You are now leaving the Bright website and entering a third-party website. Bright has no control over the content, products, or services offered, nor the security or privacy of information transmitted to others via their website. We recommend that you review the privacy policy of the site you are entering. Bright does not guarantee or endorse the products, information, or recommendations provided on any third-party website.

When it comes to managing one's finances and fulfilling financial goals, individuals often find themselves at a crossroads, trying to choose between Personal Loans and lines of credit. Both these financial tools offer unique advantages and come with their own set of considerations.

But before we get into the topic, it is recommended to first read about Mastering Loan Repayment in detail by Bright Money!

In this exploration, we will delve into the distinctions between Personal Loans and lines of credit, shedding light on the crucial factors that can guide individuals in making informed financial decisions.

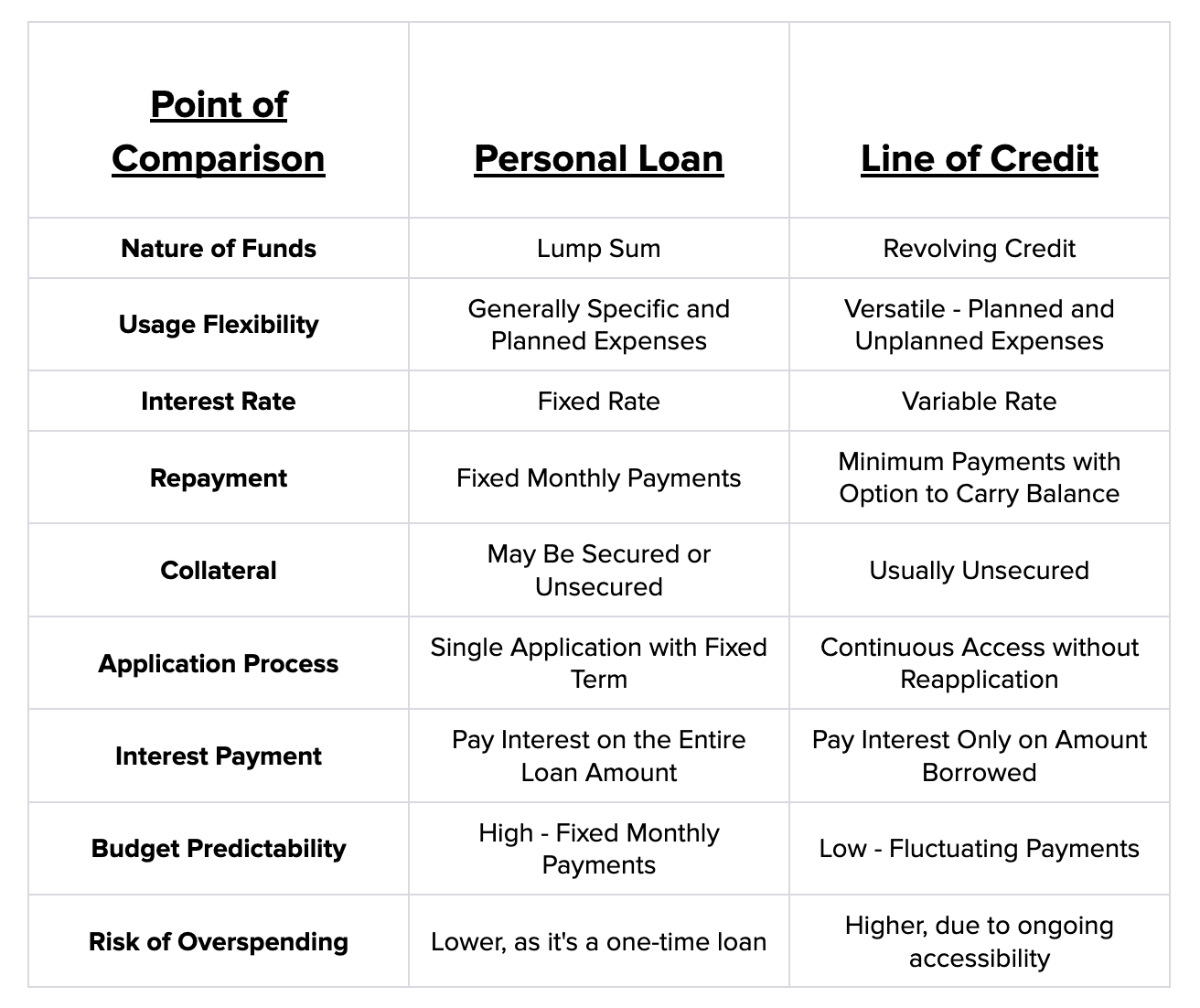

Personal Loan vs. Line of Credit

The choice between a Personal Loan and a Line of Credit depends on your specific needs:

- Personal Loan: Better for one-time expenses with a fixed amount and repayment schedule

- Line of Credit: Better for ongoing or flexible borrowing needs with a revolving credit limit

What is a Personal Loan?

Personal Loans are one of the fastest-growing forms of consumer lending, with a market size expected to grow by $476.25 billion by 2027. A Personal Loan is a lump-sum amount borrowed from a financial institution, such as a bank or an online lender, with the agreement to repay it over a fixed term. These loans are typically unsecured, meaning they do not require collateral, and can range from a few hundred to several thousand dollars. The repayment terms can vary from a few months to even several years, depending on the lender and the amount borrowed.

Benefits of Personal Loan

1. Predictable Payments

One of the primary advantages of Personal Loans is the predictability they offer in terms of monthly payments. When you take out a Personal Loan, you receive a fixed interest rate and a clearly defined repayment schedule. Here's why this predictability is such a valuable feature:

Fixed Interest Rate: The interest rate on a Personal Loan is fixed for the duration of the loan. This means your interest rate will remain unchanged from signing the loan agreement until the last payment. Because of this predictability, you can confidently manage your budget since you know precisely how much you must set aside monthly for your loan payment

Set Repayment Schedule: Personal Loans also come with a predetermined repayment schedule. You'll know the monthly payments required to pay the loan in full. This makes budgeting easier and ensures you won't be caught off guard by unexpected increases in your monthly obligations

Financial Planning: The predictability of Personal Loan payments is especially beneficial for individuals who plan their finances meticulously. Whether you're managing a tight budget or simply prefer to have a clear picture of your financial commitments, Personal Loans provide the stability and certainty you need.

2. Versatile Use

Personal Loans are known for their versatility regarding using the funds. Here's a closer look at this benefit:

Debt Consolidation: Personal Loans can be an excellent tool for consolidating high-interest Debt. By taking out a Personal Loan to pay off multiple Credit Card balances or other Debts, you can often secure a lower interest rate, reduce your monthly payments, and thus simplify your financial life.

Covering Medical Expenses: Unexpected medical bills can strain your finances. Personal Loans can provide the funds needed to cover medical expenses, offering peace of mind during challenging times.

Financing a Vacation: Personal Loans can make it possible whether it's a dream vacation or a much-needed getaway. By spreading the cost of your trip over a fixed term, you can enjoy your vacation without depleting your savings.

Home Improvements: Personal Loans are a popular choice for funding home improvement projects. These loans provide the capital required to enhance your living space, from renovating your kitchen to adding an extra bedroom.

3. No Collateral Required

Personal Loans are typically unsecured loans, which means they do not require borrowers to put any assets as collateral. This characteristic offers several benefits:

Reduced Risk: Since Personal Loans don't involve collateral, your personal property, such as your home or car, is not at risk if you face difficulties repaying the loan. This can provide peace of mind, particularly for individuals uncomfortable with the idea of putting their assets on the line

Faster Approval: Unsecured loans often have a quicker approval process than secured loans, which may involve extensive documentation and evaluations of the collateral's value. Personal Loans are accessible to a broader range of borrowers, including those who may not have valuable assets to use as collateral.

4. Fixed Interest Rates

Most Personal Loans come with fixed interest rates, meaning the interest rate remains constant throughout the loan term. This feature offers several advantages:

Rate Stability: Fixed interest rates shield borrowers from unexpected interest rate hikes. Regardless of fluctuations in the broader financial market or changes in the lender's policies, your interest rate will stay the same. This stability makes it easier to budget and plan for the long-term cost of the loan.

Long-Term Savings: If you secure a Personal Loan with a favorable fixed interest rate, you can save money over time compared to variable-rate loans, such as Credit Cards or adjustable-rate mortgages. Your fixed rate ensures that interest costs are known from the outset, helping you make financially savvy decisions.

Drawbacks of Personal Loans

1. Higher Interest Rates

Interest Rate Comparison: One of the notable drawbacks of Personal Loans is that they may carry higher interest rates than other forms of credit. The specific interest rate you receive on a Personal Loan can vary significantly based on factors like your Credit Score, credit history, and the lender's policies. Individuals with lower Credit Scores may face higher interest rates, which can substantially increase the cost of borrowing.

Impact on Cost: Higher interest rates mean that you'll ultimately pay more for the same borrowed amount over the life of the loan. This can impact the total cost of the loan significantly, making it essential to carefully consider whether the benefits of the loan outweigh the potential interest expenses.

competitive rates and terms to ensure you get Shopping for Rates: To mitigate the impact of higher interest rates, shopping around for the best rates and terms is crucial. Different lenders offer varying interest rates, so taking the time to compare offers can potentially save you a substantial amount of money. Be proactive in seeking competitive rates and terms to ensure you get the most favorable deal possible.

2. Origination Fees

Some lenders charge these fees. What Are Origination Fees: Another potential drawback of Personal Loans is the presence of origination fees. Some lenders charge these fees at the beginning of the loan application process and are intended to cover the administrative costs associated with processing and approving the loan.

Impact on Borrowing Costs: Origination fees can significantly add to the overall borrowing cost. These fees are typically calculated as a percentage of the total loan amount, so the larger the loan, the higher the origination fee. Borrowers must be aware of these fees and factor them into their decision-making process.

Comparing Loan Offers: When evaluating Personal Loan offers from different lenders, it's essential to inquire about origination fees. Some lenders may charge you higher fees than others, while some may not charge any at all. This information should be considered alongside the interest rate and other terms to determine the true cost of the loan.

Juggling multiple Credit Card Debts can be a financial and emotional burden. Debt consolidation simplifies this by merging all your outstanding balances into a single loan, often with a lower interest rate. Bright Money can help.

What is a Line of Credit?

The global Line of Credit market is expected to grow at a CAGR of 4.8% from 2021 to 2028. A flexible financial arrangement known as a Line of Credit (LOC) gives you access to a revolving credit limit. A Line of Credit lets you borrow money up to a certain limit, unlike a Personal Loan, which provides a flat payment; you only pay interest on the amount you actually use. It is comparable to having a financial safety net that you may use when necessary.

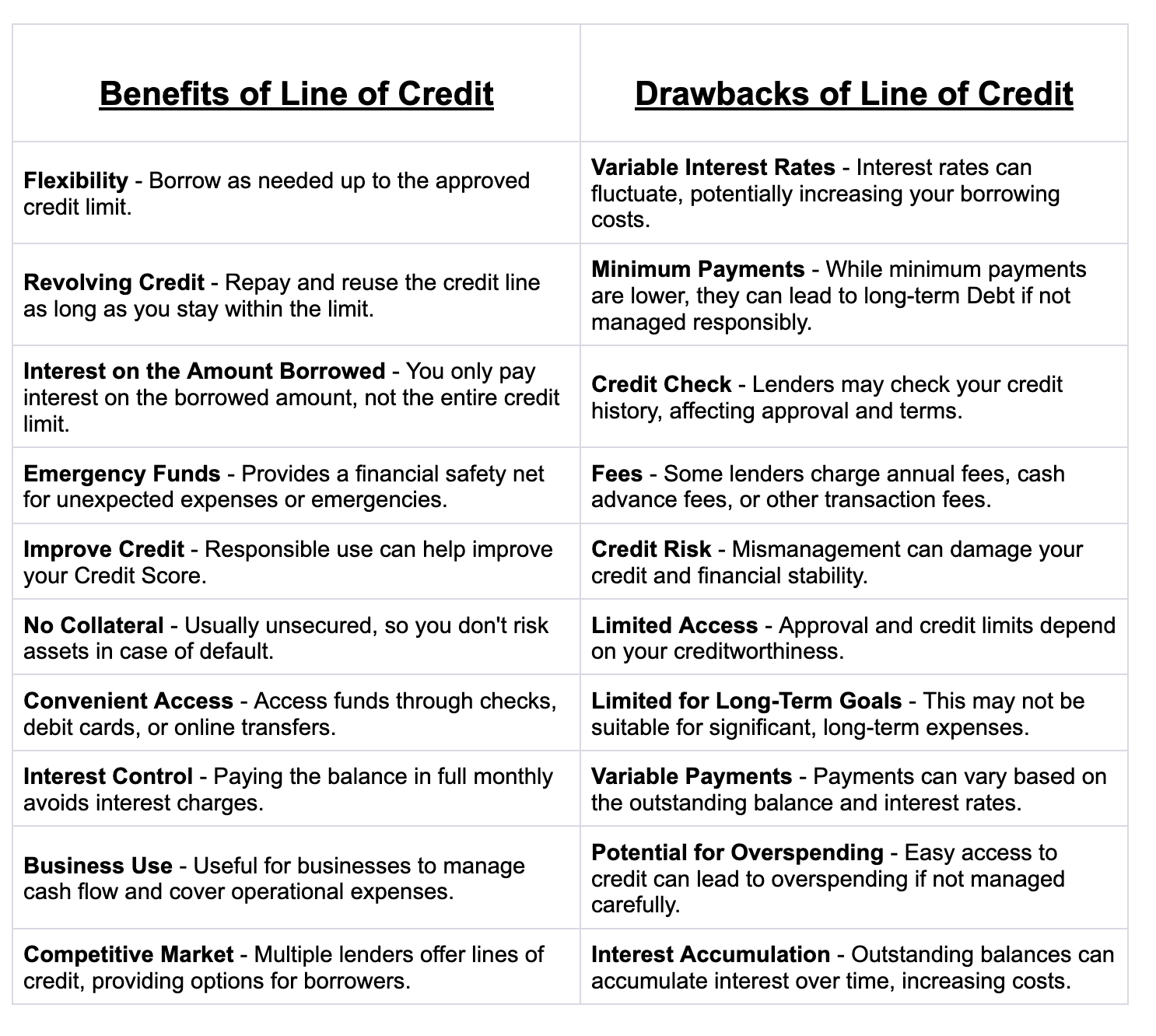

Benefits of Lines of Credit

1. Flexibility

Versatile Use: Lines of credit offer remarkable flexibility regarding utilizing the funds. Unlike some other financial products with specific restrictions, lines of credit allow you to use the borrowed money for various purposes. This versatility makes lines of credit suitable for planned expenses and unforeseen emergencies.

Planned Expenses: For planned expenses like home renovations, tuition fees, or business investments, lines of credit can provide a convenient funding source. You can access the necessary funds when you need them without the need to apply for a new loan each time.

Emergency Funds: Lines of credit also act as a financial safety net during unexpected emergencies, such as medical bills, car repairs, or sudden job loss. Having a readily available source of funds can provide peace of mind in times of crisis.

Interest Savings: One key advantage is that you only pay interest on the amount you borrow, not on the entire credit limit. This feature allows you to keep the Line of Credit open for future needs without incurring unnecessary interest charges. It's a cost-effective way to access credit when necessary while minimizing ongoing expenses when the credit is not in use.

2. Lower Interest Costs

Comparative Advantage: Lines of credit often come with lower interest rates than carrying a balance on high-interest Credit Cards. Credit Card interest rates can become exceptionally high, making it costly to maintain a balance. In contrast, lines of credit typically offer more favorable terms, helping borrowers save money on interest charges.

Long-Term Savings: The lower interest costs associated with lines of credit can result in substantial long-term savings. Whether you're using the credit for ongoing expenses or larger investments, paying less interest over time can significantly impact your financial health.

Financial Stability: Lower interest costs make it easier for borrowers to manage their Debt and maintain financial stability. The reduced financial burden can lead to more manageable monthly payments, allowing individuals to allocate resources to other important financial goals and obligations.

3. Revolving Credit

Continuous Access: One of the most valuable features of a Line of Credit is its revolving nature. As you repay the borrowed amount, it becomes available for you to use again. This revolving credit structure is akin to having a financial safety net that never depletes as long as you manage it responsibly.

Convenience: The revolving nature of lines of credit eliminates the need to reapply for a new loan each time you require funds. This convenience saves time and paperwork, making lines of credit a practical choice for individuals who value ease of access to credit.

Capitalizing on Opportunities: Accessing funds quickly and without hurdles can be advantageous in seizing investment opportunities, such as purchasing stocks, acquiring assets, or expanding a business. Lines of credit provide the financial flexibility needed to act swiftly when opportunities arise.

Drawbacks of Lines of Credit

1. Variable Interest Rates

Fluctuating Monthly Payments: One of the primary drawbacks of lines of credit is their often variable interest rates. Unlike Personal Loans, which offer fixed interest rates, lines of credit come with interest rates that can change over time. These rate fluctuations can lead to monthly payments that are inconsistent and harder to predict.

Budgeting Challenges: The variability in monthly payments can make budgeting more challenging for individuals. It's difficult to allocate a specific monthly amount when you're unsure about the interest rate changes. This unpredictability can cause financial stress, particularly for those who rely on stable and consistent budgets.

Interest Rate Risk: Borrowers with lines of credit are exposed to interest rate risk. If interest rates rise, it can result in higher monthly payments, potentially straining your finances. It's essential to be prepared for increased interest costs and factor this into your financial planning.

2. Temptation to Overspend

Easy Accessibility: Lines of credit offer high accessibility to funds. This convenience can be both a blessing and a curse. While it's advantageous to have readily available credit for genuine needs, it can also be tempting to overspend when the funds are so easily accessible.

Risk of Accumulating Debt: The accessibility of a Line of Credit can lead to the accumulation of Debt if not managed responsibly. Some individuals may succumb to the temptation of using the credit line for non-essential purchases or unnecessary expenses, resulting in a growing Debt balance that can be challenging to repay.

Discipline is Key: To avoid overspending and the potential pitfalls of accumulating Debt, discipline is crucial when using a Line of Credit. It's essential to exercise restraint and tap into the credit line when it is necessary, such as for emergencies or planned expenses that align with your financial goals.

Juggling multiple Credit Card Debts can be a financial and emotional burden. Debt consolidation simplifies this by merging all your outstanding balances into a single loan, often with a lower interest rate. Bright Money can help.

Choosing Between a Personal Loan and a Line of Credit

The decision between a Personal Loan and a Line of Credit is significant, as it can substantially impact your financial situation. To make an informed choice, consider the following guidelines tailored to your specific needs and objectives:

Choose a Personal Loan if:

1. You Have a Specific, One-time Expense: If you have a clearly defined, one-time expense, such as a home renovation project, purchasing a car, or consolidating high-interest Debt, a Personal Loan can be an excellent choice. Personal Loans provide a lump sum of money upfront, which can be particularly helpful when you know the exact amount you need to cover your expenses.

Example: Let's say you plan to undertake a home renovation project. You've received contractors' quotes and know the project will cost you $20,000. In this scenario, opting for a Personal Loan is an excellent choice. You can apply for a $20,000 Personal Loan, receive the funds upfront, and pay your contractors and suppliers a lump sum. With fixed interest rates and a set repayment schedule, you'll have predictability in your monthly payments, making it easier to budget for the renovation.

2. You Prefer the Predictability of Fixed Monthly Payments: Personal Loans offer fixed interest rates and set repayment schedules. Suppose you value predictability in your financial planning and want to know precisely how much you'll pay each month until the loan is repaid fully. In that case, a Personal Loan aligns with your preference. This can make budgeting more straightforward.

Example: Suppose you plan to consolidate your high-interest Credit Card Debts, which amount to $15,000. A Personal Loan with a lower interest rate can help you save on interest costs and simplify your Debt management. You apply for a $15,000 Personal Loan, receive the funds, and use them to pay off your Credit Card balances. With fixed monthly payments, you can create a clear Debt repayment plan and work towards becoming Debt-free.

3. You Want to Avoid the Temptation of Continually Borrowing: Personal Loans come with a defined term and fixed monthly payments. Suppose you're concerned about the temptation to borrow more than you need or accumulate additional Debt over time. In that case, a Personal Loan structure can help you stay disciplined in paying off your obligations without the option of continuous borrowing.

Example: Imagine you're in the market to purchase a new car. After researching your options, you find a vehicle that fits your needs, and the total cost is $25,000. Choosing a Personal Loan for this one-time expense allows you to secure the funds necessary to buy the car. With a fixed interest rate and a set repayment schedule, you can budget for your car payments and enjoy the predictability of Personal Loans.

Choose a Line of Credit if:

1. You Have Ongoing, Unpredictable Expenses: Lines of credit are exceptionally well-suited for individuals with ongoing and unpredictable financial needs. If you regularly encounter expenses like medical bills, home repairs, or irregular income fluctuations, a Line of Credit provides you with a flexible source of funds to tap into as needed.

Example: Imagine you're a freelance graphic designer with an irregular income, and you often encounter unexpected expenses like equipment repairs or medical bills. In this case, a Line of Credit is a suitable financial tool. You can establish a Line of Credit with a credit limit of $10,000. When you face an unforeseen expense, you can tap into your Line of Credit to cover the cost, whether it's a $500 repair bill or a $1,000 medical expense. The flexibility of a Line of Credit allows you to borrow as needed without reapplying for a new loan each time, helping you manage your financial fluctuations.

2. You Want the Flexibility to Borrow as Needed Without Reapplying for a Loan: Unlike Personal Loans that provide a one-time lump sum, lines of credit offer a revolving credit limit. This means you can borrow, repay, and borrow again without the need to reapply for a new loan each time. It's a convenient option for those who require access to credit on an ongoing basis.

Example: As a small business owner, you often encounter irregular cash flow patterns. You need access to funds to cover operational expenses like inventory purchases, unexpected repairs, or payroll gaps. In this situation, a business Line of Credit is a valuable financial tool. You establish a Line of Credit with a $50,000 credit limit. When cash flow is tight or when unexpected expenses arise, you can draw funds from your Line of Credit to meet your business needs. This flexibility helps you manage your business's financial ups and downs effectively.

3. You Are Confident in Your Ability to Manage Revolving Credit Responsibly: Lines of credit require responsible financial management. If you feel confident in your ability to use credit wisely, make timely repayments, and not fall into the temptation of excessive borrowing, a Line of Credit can be an advantageous tool. Properly managed, it can offer financial stability and flexibility.

Example: You're a homeowner who anticipates occasional maintenance and repair costs. Rather than taking out a lump sum Personal Loan for each repair, you open a home equity Line of Credit (HELOC) with a $30,000 credit limit. When your roof needs repairs, you use your HELOC to cover the $5,000 expense. A few months later, you encounter plumbing issues, and you tap into your HELOC again for the $4,000 repair cost. The flexibility of the HELOC allows you to address these home-related expenses as they arise without needing a new loan for each project.

Conclusion

In the dynamic landscape of personal finance, choosing between a Personal Loan and a Line of Credit is far from trivial. Each option has merits and demerits, serving different financial needs and circumstances. The decision ultimately concerns individual preferences, goals, and financial standing. Whether it's the structured approach of a Personal Loan or the flexibility of a Line of Credit, understanding the nuances of these financial tools empowers people to make choices that align with their unique financial journeys.

So, as you embark on your path toward financial stability and growth, remember that the right choice between a Personal Loan and a Line of Credit can be a pivotal step toward achieving your financial aspirations.

Juggling multiple Credit Card Debts can be a financial and emotional burden. Debt consolidation simplifies this by merging all your outstanding balances into a single loan, often with a lower interest rate. Bright Money can help.

Recommended To Read:

Should I pay my Credit Card bill as soon as I get it?

3 reasons to use Personal Loans to pay off Debt

FAQs

1. What is a Personal Loan, and how does it differ from a Line of Credit?

A Line of Credit(LOC) is a revolving credit account that enables you to draw funds up to a certain maximum as needed, whereas a Personal Loan is a lump sum of money that is obtained for a specified reason with set monthly payments.

2. What are the typical uses for a Personal Loan?

Personal Loans are usually used for Debt consolidation, home improvement, medical expenses, weddings, and other one-time expenses.

3. When should I consider applying for a Line of Credit?

Lines of credit are often suitable for ongoing or unpredictable expenses, such as covering emergencies, paying for educational costs, or managing irregular cash flow in a business.

4. How do interest rates compare between Personal Loans and lines of credit?

Personal Loans usually have fixed interest rates, while lines of credit often have variable rates that can change over time. Personal Loans may offer more predictable monthly payments.

5. What's the typical repayment period for a Personal Loan vs. a Line of Credit?

Personal Loans typically have fixed terms ranging from 1 to 7 years, whereas lines of credit have no set term, and you can borrow and repay as long as the line remains open.

6. Do Personal Loans or lines of credit affect my Credit Score differently?

Both can impact your Credit Score. Timely payments on either can positively affect your Credit Score, while late payments can harm it.

7. Which option is better for consolidating existing Debts?

A Personal Loan is often a preferred choice for Debt consolidation because it offers a fixed interest rate and term, making it easier to budget for repayment.

8. Can I get a Personal Loan or a Line of Credit with bad credit?

It can be challenging, but not impossible. Some lenders offer Personal Loans and lines of credit for individuals with less-than-perfect credit, although the terms may not be as favorable.

9. Are there any fees associated with Personal Loans or lines of credit?

Both types of credit may come with fees, such as origination fees for Personal Loans and annual fees for lines of credit. It's essential to review the terms and conditions of the specific loan or line you're considering.

10. Can I have both a Personal Loan and a Line of Credit simultaneously?

Yes, having a Personal Loan and a Line of Credit is possible, but it's crucial to manage them responsibly and ensure they align with your financial goals.

References:

https://www.imarcgroup.com/consumer-credit-market

Disclaimer:

For credit building related: payment history has the biggest impact on Credit Score, accounting for 40% of how score is calculated per transunion (https://www.transunion.com/credit-score). Bright Builder helps you build payment history that may positively improve your Credit Score. Credit Score increase is not guaranteed. Individual results may vary. Late payments, missed payments, or other defaults on your accounts with us or others will have a negative effect on your Credit Score. Products and services subject to state residency and regulatory requirements. Bright Builder is currently not available in all states.