You are now leaving the Bright website and entering a third-party website. Bright has no control over the content, products, or services offered, nor the security or privacy of information transmitted to others via their website. We recommend that you review the privacy policy of the site you are entering. Bright does not guarantee or endorse the products, information, or recommendations provided on any third-party website.

Home Improvement Loans come with a wide range of interest rates, starting as low as 3% and going up to 36%. Repayment terms are equally varied, from two to seven years. Economic factors play a significant role in determining these rates.

Hidden terms and conditions in loan agreements can make or break the deal. Risk management is crucial, as is having a solid repayment strategy. The goal here is to equip you with the knowledge to navigate these complexities. So, let's get into the details.

What is a Home Improvement Loan?

A Home Improvement Loan is money borrowed to finance projects in your home. The U.S. Census Bureau reports that homeowners spent $522 billion on such projects from 2017 to 2019.

Types of Home Improvement Loans:

- Personal Loans: These are unsecured. Interest rates can go from 3% to 36%. You have to pay back the loan in 2 to 7 years. These loans are good for small projects like fixing a roof

- Home Equity Loans: Your home acts as collateral. Interest rates are usually between 4% and 7%. You can take up to 30 years to repay. Use these for big projects like redoing a kitchen

- HELOCs: This is a line of credit against your home. The interest rates change. You pay interest only on what you borrow. Use these for projects where you don't know the total cost upfront

- Cash-Out Refinance: You refinance your mortgage for a larger amount and use the extra for home improvement. The interest rate is similar to your mortgage rate. This is a long-term loan often used for big, multiple projects

Usage:

- Personal Loans: Use these for quick fixes like a new HVAC system

- Home Equity Loans: These are for large projects that you do all at once, like adding a new room

- HELOCs: Use these for ongoing projects, like a series of repairs

- Cash-Out Refinance: Use these for multiple big projects, like redoing the roof and installing a pool at the same time

Each loan type has its own rules and risks. Make sure the loan matches your project and that you can pay it back. Always read the terms carefully before you decide.

How do Home Improvement Loans work?

- Stage 1 - Application Process: To apply, you need documents like tax returns, proof of income, and credit reports. You can apply online or in person. Some lenders may also ask for property assessments

- Stage 2 - Approval Criteria: Lenders look at your credit score, income, and Debt-to-income ratio. A credit score above 700 usually results in approval and a lower interest rate. Your income should be stable, and your Debt-to-income ratio should be below 43%

- Stage 3 - Loan Disbursement: After approval, you get the money. Some lenders give the full amount at once. Others give it in parts for bigger projects. According to the Federal Reserve, it takes about 14 days from application to getting the money

- Stage 4 - Repayment: You repay the loan amount plus interest. Interest rates range from 3% to 36%. Repayment time varies from 2 to 30 years. A good tip is to pay more than the minimum to reduce the loan repayment time and total interest

That's the process from start to finish. Each step has its own requirements and timelines. Make sure you understand them all to manage your loan effectively.

If you're struggling with multiple high-interest Debts, consider consolidating them into a single loan with Bright Money's Debt Consolidation program. This could potentially lower your interest rates and simplify your repayment process, helping you become Debt-free faster.

Pros and Cons

Pros

- No Collateral Required: Personal Loans often don't need collateral, reducing risk to your home

- Fixed Interest Rates: Monthly payments are predictable, aiding financial planning

Cons

- High Interest Rates: Poor credit can result in rates up to 36%, increasing the cost of the loan. To mitigate, compare multiple lenders to find the best interest rate

- Risk of Over-Borrowing: Easy approval might tempt you to borrow more than needed, leading to Debt issues. Know your project's cost and add a small buffer for unexpected expenses, but don't exceed it

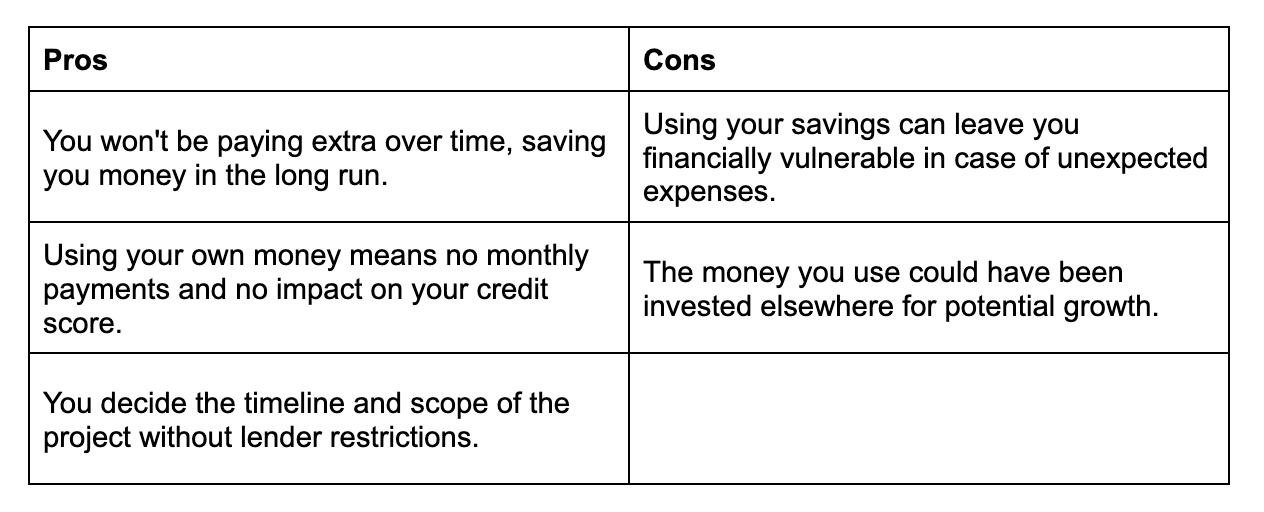

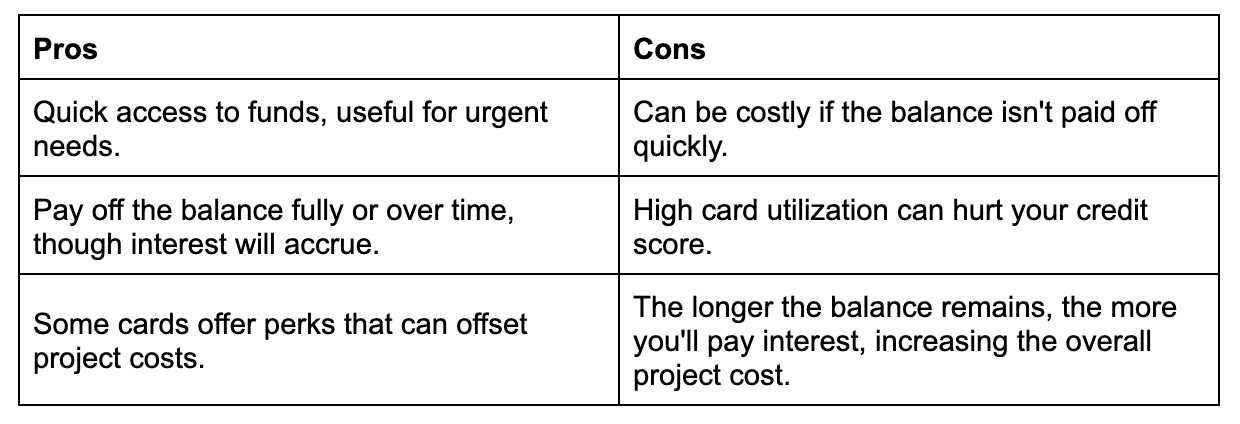

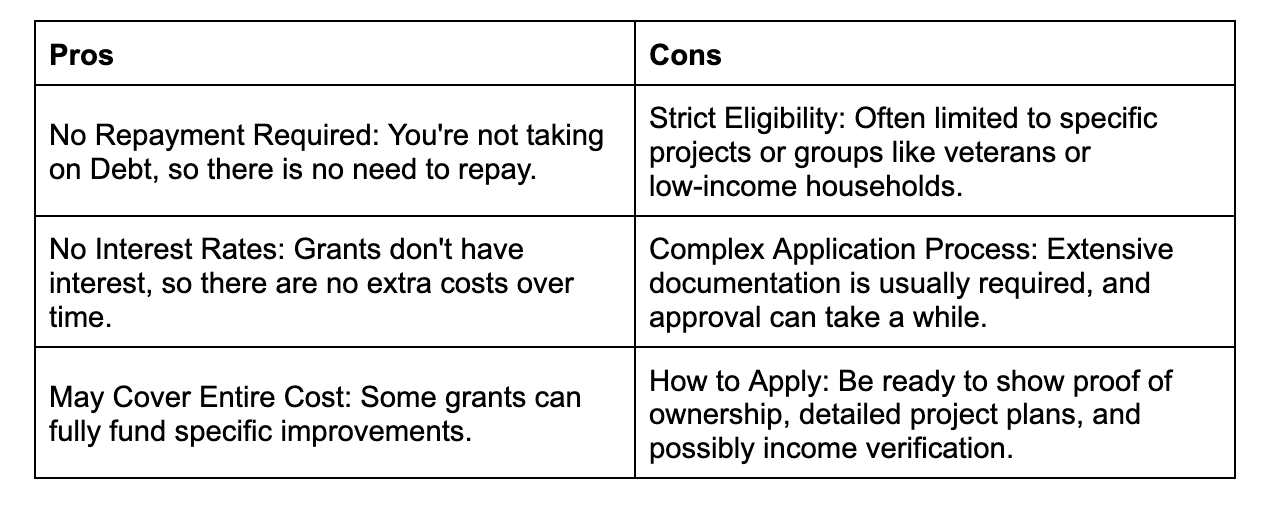

Alternatives to Home Improvement Loans

1. Savings

2. Credit Cards

3. Government Grants

If you're struggling with multiple high-interest Debts, consider consolidating them into a single loan with Bright Money's Debt Consolidation program. This could potentially lower your interest rates and simplify your repayment process, helping you become Debt-free faster.

How to find the best Home Improvement Loan?

Interest Rates

It's crucial to shop around. Different lenders offer varying interest rates. Some might offer introductory rates that look appealing but can skyrocket later. Make sure you understand the full terms.

Online calculators are invaluable here. They can show you how even a small difference in interest rate can significantly affect your monthly payments and the total amount you'll end up paying back.

Loan Amount

First, get a detailed estimate of your project's cost. It's wise to add a buffer of around 10-20% for unexpected expenses like delays or material price hikes. However, don't inflate this buffer unnecessarily, as you'll be paying interest on it.

To arrive at an accurate estimate, break down your project into components. Consider labor costs, material costs, and any permits or fees you'll need to pay. Add these up to arrive at a realistic total loan amount.

Repayment Terms

The repayment terms dictate your financial commitment for years to come. You need to know the loan tenure, whether it's a few months or several years, and what the implications are if you miss a payment.

Inquire about late payment penalties. These can be hefty and add to your financial burden. Also, ask if there's an option to pay off the loan early without incurring additional fees. Some lenders charge a prepayment penalty, which could negate any savings from paying off the loan early.

General Eligibility:

You can apply for a Home Improvement Loan either individually or jointly. If the property is co-owned, all owners must apply for the loan. Documentation typically required includes:

- A fully filled application form

- Proof of identity, income, employment, and residence

- Bank statements from the last 6 months

- Photographs

- A cheque for the processing fee

- The original title deed of your home

- A no-encumbrance certificate

- An estimate of your improvement work from an architect or engineer

If you're struggling with multiple high-interest Debts, consider consolidating them into a single loan with Bright Money's Debt Consolidation program. This could potentially lower your interest rates and simplify your repayment process, helping you become Debt-free faster.

Conclusion

Home Improvement Loans offer a structured way to finance renovations, from small fixes to major overhauls. These loans come in various forms, each with its own set of terms, interest rates, and repayment schedules. The application process is often rigorous, requiring a good credit score and stable income for approval. Once approved, managing the loan effectively is crucial to avoid financial pitfalls.

Alternatives like personal savings, credit cards, and government grants also exist, each with its own set of advantages and drawbacks. The key to a successful home improvement project lies in choosing the right financing option, understanding the associated costs, and having a solid repayment strategy.

A thorough assessment of your financial health will lead to better financial planning. Bright Money can build customized financial plans for your unique situations.

Read More:

- HELOC vs. Home Equity Loan: How Do They Work?

- I Need Cash Now: HELOC vs. Personal Loan - Which Is the Right Choice?

- The Real Story Behind 'Free Credit Score' Promotions

FAQs

1. Can I Use a Home Improvement Loan to Build a Home Office?

Yes, you can! With remote work becoming more common, a dedicated home office is a valuable addition. You can use a Home Improvement Loan to create a functional and comfortable workspace. This could also increase your home's resale value down the line.

2. What If I Want to Use the Loan for Multiple Small Projects Over Time?

That's where a Home Equity Line of Credit (HELOC) could come in handy. Unlike a traditional loan that disburses a lump sum, a HELOC lets you draw funds as needed, making it ideal for ongoing or phased projects.

3. Can I Use a Home Improvement Loan for a Pet-Friendly Renovation?

Absolutely! Pet-friendly renovations like fencing your yard or adding a pet door are eligible for Home Improvement Loans. These upgrades not only make your home more convenient but could also appeal to future pet-owning buyers.

4. What If I'm Planning to Sell My House Soon? Is a Loan Still a Good Idea?

It can be, especially if the improvements will increase your home's market value. Just be cautious not to over-improve beyond what's standard in your neighborhood, as you may not recoup the costs when you sell.

5. Can I Use the Loan for Smart Home Upgrades?

Yes, you can use a Home Improvement Loan to integrate smart home technology like security systems, smart thermostats, or advanced lighting systems. These upgrades can make your life easier and could be a selling point for future buyers.

Reference

- https://www.nerdwallet.com/article/loans/personal-loans/how-home-improvement-loans-work

- https://money.com/what-are-home-improvement-loans/

- https://www.indiabullshomeloans.com/blog/give-your-home-a-makeover-with-affordable-home-improvement-loans

- https://intuitivefinance.com.au/what-are-home-improvement-loans-and-how-do-they-work/

- https://www.indiabullshomeloans.com/blog/give-your-home-a-makeover-with-affordable-home-improvement-loans