You are now leaving the Bright website and entering a third-party website. Bright has no control over the content, products, or services offered, nor the security or privacy of information transmitted to others via their website. We recommend that you review the privacy policy of the site you are entering. Bright does not guarantee or endorse the products, information, or recommendations provided on any third-party website.

High-interest Debt is a serious issue that can derail your financial stability for years. We’ve got go-to solutions for you to assist you in tackling this problem head-on. One of the best strategies is to use Personal Loans to consolidate Debt. Credit Cards often come with high-interest rates, averaging 18%.

In contrast, Personal Loans can offer rates as low as 7.5-10%. This rate difference can lead to substantial savings over time. When you consolidate your Debts into one Personal Loan, you simplify your monthly payments. This makes it easier to manage your budget and can free up money for other financial goals like saving for retirement or building an emergency fund.

Why Should You Pay Off High-Interest Rate Debt First?

Paying off high-interest-rate Debts first allows you to accumulate interest-rate savings since the interest payments stack up quickly. It also leads to an improvement in your Credit Score, helps you get out of Debt faster, and allows you more financial freedom in life. Let's take a more nuanced look at why you need to pay off high-interest rate Debt first.

1. The Hidden Costs of High-Interest Debt

High-interest Debt is more than a monthly bill. It's a financial liability that can affect your long-term financial health.

First, let us shed light on the term “Interest Rate Drag.”

This is the difference between the interest rate on your Debt and the potential return on investments. If you're paying 18% on a Credit Card and your investments grow at 7%, you're losing out on an 11% return. This slows down your financial growth and can delay your journey to financial freedom.

Personal Loans can offer a way out. These loans often have lower interest rates than Credit Cards. For example, if you can get a Personal Loan at an 8% interest rate, you could cut your interest payments in half. This can save you thousands of dollars over the life of the loan and speed up your path to being Debt-free.

High-interest Debt is a pressing financial issue that can hinder your ability to save and invest, affecting your personal finances. Understanding the hidden costs and considering options like Personal Loans can be key strategies for improving your financial health.

2. Opportunity Cost

Opportunity cost in the context of high-interest Debt is a critical financial consideration. When funds are allocated to servicing high-interest Debt, they are unavailable for other potentially lucrative investments. For example, if you're paying $200 monthly solely on Credit Card interest, that's $2,400 annually that could have been invested elsewhere.

If that $2,400 were invested in a financial instrument yielding a 7% annual return, the potential earnings would be approximately $168 in just the first year. Extend that over a decade with a consistent 7% return, and you're looking at a missed opportunity nearing $4,000.

High-interest Debt not only depletes your current financial resources but also diminishes your future financial growth potential. Each dollar spent on high-interest payments is a dollar not invested, not growing, and not contributing to your financial stability. Therefore, understanding and mitigating the opportunity costs associated with high-interest Debt is crucial for long-term financial planning.

3. Tax Implications

High-interest Debt like Credit Card balances often come with zero tax benefits, making them even more burdensome. Unlike mortgage interest, which can often be deducted from your taxable income, the interest paid on high-interest Debt doesn't offer this advantage. This lack of tax relief amplifies the financial strain of carrying such Debt.

When considering a Personal Loan to pay off Debt, it's crucial to remember that Personal Loan interest is generally not tax-deductible either. However, the real advantage of a Personal Loan lies in its lower interest rates compared to Credit Cards. This rate difference can lead to substantial savings over the life of the loan, even without the tax benefits. Therefore, while you won't get a tax break, you could still end up saving a considerable amount in interest payments. Let’s take a look at an example to understand your situation better. What happens when you pay off high-interest rate Debt first vs when you pay it late?

Paying Off High-Interest Rate Debt First: A Smart Move

When it comes to managing your finances, tackling high-interest rate Debt as a priority can yield significant benefits. Let's consider an example:

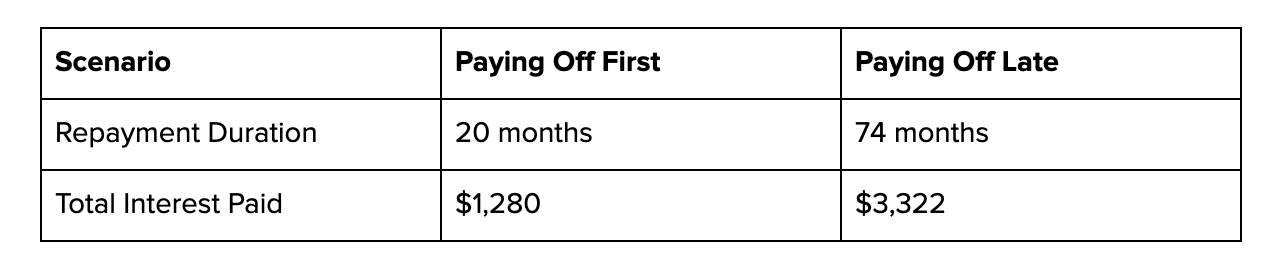

Let's say you have a Credit Card Debt of $5,000 with a high 25% Annual Percentage Rate (APR). Now, let's explore two scenarios:

Scenario 1: Paying Off First

You decide to pay off this high-interest Credit Card Debt aggressively, allocating an extra $300 per month towards it.

In this scenario, you can pay off the Debt in approximately 20 months.

Over the repayment period, you'll pay about $1,280 in interest.

Scenario 2: Paying Off Late

Alternatively, you only make the minimum payments, which could be around $100 per month.

It will take you significantly longer to clear the Debt, around 74 months.

Over this extended period, you'll pay approximately $3,322 in interest.

As seen in the table, paying off high-interest Debt first in Scenario 1 results in a substantially shorter repayment period and significantly less interest paid. This approach not only saves you money but also frees you from Debt more quickly.

For individuals looking for assistance in managing their Debts, services like Debt Consolidation and Bright Money offer solutions to help streamline the process and make paying off high-interest Debt more achievable.

Strategic Repayment Plans

If you're committed to eliminating high-interest Debt, having a well-thought-out strategy is essential. One popular method is the Debt Avalanche approach. This involves listing all your Debts in descending order of interest rates. You then focus on paying off the Debt with the highest interest rate first while making minimum payments on the others. Once the highest-interest Debt is paid off, you move on to the next one on the list.

Personal Loans can be a useful tool in this strategy. By consolidating your Debts into a single Personal Loan with a lower interest rate, you simplify your monthly payments. This can make the Debt Avalanche method easier to manage.

However, Personal Loans are not a one-size-fits-all solution. They often come with origination fees, and the interest rates may not be as low as you expect. It's crucial to read the loan agreement carefully and calculate the total cost, including any fees, before proceeding.

The Role of Emergency Funds

Having an emergency fund is non-negotiable. A Federal Reserve study showed that 40% of Americans would struggle to cover a sudden $400 expense. Even when you're focused on paying off high-interest Debt, it's crucial to have some money set aside for emergencies.

A balanced approach is to start by saving up one month's worth of living expenses. Once you've achieved this, shift your primary focus to paying off high-interest Debt. When considering a Personal Loan for Debt Consolidation, evaluate how this could affect your ability to contribute to an emergency fund. Personal Loans often offer lower monthly payments, which could free up some money for your emergency fund. However, always consider the loan's fees and interest rates to ensure it's a financially sound decision.

Conclusion

The urgency of paying off high-interest Debt cannot be overstated. This blog has delved into the hidden costs, the lack of tax benefits, and strategic repayment methods like the Debt Avalanche. Each of these aspects highlights the critical nature of addressing high-interest Debt as soon as possible.

While Personal Loans can offer a way to consolidate Debt and potentially lower your interest payments, they are not without their drawbacks. Always weigh the pros and cons and make an informed decision that aligns with your financial goals.

Let Bright Money help you navigate Debt Consolidation!

Read More:

- Surviving Debt Consolidation: Dodge These Traps.

- Impact Of Age On Credit

- Score Big In Life: What’s The Magic Credit Score?

FAQs

1. Why prioritize high-interest Debt over lower-interest Debt?

Paying off high-interest Debt first is like plugging the leak in your financial boat before bailing water. High-interest Debt, like Credit Cards, can quickly accumulate, making it costlier in the long run. By tackling these Debts first, you reduce the overall interest you'll pay, freeing up more money for other financial goals.

2. Can I negotiate lower interest rates on my Debts?

Don't hesitate to contact your creditors and negotiate for lower interest rates. Explain your commitment to paying off the Debt and how a reduced rate can help you achieve that. Many creditors are willing to work with you to retain a responsible borrower.

3. Should I use balance transfer cards to consolidate high-interest Debt?

Balance transfer Credit Cards can be a savvy move. They often offer low or 0% interest for an introductory period, allowing you to consolidate high-interest Debt onto one card. Be cautious, though, as transfer fees and high rates after the intro period can negate the benefits.

4. What about using a Personal Loan to pay off high-interest Debt?

Personal Loans can be a smart strategy. They typically have lower interest rates than Credit Cards, allowing you to pay off high-interest Debt more affordably. However, it's crucial to manage your spending and avoid accumulating new Debt.

5. How can I stay motivated while paying off high-interest Debt?

Set milestones and celebrate your progress. Visualize your Debt shrinking, and remind yourself of the financial freedom you're working towards. Engage with online communities or financial advisors for support and guidance. Staying motivated is key to successfully paying off high-interest Debt.

References

- https://www.bankrate.com/personal-finance/Debt/which-accounts-pay-first/

- https://www.investor.gov/introduction-investing/investing-basics/save-and-invest/pay-credit-cards-or-other-high-interest

- https://www.experian.com/blogs/ask-experian/what-Debts-should-i-pay-off-first/

- https://www.investopedia.com/articles/pf/08/invest-reduce-Debt.asp

- https://www.capitalone.com/learn-grow/money-management/which-Debt-should-you-pay-off-first/