You are now leaving the Bright website and entering a third-party website. Bright has no control over the content, products, or services offered, nor the security or privacy of information transmitted to others via their website. We recommend that you review the privacy policy of the site you are entering. Bright does not guarantee or endorse the products, information, or recommendations provided on any third-party website.

No one likes being in Debt. It's like having a cloud hanging over you. One way to clear it faster is to make payments every two weeks. This can help reduce the interest you pay. Another idea is to look for Credit Cards with lower interest rates and move your debt there. But you have to read the fine print to avoid any surprises. And sometimes, just talking to your bank or Credit Card company can help.

They might offer a better payment plan. A dilemma many face is deciding between Debt pay off or investing in opportunities. In this article, we'll explore these options and more, giving you a roadmap to a Debt-free future.

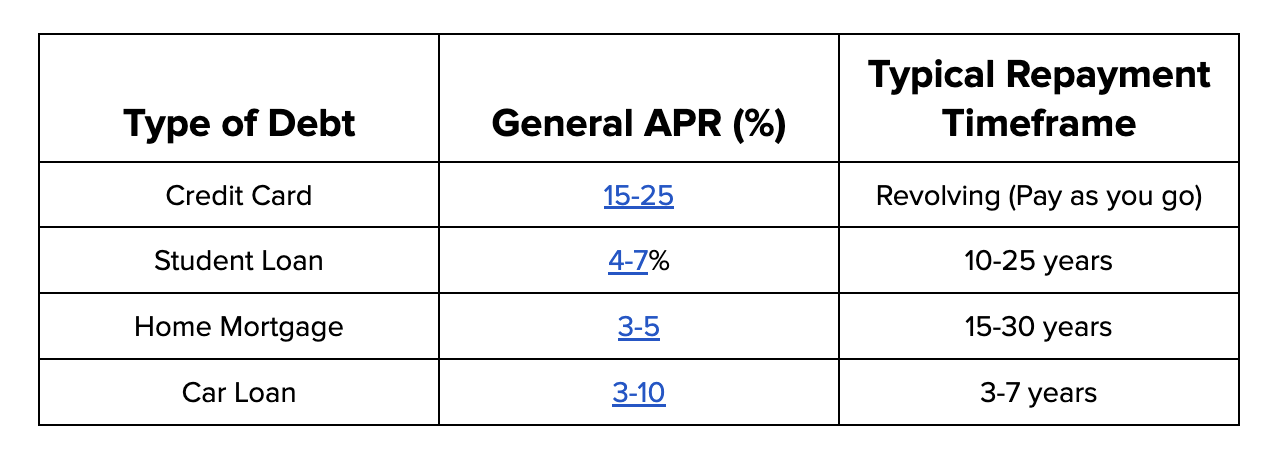

Which Type Of Debt Should You Pay Off First?

The quickest way to pay off all your Debt is to prioritize and see which one you need to pay off first. While a lot of factors come into play while making this decision, here’s what you can generally follow

Disclaimer: Information on brightmoney.co is for informational purposes; we do not guarantee its accuracy or update frequency. Verify independently and seek professional advice for financial decisions.

Best Tools to Pay Off Debt Quickly

1. Debt Consolidation for Credit Card Debt

Juggling multiple Credit Card Debts can be a financial and emotional burden. Debt consolidation simplifies this by merging all your outstanding balances into a single loan, often with a lower interest rate. One tool that stands out for this purpose is Bright Money. It employs artificial intelligence to analyze your spending habits and outstanding Debts. Then it crafts a personalized repayment plan for you. The platform can even automate your payments, ensuring you never miss a due date.

2. Student Loan Forgiveness Programs

Student loans can be a long-term commitment that many find overwhelming. If you're in specific professions like teaching, nursing, or public service, you might be eligible for loan forgiveness programs. These programs can wipe out a significant portion of your Debt after you've made a predetermined number of on-time payments. However, eligibility criteria can be stringent, and you'll need to make sure you're in a qualifying repayment plan.

3. Refinancing Home Loans

Home loans are often the largest Debt a person will take on in their lifetime. Refinancing can offer relief by replacing your existing mortgage with a new loan at a lower interest rate. This can result in lower monthly payments and potentially save you thousands over the life of the loan. It's important to calculate these costs to ensure that refinancing will actually save you money in the long run.

Strategies To Pay Off Debt Faster

1. Pay as per Interest Rates

Interest rates play a pivotal role in the world of loans and Credit Card Debt. Simply put, an interest rate is a percentage charged on the principal amount borrowed or the amount of credit used. It's the price you pay for the privilege of borrowing.

Different loans and Credit Cards come with distinct interest rates. For example, personal loans might offer a fixed interest rate, while Credit Card rates can be variable. This distinction is crucial because the type of interest rate can influence the total amount you'll repay over the loan's lifetime.

One key aspect to grasp is the compounding effect of interest. If you only pay the minimum amount due on a Credit Card, the unpaid balance gets carried over to the next month, and interest is charged on this new amount. Over time, this can lead to a significant increase in your Debt, making it harder to pay off.

Understanding interest rates and their implications is the first step in crafting an effective Debt repayment strategy. It is generally better to pay off Debts with higher and compounding interest rates first.

2. Extra payments For lesser time

Now, you don't need a huge amount to make a difference. Let's say you owe $10,000 with an interest rate of 5%. By just paying an extra $50 a month, you can save almost $650 in interest and reduce your pay-off time by nearly a year! Tiny steps, huge leaps!

Before you buy that fancy coffee or new shoes, think of your future self. By prioritizing your Debt payments, you're essentially paying yourself first. This mindset shifts how you approach money and can fast-track your journey to a Debt-free existence.

So next time you ponder on how to pay off Debt or Debt pay off or save, remember: every penny counts. It's the small, consistent actions that propel you to a financial win. Choose wisely!

3. Debt Consolidation as a speed strategy

When drowning in a sea of multiple Debts, you often wish for a lifesaver, don't you? This is where Debt consolidation can come to your rescue.

At its core, Debt consolidation is the act of merging various Debts into one. Instead of juggling five different monthly payments at varying interest rates, imagine having just one manageable payment! It's a simplifying strategy many employ in their journey on how to pay off Debt.

Criteria to Eye for Consolidation:

- Interest Rate: Ideally, your consolidated loan should carry a lower interest rate than your current Debts

- Loan Term: While a longer term might lower your monthly payments, it could cost more in the long run. So, be mindful!

So, next time you wonder about how to pay off Credit Card Debt or contemplate Debt pay off or save, remember: Debt consolidation can be a solid strategy. But just like any powerful tool, wield it wisely.

4. Balance Transfers for Credit Card Debt

A balance transfer is a financial strategy where you transfer the Debt from one or more Credit Cards to another Credit Card. This new card often has a lower introductory interest rate. When selecting a balance transfer card, consider the following:

- Transfer Fee: Seek out cards with minimal or no transfer fees

- Introductory Rate Duration: A card offering an extended period of 0% interest can be more beneficial

- Other Fees: Ensure there aren't any hidden charges that could surprise you later

While a balance transfer can be advantageous, it's essential to understand the offer's terms. Some cards might increase the interest rate significantly if you miss a payment. If the balance isn't cleared before the introductory rate ends, you could be subject to higher interest rates.

In the journey of how to pay off Debt, utilizing balance transfers can be an effective strategy. However, it's vital to approach it with a clear understanding and select the most suitable card for your situation.

5. The Role of Budgeting

Budgeting is more than just jotting down numbers. It's understanding where every penny of your income is allocated. At the foundation of financial clarity, budgeting is paramount. When you know where your money goes, it's easier to cut down on unnecessary expenditures.

There are tech tools to simplify this task. For example, apps like Mint provide an overview by linking with your bank accounts, categorizing each spend. On the other hand, YNAB (You Need a Budget) ensures you have a plan for every dollar that comes in. These digital assistants not only streamline the process but also provide insights, offering a snapshot of where you might be overspending.

Furthermore, it's not just about setting a budget, but regularly reviewing it. Adjustments might be necessary as unexpected costs arise. But it's not just about the numbers. A well-structured budget imparts a sense of control. It curtails impulsive purchases that often set us back on our financial journey.

6. Increasing Income for Faster Payoff

While managing and reducing expenses is a pivotal step, there's another side to the equation: increasing your income. This doesn't necessarily mean switching jobs but tapping into opportunities alongside your primary profession.

The digital age has broadened horizons. Platforms such as Upwork offer freelancing opportunities ranging from content creation to web design. If education is your forte, websites like Tutor.com can be avenues for sharing knowledge in exchange for pay. Furthermore, Rover allows pet enthusiasts to earn by taking care of animals.

Beyond side gigs, think about personal growth. Upskilling or furthering your education can be a golden ticket to demanding a higher wage or stepping up the career ladder. Investing in courses on platforms like Coursera might just be the catalyst for that paycheck boost.

The Snowball and Avalanche Methods

Understanding the strategies to pay off Debt efficiently is crucial for financial well-being. Two such strategies that have gained prominence over the years are the Snowball and Avalanche methods. Here, we'll delve into these methods and evaluate their pros and cons.

1. Snowball Method

Start by paying off the smallest Debt amount first, irrespective of its interest rate. Once that's cleared, move on to the next smallest amount. The idea behind this method is the psychological satisfaction derived from clearing a Debt completely.

Pros:

- Provides a psychological boost by clearing Debts

- Simplifies Debt by reducing the number of outstanding amounts

Cons:

- Might lead to higher total interest payment over time

- Not always the most cost-effective approach

2. Avalanche Method

This strategy focuses on Debts with the highest interest rates. By paying off high-interest Debts first, you can potentially reduce the total interest paid over time.

Pros:

- Economically efficient as it aims to reduce total interest

- Targets the most financially draining Debts first

Cons:

- Initial progress might seem slow

- Requires more discipline as the focus isn't on quick wins

To choose between the two, one should consider their financial discipline and psychological needs. The Snowball method might appeal to those who gain motivation from quick achievements, whereas the Avalanche method is designed for those looking for long-term financial efficiency.

Conclusion

Clearing Debt swiftly is a common goal. The considerations of Debt payoff or investment come into play, especially when looking at the bigger financial picture. Making payments more frequently, like bi-weekly, can chip away at the principal faster.

Exploring options like balance transfers to cards with promotional interest rates can offer temporary relief. Engage with financial institutions; sometimes, they're willing to renegotiate terms. Stay informed, stay proactive, and remember that every decision should move you closer to a life free from the shackles of Debt.

Bright Money can help free you from those shackles. Check out our app to know how!

Read More:

- The Real Story Behind Free Credit Score Promotions.

- Does Financing A Car Build Credit?

- Credit Builder Loans vs PayDay Loans

FAQs

- Is it realistic to pay off a $100k loan quickly?

Paying off a $100k loan quickly is a significant financial challenge. The feasibility largely depends on your income, expenses, and commitment. By prioritizing the loan repayment above other non-essential expenses and possibly seeking additional income sources, you can accelerate the Debt pay off process. It's essential to have a clear strategy and understand how to pay off Debt in sizable chunks like this.

- What strategies can help in rapid repayment of such a large loan?

Several strategies can be employed. Refinancing the loan to get a lower interest rate can save money over time. Making bi-weekly payments instead of monthly can also reduce the interest accrued. Allocating windfalls, bonuses, or tax returns directly to the loan can make a dent. It's all about being proactive in your "Debt pay off or invest" decisions and consistently looking for ways to reduce the principal.

- How can I stay motivated with such a daunting Debt amount?

A $100k Debt can feel overwhelming, but breaking it down into smaller milestones can help. Celebrate every $5k or $10k paid off. Engage with online communities where individuals share their "how to pay off Credit Card Debt" or large loan stories. Their journeys can provide motivation and practical tips. Remember, every payment, no matter how small, brings you closer to being debt-free.

- Are there tax implications when paying off a large loan quickly?

Depending on the type of loan, there might be tax implications. For instance, mortgage interest can be tax-deductible in some cases. It's essential to consult with a tax professional to understand any potential benefits or drawbacks in your "Debt pay off or save" journey, especially when dealing with large sums.

- Can I negotiate the terms of a $100k loan if I face financial hardships?

Lenders often prefer receiving some payment rather than none. If you face financial challenges, it's crucial to communicate with your lender early. They might offer temporary relief, reduced interest rates, or even a modified repayment plan. Being proactive and transparent can open doors to solutions on how to pay off Debt under challenging circumstances.

References:

- https://www.kotak.com/en/stories-in-focus/cards/credit-cards/6-proven-ways-to-pay-off-credit-card-bills-fast.html

- https://bettermoneyhabits.bankofamerica.com/en/debt/how-to-pay-off-credit-card-debt-fast

- https://www.bankrate.com/finance/credit-cards/ways-to-pay-off-credit-card-debt/

- https://www.bankbazaar.com/credit-card/pay-off-your-credit-card-bill-faster.html