You are now leaving the Bright website and entering a third-party website. Bright has no control over the content, products, or services offered, nor the security or privacy of information transmitted to others via their website. We recommend that you review the privacy policy of the site you are entering. Bright does not guarantee or endorse the products, information, or recommendations provided on any third-party website.

Are you considering taking out a loan, but feeling overwhelmed by the thought of calculating loan repayment? Fear not, for we have crafted this comprehensive guide to help you navigate the intricate world of loan repayment calculators. The average loan repayment rate in the USA is estimated to be around 85-90%.

But before we get into the topic, it is recommended to first read about How to apply for student loan forgiveness in detail by Bright Money!

In this article, we will break down the key components of loan repayment, demystify complex terms, and provide you with the tools to confidently manage your loan obligations.

What are the Types Of Loans?

There are broadly two types of loans:

1. Fixed Term Loan/Credit:

A fixed-term loan, also known simply as a "loan," is a type of borrowing arrangement where a specific amount of money is provided to a borrower for a predetermined period. This loan is structured with a fixed term, meaning that both the borrower and the lender agree on a set repayment schedule, including a fixed interest rate, a specified monthly payment, and a defined loan duration.

Here are some key characteristics of a fixed-term loan:

- Structured Repayment: With a fixed-term loan, borrowers are required to make regular, typically monthly, payments. These payments consist of both principal (the initial borrowed amount) and interest (the cost of borrowing). The advantage of this structure is that borrowers can budget and plan their finances more effectively since they know exactly when the loan will be paid off

- Fixed Interest Rate: In most cases, fixed-term loans come with a fixed interest rate. This means that the interest rate remains constant throughout the life of the loan, providing stability and predictability to borrowers

- Specific Purpose: Fixed-term loans are often taken out for specific purposes, such as purchasing a car, funding a home improvement project, or covering educational expenses. Lenders may require information about the intended use of the loan when considering the application

- Secured or Unsecured: Fixed-term loans can be either secured or unsecured. Secured loans are backed by collateral (such as a house or car), while unsecured loans are not tied to any specific asset. Secured loans typically offer lower interest rates due to reduced risk for the lender.

2. Credit Card or Line of Credit:

Credit cards and lines of credit represent a different approach to borrowing. They are often referred to as revolving credit lines, and they do not have a fixed time frame like fixed term loans. Instead, they provide borrowers with a predetermined credit limit that they can continuously use as long as they manage their credit responsibly.

Here are some key characteristics of credit cards and lines of credit:

- Revolving Credit: Credit cards and lines of credit operate on a revolving basis. As you make purchases and borrow money, you free up your available credit. Once you repay what you've borrowed, that credit becomes available to use again

- Flexible Repayments: With revolving credit, borrowers have flexibility in making payments. They can choose to make minimum payments, pay in full, or make payments above the minimum requirement. However, it's important to note that carrying a balance from month to month can result in high interest charges

- Variable Interest Rates: Unlike fixed-term loans with a fixed interest rate, credit cards and lines of credit often come with variable interest rates that can change over time. These rates are typically tied to a benchmark interest rate, such as the prime rate

- General or Specific Use: Credit cards can be used for a wide range of purposes, from everyday purchases to travel expenses. Lines of credit, on the other hand, may be more versatile, allowing borrowers to access funds for various financial needs

What is Loan Repayment?

When you borrow money from a lender, the obligation to pay back the borrowed amount arises. This process, known as loan repayment, involves returning the principal amount along with an additional cost called interest. The duration over which you repay the loan is defined by the term, and this repayment is usually done in fixed installments known as monthly payments. The mechanism that governs the gradual reduction of the loan balance through these payments is referred to as amortization.

Breaking Down Loan Repayment Terminology

Let's delve into the terminology associated with loan repayment to empower you with a deeper understanding:

- Principal: This refers to the initial sum of money you borrow from the lender. It's the foundation upon which interest and repayment calculations are based. For instance, if you borrow $10,000, the principal amount is $10,000

- Interest: The overall loan delinquency rate in the USA is typically around 3-5%. When a lender lends you money, they charge a fee for the service, known as interest. This cost is a percentage of the principal amount and serves as the lender's profit for extending the loan. Interest rates may vary based on factors like creditworthiness and prevailing market rates

- Term: The loan term is the duration within which you are required to repay the borrowed amount along with the interest. It's the agreed-upon time frame between you and the lender. Common loan terms range from a few months to several years

- Monthly Payment: To make loan repayment manageable, it's divided into equal monthly installments. Each payment consists of a portion of the principal and the interest. The sum of these payments over the term ensures the complete repayment of the loan

- Amortization: This is the systematic process of gradually reducing the outstanding loan balance through regular payments. Initially, a significant portion of your monthly payment goes towards paying off interest, while the remainder goes towards reducing the principal. As time passes, the proportion allocated to interest decreases, and the amount applied to the principal then increases

Why Should You Use a Loan Repayment Calculator?

Loan repayment calculators are crucial tools that help borrowers plan their finances, compare loan options, save money by optimizing payments, and make well-informed decisions about managing debt.

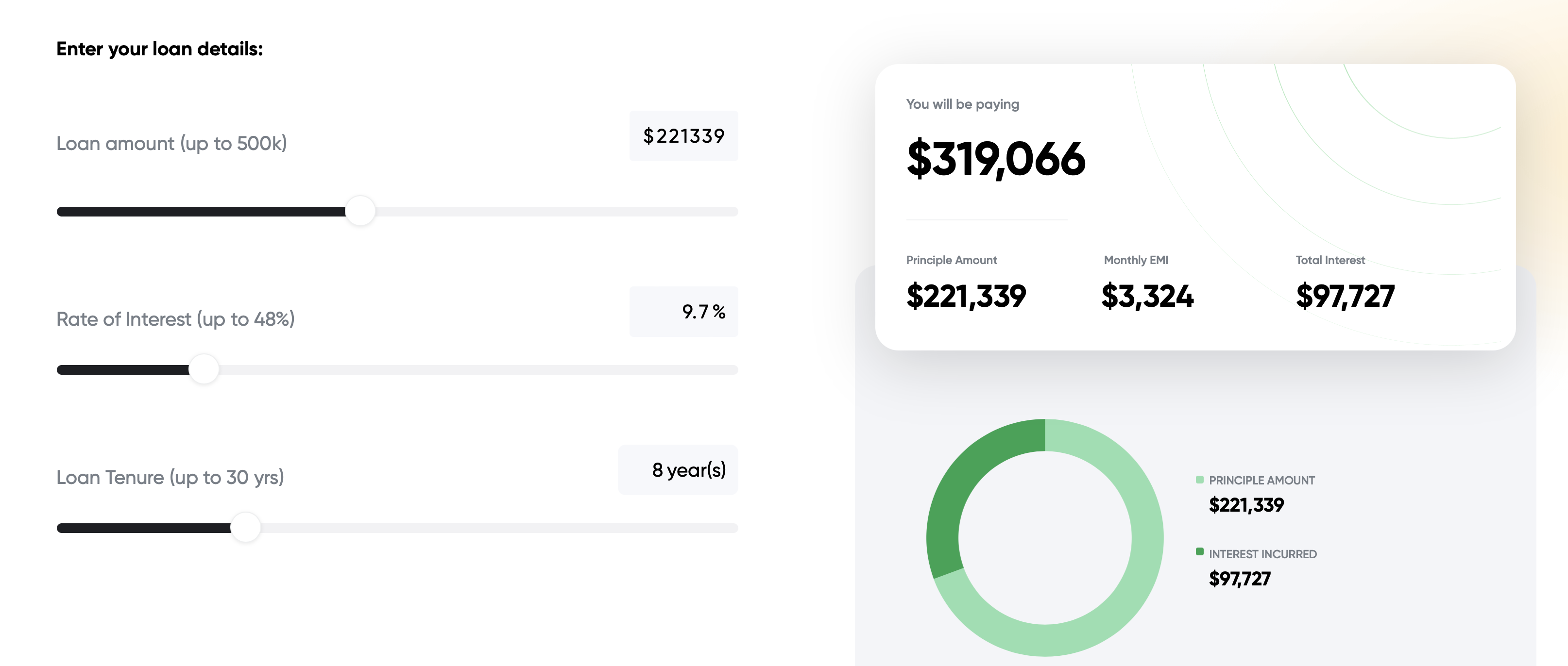

Bright Money's Loan Repayment Calculator is a powerful financial tool designed to simplify the process of calculating loan repayments. Whether you're planning to take out a personal loan, a mortgage, or any other form of borrowing, this calculator can be your trusted companion in understanding and managing your financial obligations.

Features of Bright Money's Loan Repayment Calculator

1. User-Friendly Interface

Bright Money's Loan Repayment Calculator boasts an intuitive and user-friendly interface. You don't need to be a financial expert to use it effectively. The calculator is designed to be accessible to everyone, making complex loan calculations hassle-free.

2. Multiple Loan Types

Whether you're dealing with a simple personal loan, a car loan, a home mortgage, or even a student loan, this calculator can handle it all. It supports various types of loans, allowing you to customize your calculations to your specific financial needs.

3. Loan Amount and Interest Rate

The calculator allows you to input the loan amount and the annual interest rate. You can easily adjust these values to see how different loan amounts and interest rates impact your monthly payments and the overall cost of borrowing.

4. Loan Term

Bright Money's Loan Repayment Calculator lets you choose the loan term, which is the duration over which you'll be repaying the loan. This flexibility helps you visualize how the length of the loan affects your monthly obligations.

5. Amortization Schedule

One of the most valuable features of this calculator is the ability to generate an amortization schedule. This schedule provides a detailed breakdown of each monthly payment, including how much goes toward principal and how much goes toward interest. It helps you understand how your payments change over time and how much you'll owe at any point during the loan term.

6. Extra Payments

If you plan to make additional payments towards your loan principal, Bright Money's Loan Repayment Calculator allows you to factor in these extra payments. This feature enables you to see how making extra contributions can help you pay off your loan faster and save on interest.

7. Visual Graphs

To make data interpretation easier, the calculator provides visual graphs and charts. These visuals help you visualize how different variables impact your loan repayment, making it easier to identify the most cost-effective options.

8. Real-Time Updates

As you adjust the loan parameters, the calculator updates the results in real-time, allowing you to see how changes in loan amount, interest rate, or term affect your monthly payments instantly.

9. Mobile-Friendly

Bright Money's Loan Repayment Calculator is fully responsive and mobile-friendly, ensuring you can access it on your smartphone or tablet, making financial planning on the go a breeze.

Types of Loan Repayment Methods

There are basically two types of Repayment Methods:

1. Simple Interest Method

The simple interest method is a straightforward approach to student loan repayment calculators or car loan repayment calculators that calculates interest solely based on the principal amount. Here's how it works:

- Interest Calculation: With the simple interest method, interest is calculated solely by Bright Money’s student loan repayment calculator or car loan repayment calculators on the initial principal. Each payment you make goes towards covering the interest for that specific period. The principal remains constant throughout the repayment term

- Simplicity and Drawbacks: This method is relatively simple to understand and calculate, making it suitable for short-term loans or loans with fixed interest rates. However, it might not be the most cost-effective option for long-term loans, as the interest doesn't decrease with each payment. You'll end up paying more in interest compared to other methods

2. Amortization Method

The amortization method is the most common and widely used approach for various types of loans, like mortgages, car loans, and personal loans. It's an intricate yet highly structured way to repay loans over time:

- Equal Installments: In the amortization method, your total loan amount (principal + interest) is divided into equal installments over the loan term. Each installment covers both the interest and a portion of the principal

- Shifting Balance: Each payment initially allocates a sizeable chunk to paying off the interest and a smaller piece to paying down the principle. However, the equilibrium changes as time goes on. Less of your payment is devoted to interest and more is applied to lowering the principle

- Gradual Debt Reduction: The beauty of the amortization method lies in its ability to systematically reduce your outstanding debt along with debt management. With each payment, your loan balance decreases, which in turn reduces the interest calculated on subsequent payments

- Predictable Payments: Monthly payments remain consistent throughout the loan term, making budgeting and planning more manageable

- The amortization method is advantageous for its structured approach to debt reduction and the transparency it offers regarding your loan's progress

The Loan Repayment Process

Here are the steps for the loan repayment process:

Step 1: Gather Information

This initial step sets the foundation for your loan repayment journey. It's essential to gather all pertinent information that will be used in subsequent calculations. Here's a closer look at each piece of information:

- Principal Amount: This is the original sum of money you borrowed from the lender. It serves as the base for all calculations related to interest and payments

- Interest Rate: The interest rate is a percentage that represents the cost of borrowing money. If your loan has a fixed interest rate, this percentage remains constant throughout the loan term. In the case of a variable interest rate, it can fluctuate based on market conditions

- Loan Term: The loan term specifies the duration over which you'll be making repayments. It's typically measured in months or years. Longer loan terms generally result in lower monthly payments but may lead to higher overall interest payments.

Step 2: Determine Interest Type

Understanding the type of interest rate associated with your loan is crucial as it directly impacts your repayment strategy:

- Fixed Interest Rate: With a fixed rate, the interest percentage remains steady from the start of the loan until the end. This provides stability in your monthly payments, as they will remain constant over time

- Variable Interest Rate: A variable rate means that the interest percentage can change periodically, often in response to fluctuations in the financial market. This introduces an element of uncertainty, as your monthly payments might increase or decrease as the interest rate changes.

Step 3: Choose a Repayment Plan

Selecting the right repayment plan aligns your payments with your financial capabilities and goals:

- Standard Repayment Plan: Under this plan, your monthly payments remains the same throughout the loan term. Both the interest and principal components are distributed evenly, ensuring predictability in your budget

- Graduated Repayment Plan: This plan begins with lower initial payments that gradually increase over time. It's suitable if you anticipate your income to grow in the future, enabling you to manage higher payments later

- Income-Driven Repayment Plan: Income-driven plans adjust your monthly payments based on your current income. If your earnings are lower, your payments will be lower as well, offering flexibility during periods of financial uncertainty.

Step 4: Calculate Monthly Payment

Calculating the monthly payment involves employing the loan amortization formula, which considers several variables:

- Loan Amount: This is the principal amount you borrowed

- Interest Rate: Expressed as a decimal, it represents the cost of borrowing

- Loan Term: The number of payment periods, whether in months or years.

Using this information, the formula calculates the monthly payment that combines both the interest and principal amounts. While the formula itself can be complex, various online debt consolidation calculators are available to simplify the process. These debt consolidation calculators prompt you to input your loan details, and they swiftly provide you with the exact monthly payment you'll need to make.

Factors Affecting Loan Repayment

There are several factors influence the loan repayment process:

1. Interest Rate

The interest rate is a pivotal factor in determining the overall cost of the loan. A higher interest rate translates to higher monthly payments and a greater total repayment amount. The type of interest rate, whether fixed or variable, also affects repayment. Fixed rates offer predictability, while variable rates can lead to fluctuations in payments based on market conditions.

2. Loan Amount

The principal amount you borrow significantly impacts your repayment. Larger loan amounts generally result in higher monthly payments and a greater overall repayment obligation. It's important to carefully assess your financial capacity to handle the repayments in relation to the loan amount.

3. Loan Term

The loan term, or the duration over which you'll be repaying the loan, plays a crucial role. Longer loan terms typically lead to lower monthly payments, as the repayment is spread out. However, this can also result in paying more in interest over the life of the loan. Shorter loan terms generally mean higher monthly payments but less interest paid overall.

5. Income Level

Your current income has a direct impact on your ability to make loan payments. If you have a higher income, you might opt for shorter loan terms to minimize overall interest payments. For individuals with lower incomes, income-driven repayment plans can provide manageable payment options.

6. Financial Stability

Your overall financial stability influences your ability to make consistent payments. Sudden changes in income, unexpected expenses, or job loss can disrupt your repayment schedule. Maintaining an emergency fund can provide a safety net during such times.

7. Prepayment Options

Some loans allow for prepayment or early repayment without penalties. If you have the means to pay off the loan faster than the agreed-upon schedule, it can reduce the total interest paid and shorten the repayment period.

8. Credit Score

Your credit score affects the interest rate you receive. A higher credit score may result in cheaper interest rates, which can greatly effect loan affordability.

9. Economic Conditions

Economic conditions can influence interest rates, affecting both fixed and variable rates. During periods of economic growth, interest rates might rise, leading to increased loan costs.

10. Loan Type and Purpose

Different types of loans (e.g., student loans, mortgages, personal loans) have varying terms and conditions. The purpose of the loan (education, home purchase, debt management) can also impact repayment options and terms.

Final Thoughts

In conclusion, understanding how to calculate loan repayment is a vital skill for anyone considering borrowing money. By comprehending the key terminology, repayment methods, and influential factors, you can approach loan repayment with confidence. Whether you're taking out a mortgage, a car loan, or a personal loan, these insights will empower you to make informed financial decisions.

Remember, the world of loan repayment doesn't have to be daunting. Armed with knowledge and supported by technology, you can navigate this journey successfully. So, next time you're considering a loan, approach it with the insights gained from this guide and embark on a path toward financial stability.

Recommended Reads:

How To check your credit score?

FAQs

1. What Is Loan Repayment?

Loan repayment is the process of returning the borrowed amount to the lender along with an additional cost known as interest. This process involves a series of structured payments over a specified period until the borrowed amount is fully settled.

2. How Do I Begin the Loan Repayment Process?

The loan repayment process begins by gathering essential information. You'll need to know the principal amount (the initial sum borrowed), the interest rate (either fixed or variable), and the loan term (the agreed-upon duration for repayment).

3. What's the Difference Between Fixed and Variable Interest Rates?

A fixed interest rate stays as it is throughout the loan term, resulting in predictable monthly payments. A variable interest rate, however, can fluctuate based on market conditions, leading to potential changes in your payments over time.

4. What Repayment Plans Are Available?

There are various repayment plans tailored to different financial situations:

1. Standard Repayment: Equal monthly payments over the term.

2. Graduated Repayment: Payments start low and increase gradually.

3. Income-Driven Repayment: Payments adjust based on income.

5. How Do I Calculate My Monthly Payment?

In order to calculate your monthly payment, you can use the formula for loan amortization. This formula considers the principal, interest rate, and loan term. Alternatively, you can use online debt consolidation calculators that provide quick and accurate results.

6. What Is the Simple Interest Method?

The simple interest method calculates interest solely on the principal amount. Payments go towards covering the interest, and the principal remains unchanged. This method is suitable for short-term loans or those with fixed interest rates.

7. What Is the Amortization Method?

The amortization method divides payments into equal installments covering both principal and interest. Over time, the balance shifts, and more of your payment goes towards reducing the principal. This method is commonly used for mortgages and car loans.

8. Which Repayment Method Is Right for Me?

The choice between the simple interest and amortization methods depends on factors like your loan type, interest rate, and financial goals. Short-term loans might benefit from the simple interest method, while the amortization method suits long-term loans.

9. Can I Pay More than the Minimum Monthly Payment?

Absolutely! Making extra payments towards the principal can help you in paying off the loan faster and reduce the total interest paid over time.

10. What Happens If I Miss a Payment?

Missing a payment can have various consequences, including late fees and also a negative impact on your credit score. It's important to communicate with your lender if you're facing difficulties to explore possible solutions.

11. How Can Technology Help with Loan Repayment?

Online loan calculators and apps can simplify complex calculations, providing accurate results and helping you explore different scenarios. These tools streamline the process and eliminate the risk of calculation errors.

12. How Can I Ensure Successful Loan Repayment?

Creating a proper budget, paying more than the minimum, and staying informed about your loan terms are crucial steps. Regularly assessing your financial situation and making adjustments as needed will contribute to successful repayment.

13. Where Can I Find Expert Advice on Loan Repayment?

For expert advice and insights on loan repayment and various financial matters, visit ContGPT. This platform offers valuable resources to guide you through your financial journey.

14. Is Loan Repayment a Daunting Task?

Loan repayment might seem complex, but armed with knowledge and resources, you can manage it effectively. Remember that understanding the process and seeking guidance empowers you to make informed decisions.

15. What's the First Step I Should Take?

The first step is to gather all the necessary information about your loan—principal amount, interest rate, and loan term. With this information, you'll be well-equipped to start the loan repayment process.