You are now leaving the Bright website and entering a third-party website. Bright has no control over the content, products, or services offered, nor the security or privacy of information transmitted to others via their website. We recommend that you review the privacy policy of the site you are entering. Bright does not guarantee or endorse the products, information, or recommendations provided on any third-party website.

When it comes to handling your finances, making informed decisions is crucial. Credit builder loans and payday loans are two popular options that can have a significant impact on your financial well-being. These financial tools can serve vastly different purposes, each with its own set of benefits and drawbacks.

But before we get into the topic, it is recommended to first read about how a credit builder loan builds credit and what a payday loan is in detail by Bright Money!

In this article, we will delve into the differences between credit builder loans and payday loans, helping you understand which option suits your needs and goals.

What are Credit Builder Loans?

Did you know that reports indicate that borrowers who successfully complete Credit Builder Loan terms experience an average increase of 30-60 points in their credit scores within the first year? Credit builder loans are a financial tool designed to help people build their credit scores. Unlike traditional loans, where you receive the loan amount upfront, credit builder loans work in reverse.

Lenders fund secured accounts, such as savings accounts or Certificates of Deposit (CDs), with the loan amount you request when you apply for a credit builder loan. When you pay back the loan each month, the credit bureaus will be receiving a record of your payments, which gradually raises your credit score.

The purpose of credit builder loans is to assist individuals with limited credit history or a less-than-stellar credit score in building a stronger credit profile. These loans are often a stepping stone to better interest rates and terms for future loans, including mortgages and auto loans.

Characteristics of Credit Builder loans

Here are the characteristics of credit builder loans:

- APR (Annual Percentage Rate):

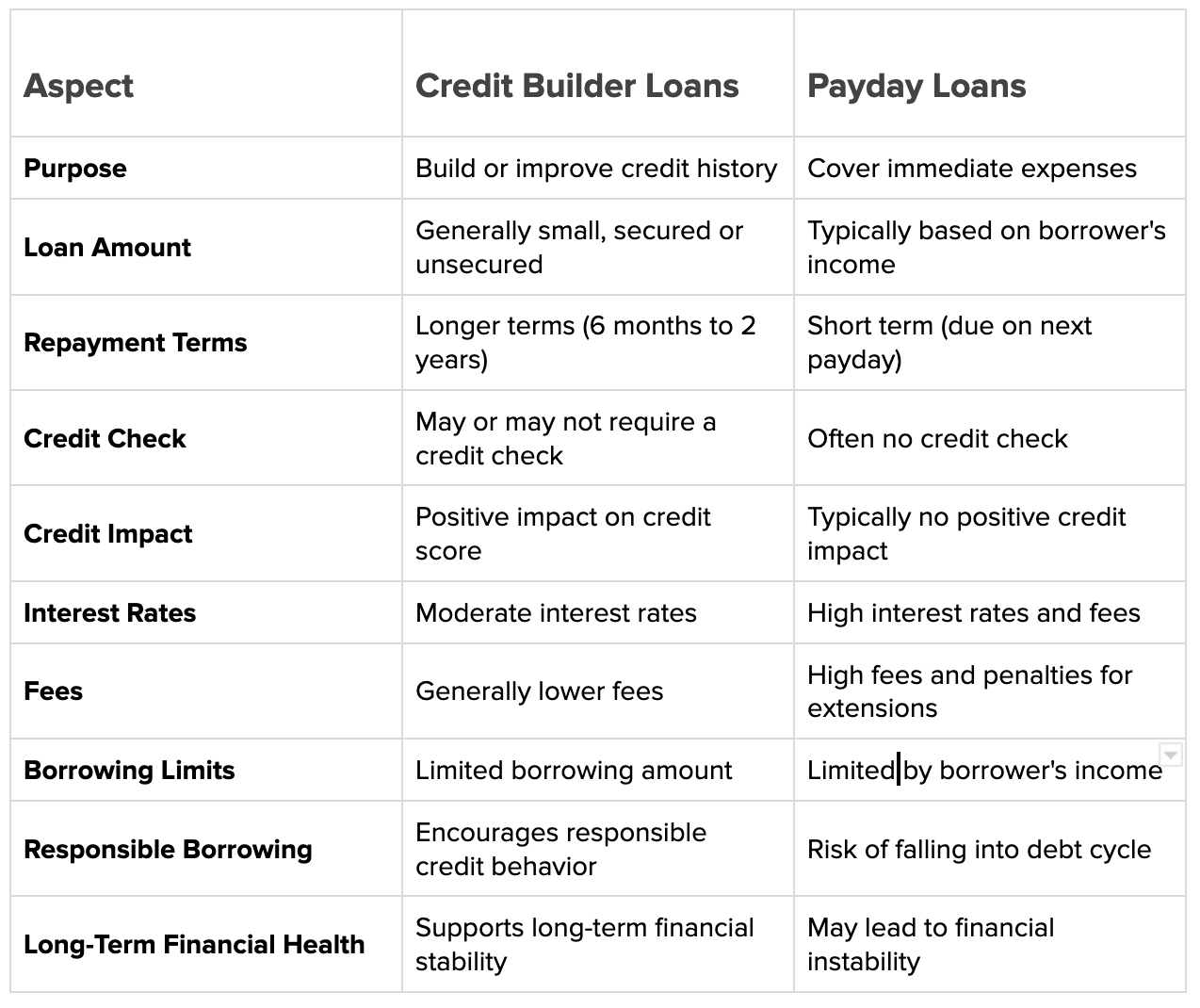

Credit builder loans typically offer lower APRs compared to payday loans. The APR for credit builder loans is generally in the single digits or low teens, making them more affordable and cost-effective for borrowers.

- Tenure:

Credit builder loans have longer tenures, often ranging from 6 months to 2 years or more. The extended repayment period allows borrowers to build credit gradually and make manageable monthly payments.

- Amount:

Credit builder loans usually provide smaller loan amounts, often ranging from $500 to $2,000. These loans are designed to be small enough to manage while still contributing positively to your credit history.

- Restrictions:

Credit builder loans may have eligibility criteria that require borrowers to have a bank account or meet certain income thresholds. However, they are generally more accessible to borrowers with low or no credit scores.

What are Payday Loans?

Payday loans represent a short-term financial solution tailored for those who require swift access to funds to bridge the gap between paychecks. These loans are specially designed to help individuals manage unforeseen and pressing expenses that arise unexpectedly. When faced with a sudden medical bill, car repair, or other urgent financial needs, payday loans offer a way to secure the necessary funds promptly.

Typically, payday loans are characterized by their small loan amounts, which are based on the borrower's income. The premise is simple: You borrow a relatively modest sum, intending to repay it as soon as your next paycheck arrives. This immediate repayment structure is what sets payday loans apart from other lending options.

Characteristics of PayDay loan

Here are the characteristics of payday loans:

- APR (Annual Percentage Rate):

Payday loans are notorious for their extremely high APRs, often exceeding 300% or even 400%. These exorbitant interest rates can lead to a cycle of debt for borrowers.

- Tenure:

Payday loans typically have very short repayment terms, usually around two weeks to a month. This short tenure can make it challenging for borrowers to repay the full loan amount on time.

- Amount:

Payday loans offer relatively small loan amounts, typically ranging from $100 to $1,000. These loans are meant to cover immediate, small-scale expenses until the borrower's next paycheck.

- Restrictions:

Payday loans often come with fewer eligibility restrictions, making them accessible to borrowers with poor credit or no credit history. However, the lack of stringent requirements can also lead to borrowers falling into debt traps due to the ease of obtaining payday loans.

What are the advantages of Credit Builder Loans?

Credit builder loans present a range of advantages that can positively impact your financial journey:

- Gradual Credit Improvement: One of the primary benefits of credit builder loans is their potential to contribute to your credit score improvement over time. When you make regular and on-time payments toward your credit builder loan, this positive payment behavior gets reported to credit bureaus. This activity, in turn, helps establish a positive credit history, a critical factor in calculating your credit score. As your payment history improves, your credit score gradually ascends, creating a stronger foundation for your financial future

- Forced Savings: Credit builder loans offer a unique aspect that can aid in building your savings while improving your credit. Whenever you apply for a credit builder loan, the loan amount is often held in a secure account, like a Certificate of Deposit (CD) or a dedicated savings account. As you make consistent payments, these payments accumulate in the secure account. Once the loan is fully paid off, you gain access to the accumulated funds. This mechanism effectively encourages disciplined savings, helping you develop a nest egg for future needs

- Establishing Financial Habits: Another advantage of credit builder loans is their role in fostering responsible financial habits. Committing to regular payments over the course of the loan term helps develop a pattern of reliable financial behavior. As you adhere to the payment schedule and manage your budget accordingly, you gain a deeper understanding of your financial capabilities and limitations. This experience lays the groundwork for better money management practices, ultimately contributing to your long-term financial success

- Diverse Credit Mix: Credit builder loans diversify your credit portfolio. A healthy mix of credit types, like installment loans and revolving credit, can positively influence your credit score. By adding an installment loan like a credit builder loan to your credit history, you enhance the variety of credit types in your profile, potentially boosting your creditworthiness

- Lower Interest Rates in the Future: A strong credit score resulting from responsible credit builder loan payments can translate to better interest rates on future loans. Lenders are more inclined to offer favorable terms to borrowers with proven repayment track records. This means you could enjoy reduced interest charges on mortgages, auto loans, and various other forms of credit, saving you money over time

- Enhanced Loan Approval Chances: Establishing a positive credit history through credit builder loans can increase your chances of loan approval for larger financial goals. Lenders are more likely to be extending credit to the ones with a track record of responsible borrowing and repayment. As a result, you'll be better positioned to secure loans for significant life milestones such as buying a home or financing higher education

- Confidence in Financial Management: Successfully navigating the credit builder loan journey instills confidence in your financial management skills. As you make consistent payments, you build a tangible example of your ability to meet financial obligations. This confidence can influence your overall financial behavior, empowering you to make informed decisions and seize opportunities

- Reduced Reliance on High-Interest Credit: By improving your credit score through credit builder loans, you can potentially reduce your reliance on high-interest credit options like credit cards with steep rates. This shift can result in lower interest payments and decreased financial stress as you manage debt more effectively

- Long-Term Financial Wellness: The combination of credit score improvement, savings development, and responsible financial habits contributes to your overall financial wellness. A higher credit score opens doors to improved financial opportunities, while the savings cultivated during the loan period provide a safety net for unexpected expenses. This comprehensive approach sets the stage for long-term financial stability

What are the Benefits of Payday Loans?

Payday loans offer several distinct advantages that cater to specific financial needs:

- Swift and Immediate Cash: Payday loans are custom-tailored to address urgent financial needs. When faced with unexpected expenses like household repairs or medical bills, payday loans provide a lifeline by offering quick access to funds. The application process is designed for efficiency, ensuring that you can secure the necessary funds in a timely manner

- No Credit Check Required: Unlike traditional loans that often hinge on a detailed credit history analysis, payday lenders typically do not conduct thorough credit checks. This feature can be particularly be beneficial for individuals with poor or limited credit history. The absence of an extensive credit check means that your credit score won't be a barrier to obtaining the funds you need

- Accessible During Emergencies: Payday loans act as a safety net during emergencies. When unforeseen circumstances demand immediate financial attention, payday loans can bridge the gap between paychecks. Whether it's a sudden medical expense, a vehicle breakdown, or a home repair, these loans provide a solution for tackling pressing situations promptly

- Flexibility in Loan Amounts: Payday loans are available in various amounts, allowing you to borrow only what you need. This flexibility ensures that you don't overextend your borrowing and only take out the necessary funds to cover your emergency expenses

- Convenience and Ease of Application: Applying for a payday loan is often a straightforward process. Most lenders offer online applications, enabling you to submit your information from the comfort of your home. The simplicity of the application process, along with the minimal documentation required, means that you can swiftly complete the necessary steps to secure the loan

- No Collateral Requirement: Payday loans are typically unsecured, which means you don't need to provide collateral to obtain the loan. This feature eliminates the risk of losing valuable assets in case you're unable to repay the loan. The absence of collateral can be particularly comforting when dealing with sensitive and urgent financial matters

- Short-Term Commitment: Payday loans are crafted to be short-term borrowing options. This means that you won't carry the burden of long-term debt, as the loan is intended to be repaid on or shortly after your next paycheck. This short repayment window minimizes the financial stress associated with prolonged debt obligations

What are the Key Differences Between Credit Builder Loans & Payday Loans?

Application Process for Credit Builder Loans

Let's say Sarah is a recent college graduate who is looking to improve her credit score. She has limited credit history due to being a student and has encountered difficulties in getting approved for traditional credit cards. She then decides to apply for a credit builder loan.

- Research and Selection: Sarah researches various lenders online and finds Bright Builder, a reputable financial institution offering credit builder loans

- Eligibility Check: Sarah checks the lender's eligibility criteria and sees that Bright Builder doesn't have any such requirements except the fact that she only has to deposit as little as $50 as a security deposit!

- Application Submission: Sarah completes the online application form, providing her personal information and employment details

- Loan Approval and Terms: As there’s no such requirements for Bright Builder, so Sarah's application gets approved for a $1,000 credit builder loan with an interest rate

- Acceptance and Funding: Sarah carefully reviews the loan offer, and electronically signs the loan agreement. The Bright Builder then deposits the $1,000 loan amount into a separate account

- Repayment and Reporting: Sarah makes regular monthly payments of around $88 towards the loan. Every payment is reported to the credit bureaus, helping to build a positive credit history

- Loan Completion: After making all 12 payments on time, Sarah's credit builder loan is considered paid off. Her timely payments have resulted in an improved credit score, making it easier for her to qualify for other credit products in the future

Application Process for Payday Loans

Sarah finds herself facing unexpected medical expenses and needs $500 to cover the bills. She researches online and chooses a reputable payday lender.

- Research and Choose a Lender: Sarah compares different lenders like CashUSA, BadCreditLoans, ClearViewLoans and their terms and decides to go with that lender due to their positive customer reviews and reasonable interest rates

- Gather Required Information: Sarah gathers her driver's license, recent pay stubs, utility bill, and her bank account details

- Online Application: She visits the lender’s website and fills out the online application form, providing accurate financial and personal information

- Review Loan Terms: Within a few hours, the lender reviews her application and offers her a $500 loan with a 15% interest rate, due to be repaid in two weeks

- Acceptance and E-Signature: Sarah agrees to the terms and provides an electronic signature to accept the loan offer

- Verification and Documentation: The lender requests copies of her identification and pay stubs. Sarah promptly scans and sends the required documents

- Loan Approval: After verifying her documents, the lender approves Sarah's loan. She receives a notification stating that her loan application has been successfully processed

Choosing the Right Option for You: Making an Informed Decision

The decision between credit builder loans and payday loans is a pivotal one that requires a thorough evaluation of your unique financial situation and aspirations. A study revealed that the average APR for payday loans can exceed 300%, making them a risky choice for borrowers.

Let's explore the considerations and steps to ensure you make the choice that aligns with your needs:

- Step 1: Assess Your Financial Circumstances

Make a list of your present financial situation first. Consider your credit history, income stability, and existing debts. This assessment will provide insight into which loan option is more suitable for your circumstances.

- Step 2: Define Your Goals

Clarify your financial goals. Are you aiming to improve your credit score, establish financial discipline, or address immediate emergencies? Defining your objectives will help in guiding your decision-making process.

- Step 3: Understand Loan Terms

Thoroughly comprehend the terms associated with each loan option. Pay attention to interest rates, repayment periods, and any additional fees. Calculate the total cost of borrowing to make an accurate comparison.

- Step 4: Consider Long-Term Impact

Think about the long-term consequences of your decision. Credit builder loans contribute to improving your credit score over time, potentially leading to better financial opportunities. Payday loans, while offering immediate relief, could result in high costs and limited long-term benefits.

- Step 5: Analyze Urgency

If you're facing an urgent financial need, such as a medical bill or car repair, a payday loan might provide the quick solution you require. However, if your goal is to strengthen your credit profile, a credit builder loan is a more strategic choice.

- Step 6: Seek Professional Advice

If you're unsure about the best course of action, consider seeking advice from financial advisors or credit counseling services. They can offer objective insights based on your specific situation.

- Step 7: Weigh the Trade-Offs

Every financial decision involves trade-offs. Consider the trade-offs associated with each loan option. Are you willing to pay higher interest rates for the convenience of a payday loan? Are you willing to commit to a longer repayment period for the benefits of a credit builder loan?

- Step 8: Make an Informed Choice

Ultimately, the decision comes down to aligning your needs with the loan option that best meets them. If you're focused on building or improving your credit, a credit builder loan is the strategic route. If urgent expenses demand immediate attention, a payday loan might be the pragmatic choice.

Conclusion

As the dust settles on the comparison between credit builder loans and payday loans, one truth emerges crystal clear: the path to sound financial health is paved with wise decisions. Credit builder loans, with their focus on responsible credit-building and long-term stability, provide a tangible means to strengthen your financial foundation. On the other hand, payday loans, while offering quick fixes, come at the cost of high fees and potential debt traps.

In the end, the choice boils down to your financial goals and values. Remember, every financial decision is a stepping stone toward your aspirations. So, tread wisely. Whether you opt for credit builder loans or cautiously explore alternatives, always prioritize your financial well-being. After all, making the right choice today can shape a brighter, more secure tomorrow.

Recommended Reads:

How to check your credit score?

Top 5 types of credit cards to build credit

FAQs

1. Will I get a Credit Builder Loan with no credit history?

Yes, Credit Builder Loans are ideal for establishing credit when you have no credit history. They offer a structured way to build credit from scratch.

2. What are the typical repayment terms for Credit Builder Loans?

Repayment terms for Credit Builder Loans can vary, but they generally range from 6 months to 2 years. Longer terms may be available depending on the lender.

3. Do Payday Loans require a credit check?

Payday Loans typically do not require a credit check, which is why they are often considered a quick borrowing option. However, they come with high costs.

4. Can Credit Builder Loans help improve my credit mix?

Yes, having different types of credit, including installment loans like Credit Builder Loans, can positively impact your credit mix, a factor in your credit score.

5. What happens if I can't repay a Payday Loan on time?

If you can't repay a Payday Loan on time, you may have the option to extend the loan, but this usually comes with additional fees. This can lead into a cycle of debt.

6. Are there alternatives to Payday Loans in emergencies?

Yes, other options include taking out a credit card with a reduced interest rate, borrowing money from friends or family, or applying for personal loans from banks or credit unions.

7. Can I get a Credit Builder Loan online?

Yes, many online lenders offer Credit Builder Loans. Just be sure to research the lender's reputation and terms before proceeding.

8. How do Credit Builder Loans differ from secured credit cards?

Credit Builder Loans involve borrowing and repaying a fixed amount, while secured credit cards require a deposit as collateral and allow you to spend up to that amount.

9. Can a Credit Builder Loan improve my credit score if it's already good?

If your credit score is already good, the impact of a Credit Builder Loan may be less significant. However, it can still diversify your credit profile.

10. Are there organizations that offer financial counseling on these options?

Yes, many nonprofit organizations offer financial counseling and education to help individuals make informed decisions about Credit Builder Loans and Payday Loans.

References:

https://files.consumerfinance.gov/f/documents/cfpb_targeting-credit-builder-loans_report_2020-07.pdf

https://www.investopedia.com/payday-loans-vs-personal-loans-5214282