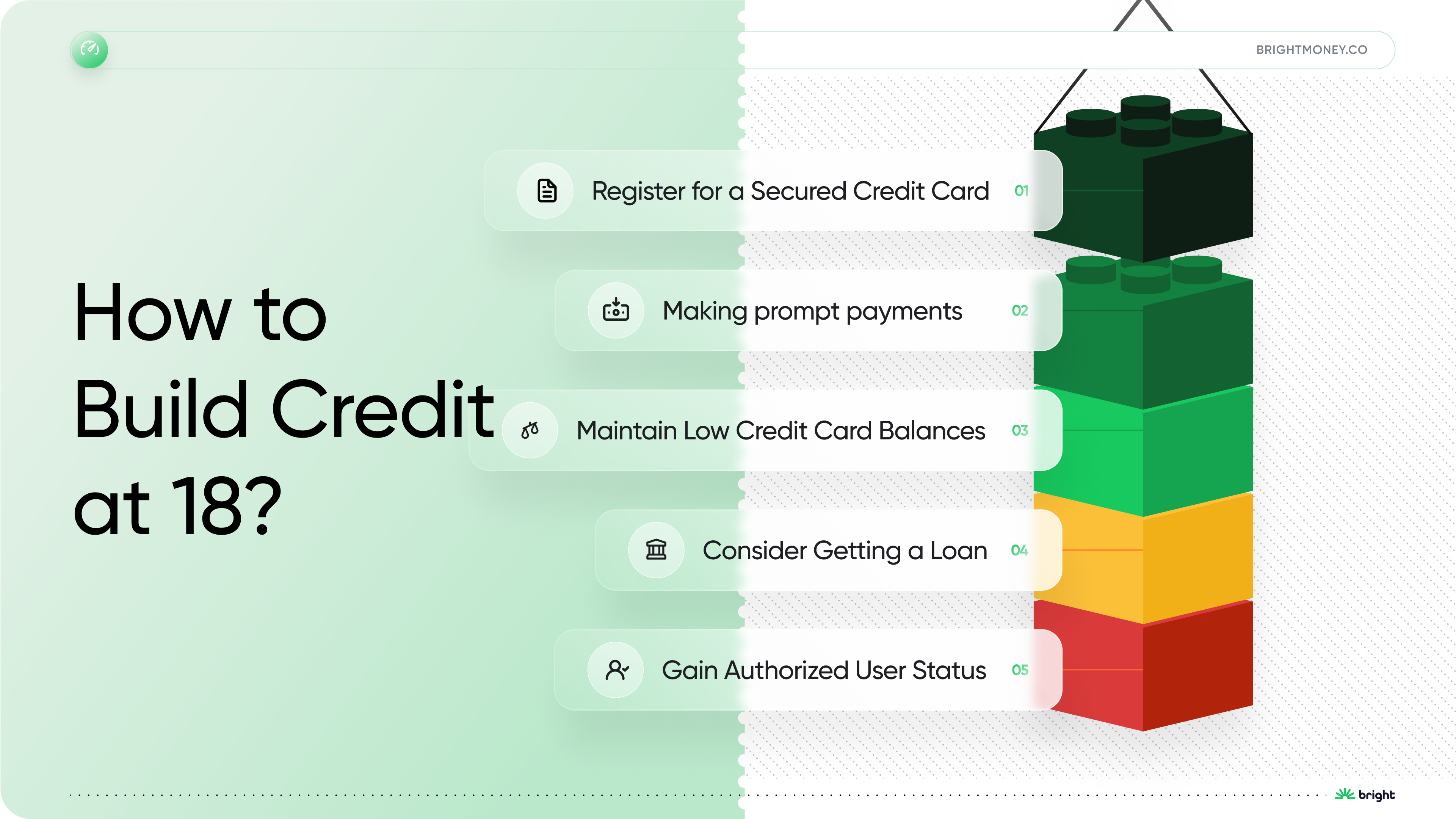

8 Credit Building Strategies

Building credit at the age of 18 is a smart move that can set you up for financial success in the future. Establishing a positive credit history early on can make it easier for you to get approved for loans, credit cards, and even better interest rates down the line. Here are some practical strategies to build credit fast and responsibly:

1. Register for a Secured Credit Card

Consider getting credit cards to build credit if you'd prefer to do it on your own. Signing up for a secured credit card advances your credit-building efforts by 15%. A security deposit is needed for a secured credit card, and that amount serves as your credit limit. Lenders are more likely to approve your application even with little or no credit history because the deposit serves as collateral.

Timely repayment of your charges will contribute positively to your credit history, and you may even receive your deposit back when you close the account. Be diligent about paying your credit card bill on time to avoid potential negative impacts on your credit. The positive impact of using a secured credit card responsibly may start showing on your credit report within six months to a year of consistent and timely payments.[1]

2. Making prompt payments

Being on time with your payments is essential for establishing credit. Making prompt payments is one of the best ways to build credit. It carries 35% weight in your credit report. Late payments can significantly lower your credit score and stay on your credit report for up to seven years. Make sure you pay all of your bills, including credit card balances and other debts like auto or school loans, on time.

Enrolling in autopay is a practical step to prevent missed payments. Moreover, it's essential to monitor your accounts for accurate billing regularly and to catch any possible overcharges. The impact of timely payments on your credit score is significant.

Responsible financial behavior and reliability to creditors are demonstrated through on-time payments, resulting in a positive credit history. Consistently making prompt payments over several months to a year can lead to noticeable improvements in your credit score, depending on your overall credit history.[1][2]

Read more: Should I pay my credit card bill as soon as I get it?

3. Maintain Low Credit Card Balances

Your credit utilization ratio is a crucial factor that heavily influences your credit score. It represents the amount of credit you use compared to your credit limits. Equally important is the maintenance of low credit card balances, which holds a 25% significance in determining your credit score. To keep a healthy credit utilization ratio, aiming for a level below 30% is advisable, with an even more recommended threshold of approximately 10%.

To illustrate, suppose your credit card has a limit of $2,000. In that case, it's wise not to borrow more than $600 at any given time. By doing so, you can avoid high credit utilization, which hurts your credit score. Maintaining low credit card balances is crucial to ensuring a positive credit score outcome.

Responsible credit usage is demonstrated through this strategy, and it can significantly improve your credit score. You may start noticing positive changes within one to two billing cycles as credit card companies update the information to credit bureaus.[1][2]

4. Consider Getting a Loan

Taking out a loan can be beneficial to build credit fast, although it's not essential if you don't require one. The possibility of obtaining a loan holds a 10% weightage in building credit. Student loans, personal loans, or car loans, when repaid on time, can contribute positively to your credit history. However, avoid taking out loans solely for building credit. Instead, consider a credit-builder loan specifically designed to help establish credit.

A credit-builder loan is an effective method to build credit fast. You make regular deposits into an account each month, and at the end of the loan term, you receive the accumulated funds, often with interest. These loans are available through local credit unions or online lending platforms.

When managed responsibly with timely payments, credit-builder loans can have a substantial positive impact on your credit score. Whether you opt for a credit-builder loan from Bright Money or other types of loans, improvements in your credit score can be observed within a few months to a year, depending on the length of the loan term and your overall credit history.[1]

5. Gain Authorized User Status

If you have a trusted family member or friend with a strong credit history, ask them to add you as an authorized user on one of their credit cards. By doing so, their positive payment history can be reflected on your credit report and improve your credit score. However, keep in mind that any negative payment activity by the primary cardholder could adversely impact your credit score.

The impact of gaining authorized user status as a strategy cannot be precisely quantified, as it depends on the primary cardholder's payment history. As an authorized user, the strategy may start showing results on the authorized user's credit report within a few months of being added to the account.[1][2]

Discover the smart way to improve your credit score with Bright Money. Sign up now!

6. Monitoring and Maintaining Credit

Building credit is an ongoing process that requires consistent effort. As you implement the best way to build credit above, it's important to keep a few additional tips in mind:

1. Monitor Your Credit Reports: Regularly check your credit reports for accuracy and dispute any inaccuracies promptly. Staying informed about the information contained in your credit reports will help you track your progress and identify areas for improvement.

2. Limit New Credit Applications: Avoid applying for multiple credit accounts within a short period. Too many inquiries can lower your credit score and be seen as a red flag by lenders. Be selective and intentional about the credit you apply for.

3. Practice Responsible Borrowing: Use credit responsibly and avoid accumulating unnecessary debt. Only borrow what you can comfortably repay within the specified timeframe. Demonstrating responsible borrowing habits will strengthen your creditworthiness, and you can improve your credit score over time.[3]

Bottom Line

Learning how to build credit at 18 is crucial for establishing a solid financial foundation. By understanding the fundamentals of credit scores and reports and implementing strategies such as becoming an authorized user or opening credit cards to build credit, you can build credit fast and effectively. Making timely payments, maintaining low credit card balances, and considering loans for responsible borrowing are all part of the best way to build credit.

Remember to monitor your credit reports regularly to ensure accuracy and take the necessary steps to dispute any errors. With dedication and responsible financial habits, you can successfully improve your credit score and pave the way for a brighter financial future.

Ready to take control of your credit? Start building a bright financial future with Bright Money today. Get App!

References:

- https://www.forbes.com/advisor/credit-score/how-to-build-credit-at-18/

- https://www.chase.com/personal/credit-cards/education/build-credit/how-to-build-credit-at-18

- https://www.bankbazaar.com/cibil/credit-monitoring.html

FAQs

Q. How long does it take to build credit from scratch?

Building credit from scratch can take time. It typically requires at least six months of responsible credit activity to start establishing a credit history. However, building a strong credit profile can take several years of consistent positive payment history and responsible borrowing habits.

Q. Can I build credit without a credit card?

Yes, you can build credit without a credit card. Alternative options include becoming an authorized user on someone else's credit card, taking out a credit-builder loan, or ensuring that your rent payments are reported to credit bureaus.

Q. How many credit cards should I have to build credit?

There is no specific number of credit cards required to build credit. It's more important to focus on responsible credit usage rather than the quantity of cards. Start with one or two credit cards and use them responsibly to build a positive credit history.

Q. Will building credit at 18 affect my credit score?

Building credit at 18 can have a positive impact on your credit score if you make timely payments, maintain low credit utilization, and establish a positive credit history. Responsible credit management at a young age can set you on a path to a stronger credit score over time.

Q. What is the fastest way to improve my credit score?

Improving your credit score takes time, but there are steps you can take to expedite the process. Focus on making all payments on time, paying down debt to reduce credit utilization, and avoiding new credit applications. Regularly monitoring your credit reports for errors and disputing inaccuracies can also help improve your credit score.

* Payment history has the biggest impact on credit score accounting for 40% of how score is calculated per TransUnion (https://www.transunion.com/credit-score). Bright Builder helps you build a payment history that may positively improve your credit score. A credit score increase is not guaranteed. Individual results may vary. Late payments, missed payments, or other defaults on your accounts with us or others will hurt your credit score. Products and services are subject to state residency and regulatory requirements. Bright Builder is currently not available in all states.